国内会计准则和国际会计准则的价值相关性——以AB股公司的会计数据及其在A股市场上的股票价格为例

2016-11-19 08:04李世祥

经济研究导刊 2016年27期

李世祥

(萨里大学,英国 伦敦 GU2 7JL)

国内会计准则和国际会计准则的价值相关性——以AB股公司的会计数据及其在A股市场上的股票价格为例

李世祥

(萨里大学,英国 伦敦 GU2 7JL)

以同时发行A股和B股的公司的会计数据为基础,研究A股市场的会计数据和股票之间的价值相关性。使用价格水平模型和E-view,对44个AB股公司十年的会计数据(每股盈利和每股净利润)和相应时点的股票价格进行混合最小二乘法回归,研究当国内的会计准则更多地融合了国际会计准则后A股市场上价值相关性的变化情况。因自2007年起,国内的会计制度规定更多地融合国际会计准则,故将十年分为两个阶段(2002—2006年和2011—2015年)以便对两个不同时期回归结果做出比较,从而得出更加精确的结论。运用随机事件效应以及固定时间效应(即按年回归)分别对两个时期的数据进行截面分析,得出以下结论:每股收益在A股市场上的价值相关性在国内会计准则更多地融合了国际会计准则后有一定程度的增加,换句话说,国际会计准则的部分使用能够提高以每股收益为代表的会计信息的价值相关性。但是,发现每股净利润在两个时期都不具有价值相关性。根据回归结果,在国内的会计准则下,会计信息的价值相关性有一定的相对稳定性,但是当国内的会计准则融合了更多的国际会计准则之后,每股收益呈逐年递增的趋势(2015年除外)。

价值相关性;国内会计准则;国际会计准则;A股市场;AB股公司;每股收益;每股净利润;股票价格

CHAPTER 1:INTRODUCTION

It is necessary to know the history of capital market in China before conducting studies of associations between accounting information and stocks’prices.As the second biggest economy in the world,China plays an important role and its unique economic and financial structure has attracted an increasing number of researchers’eyes.Stock firms reappeared in the Chinese economy in the late 1980s with the purpose of facilitating the economy.The Shanghai Stock Exchange market and the Shenzhen Stock Exchange market were established in the 1990s,which lead to the repay expansion of the capital market(Chen and Thomas,2003).However,the stock market in China was far from standardized as it has an imperfect regulatory framework,especially in the aspect of accounting information disclosure and financial reporting,compared with those capital markets in developed countries.The lack of transparent and reliable financial information may lead to information asymmetry,which may influence the investors’forecast of companies’future performance and therefore a less effective investment decision(A-harony et al.2000).

1.Research questions

The first research question is that the value-relevance of Chinese GAAP and the converged Chinese GAAP(with IFRS),in other words,whether the Chinese GAAP and the converged Chinese GAAP are value-relevant or not.Furthermore,the other research question is that changes on value-relevance after Chinese GAAP converged with more IFRS,in other words,changes on the degree of value-relevance after Chinese GAAP converged with more IFRS(increase or decrease).And this paper will discuss the value-relevance in terms of two accounting numbers(earnings and book values).

2.Research objectives

The research objectives of this paper are accounting numbers(earnings and book values)and A-stock prices of AB-share companies.The typical stock market structure in China provided an opportunity to test the value-relevance of accounting information reported under different accounting standards.Companies is-suingboth A-share and B-share are the best choice tobe selected as sample to study the value-relevance of accounting information reported under Chinese GAAP and the converged Chinese GAAP. The reason is that companies issuing both A-share and B-share are requested to prepare two financial reports(one is under Chinese GAAP and the other one is under IFRS).Those companies may have more experiences and accounting practices to make a better reconciliation with the IFRS,which may get more accurate results.Such kind of studies should be able to examine the necessity and feasibility of converging Chinese GAAP with more IFRS in China.

CHAPTER 2:LITERATURE REVIEW

1.Related studies on value-relevance in China

Studies on the adoption of IFRS in China is also becoming more and more far-reaching because some specialized institution ranked China as the second largest economy which is next to the America.As the quickly growing emerging market,China has been playing an important role in the world’s capital market,which is increasingly attractive to investors all over the world(Lin and Liu,2009).From this aspect,the adoption ofthe IFRS and its fitness in China may directly influence the accounting reporting comparability,which is becoming more and more significant to investors. Although the IFRS was not adopted by the China’s government completely,the reform ofthe accounting system in China has been conducted years ago.The new business accounting reform,one of the points in the accounting reform,had been introduced by the government in 1993.Such newaccounting system has been developing which is referring to the IAS in order to keep pace with the international trend(Xiao et al.,2004).Such reforming is mainly due to the economic reform and increasing foreign activities occurred in China(Tang,2000).Furthermore,in the year of 2007,all listed companies in China were requested by the government to adopt a new set of accounting standards which brought the IFRS together.IFRS converged with CAS was seen as converged substantiallywith IFRS(IFRS,2013).

Many researchers also conducted some research on the adoption of the IFRS in different companies in China.Increasingly using of the IFRS in China would facilitate its accounting quality and its stock prices level(Chen and Thomas,2003).However,Chamisa(2000)argued that it maybe inappropriate touse those findings in the Chinese market because of the economic environment and historical developments in different countries may vary.Moreover,Daske et al.(2008)argued that the IFRS accounting system may facilitate the development of capital market,but this is only effective under the developed capital market which has a perfect legal system and strong transparent reporting system.In other words,the adoption of IFRS in China maybe less effective,especiallyin the China’s capital market.

After a year,Lin and Chen(2005)initiated a study to address such limitations using both the Price-level Model and the ReturnModelandmadeacomparisonbetweenthe value-relevance of Chinese GAAP and the reconciliation with IFRS in both the A-stock and B-stock market,which eliminated the potential bias comes from sampling by choosing companies issuing bothA-stocks andB-stocks.Moreimportantly,they selected a sampling period before the year of 2000 which is the starting time of the Chinese GAAP’s reforms.In other words,they eliminated an extra variable which may influence the results of such study.They figured out that financial earnings on the basis of Chinese GAAP were effective in explaining stock prices in both the A-stock market and the B-stock market.But when it comes to the returns,financial earnings based on the Chinese GAAP tended to be value-relevant in the A-stock market instead of the B-stock market.Furthermore,they found that changes on earnings on the basis of Chinese GAAP were value-relevant in explaining stock prices and returns in the B-stock market instead of the A-stock market.Those results indicated that the B-stock investors may consider accounting information comes from both Chinese GGAP and FIRSwhen makinginvestment decisions.

More recently,Tamer(2014)studied the H-share,A-share and B-share in China’s stock market adopting OLS regression method using accounting data from 1999 to 2012 and found that the market variations of both A-and B-shares have a significant association with the accounting information in terms of EPS and book value of equity per share.When it comes to the H-share market,the outcomes were more obvious even though the observing variations were the accounting information on market value instead of the stock prices.Furthermore,such research analyzed the joint effects of both accounting data and the adoption of IFRS with Chinese GAAP,which is more meaningful than the single effects.What’s more,it also figured out that the impacts of the converged IFRS with Chinese GAAP were more associated with accounting information such as earnings and book values on both market values and stock prices in the AB-shares market than in the H-share market.Although this contention may have less convincing empirical evidence,they enriched the study findings on the impacts ofconverged Chinese GAAP.

CHAPTER 3:METHODOLOGY

1.Research design

Although manyresearchers have studied the value-relevance ofthe AB-share markets,the data was too old and the results may beoutdated,therewasnostudythatcomparingthe value-relevance in the same market during different periods of time.I will check out the previous results and have a further study on the value-relevance after the adoption of the new accounting policyin 2007 that the Chinese GAAP converged with more IFRS. In the year of 2007,all listed companies in China were requested by the government to adopt a new set of accounting standards which brought the IFRS together.IFRS converged with CAS was seen as converged substantially with IFRS(IFRS,2013).Under such circumstances,Liu et al.(2011)studied influences after the adoption of the new accounting standards on the accounting information quality of A-share companies only,which found that the converged IFRS to Chinese GAAP imposed an important impactonaccountingqualitybyimprovingtheearning management and increasing the degree of value-relevance in a specific period oftime which is from 2005 to 2008.This paper will study the value-relevance on the basis of this new accounting policy.

This paper have mentioned that all listed companies in China were requested bythe government toadopt a newset ofaccounting standards which brought the IFRS together in the year of 2007,which means that accounting data before 2007 was not converged with the IFRS or was converged little with the IFRS,and accounting data after 2007 was more converged with the IFRS. And this paper assumes that the Chinese GAAP was converged with little IFRS before 2007.This paper tries to analyze the value-relevance in the A-stock market by using accounting data which were selected fromtwoperiods(period 1 was from2002 to 2006 and period 2 was from 2011 to 2015)to figure out changes on the degree of value-relevance in the A-stock market among AB-share companies after adopting the new accounting policy. The main aim of this paper is to test whether there were some changes on the value-relevance after adopting the newaccounting policy in the A-stock market to find out whether the test results are consistent with the previous ones and enrich the study results on value-relevance.In order to get more accurate results,I will make a pooling regression and a yearly regression of the two periods,then makingan analysis.

IwillusethePrice-levelModeltoanalyzethevalue-relevance ofA-stocks amongAB-shares companies bymakinga comparison between the data of two periods and using the pooled least square method with the random time effect(the pooling regression)and the fixed time effect(the yearly regression)to test associations between accounting information and stock prices.I will use t-test to analyze whether the coefficients are at acceptable significant level.I will use R2to analyze the degree of value-relevance(increase or decrease)and use F-test to test the accuracy of the model.The t-values are at 5%significance level.

The reason that I select the AB-share companies is that companies issuing both A-stocks and B-stocks have two accounting standards(the Chinese GAAP and the IFRS). According to Bao and Chow(1999),the financial report released by firms insuring“A and B”stocks tended to have a higher quality than firms insuring only“A”stock under the Chinese accounting system.So it is the best choice to select accounting information disclosed by AB-share companies to study the value-relevance in China’s stock market.Moreover,companies issuingbothA-stocksandB-stocksusuallyhavemore experiences and more accounting practices.That is to say,when the Chinese GAAP requested to be converged with more IFRS,those companies are able to make a better reconciliation with the IFRS,which may provide more accurate accounting information in terms of earnings and book value to this study.Furthermore,considering the truth that adoption of a new accounting standard may have time effect,so I choose the period that was 3 years after the adoption ofthe newaccountingstandards.

2.Regression model of value-relevance to shareholders’equity

This paper adopted the price-per-share regression model to analyzethevalue-relevanceofaccountinginformationto shareholders’equity in the China’s A-stock market.This model was firstlyused and developed by Ohlso(1995)to study information that was reflected in the value of firms,which assuming that stock prices should reflect both the accounting information,suchasbookvaluesandearnings,andother information conveyed to the market.The model could be written as following:

3.Data and sample

The data was selected fromtwoperiods(period 1 is from2002 to 2006 and period 2 is from 2011 to 2015),and the main variables are book value per share and earnings per sharecollected from 10 year’s financial statements of 44 companies. Considering the financial data would disclose 4 months after the end of the fiscal year,I will use stock prices which were at the point of 4 months after the fiscal year(The stock prices of companies at the year of t+1,in other words,the stock prices at the point of 4 months after the fiscal year which were during 2003—2007 and 2012—2016).The new accounting policy that Chinese GAAP converged with more IFRSwas adopted in the year of 2007,so I selected accounting data which were disclosed 3 years after the adoption of the new accounting policy in order to reduce the time effects of the accounting policy.And the data was released on the internet which was secondary data and known to the public(all the data are available at http://finance.sina.com. cn/stock/).

CHAPTER 4:DATA DESCRIPTION AND ANALYSIS

1.E-viewresults oftotal regression

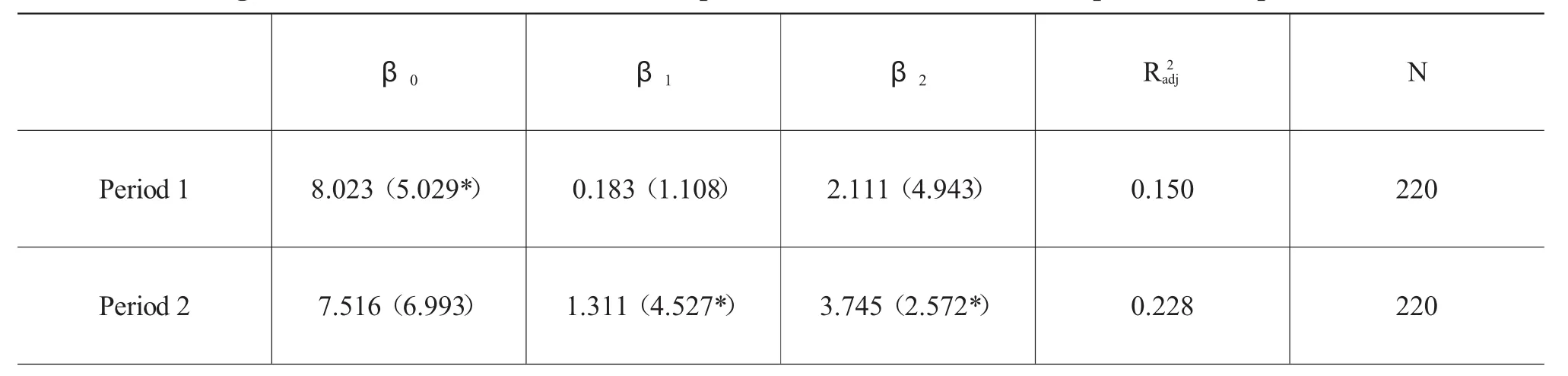

Table 1 is the results ofthe estimated price model ofperiod 1 and period 2 by pooling all observations of sample companies across time(with random time effects).I can reach such conclusion that earnings per share for both period 1 and period 2 were value-relevant,but the book value per share was not value-relevant for period 1 and it was value-relevant during period 2.Such results indicate that earnings per share reported under both Chinese GAAP and the converged Chinese GAAP(IFRS)were value-relevant in the A-stock market among AB-share companies. And the book value per share became value-relevant after the adoption of the new accounting policy in the A-stock market.In addition,the adjusted R2of period 2 was 22.8%which was more than the one during period 1(15%),in other words,accounting information duringperiod 2 was more value-relevance than period 1.That is to say,when Chinese GAAP converged with more IFRS,theA-stockswouldbecomemorevalue-relevanceamong AB-share companies,in other words,the IFRS reconciliation is value added to the determination of share prices in the A-stock market amongAB-share companies.

Table 1 Regression results of the Coefficients on price-levels model:A-shares of period 1 and period 2

Note that the Pitand Pjtrepresent the stock price of company j 4 months after the fiscal year end of period t.The numbers in the brackets represent the t-statistics;*statistical significance at 0.01 level;The BVPS and EPS represent the current fiscal year of period t.All the t-statistic results in the brackets are statistical significance at 0.05 level.

Bao and Chow(1999)studied value-relevance of B-stock market during 1993—1996 and found that earnings reported under IFRS were value-relevant and the book values were not.Although the data sample they used was different from this paper,their study was very similar with this paper’s and their study results were partial consistent with this paper’s pooling regression results.And Liu et al.(2014)used the Return Model to study the value-relevance during 1999—2005 in the AB-stock market by using AB-share companies as data sample,which found that earnings reported under both accounting standards were value-relevant and earnings reported under Chinese GAAP were more value-relevant than earnings reported under IFRS.Although they did not make a further study on the converged Chinese GAAP(with IFRS),they also reached the conclusion that earnings,no matter reported under which accounting standards,were value-relevant.

Lin and Chen(2005)studied the value-relevance ofChinese GAAP and reconciliation with IFRS in both the A-stock and B-stock market during 1995—2000,which found that earnings reported under Chinese GAAP were value-relevant and book values reported under Chinese GAAP were not value-relevant. And they also found that Chinese GAAP reconciliation with IFRS was marginally value-added to investors in the Shang Hai Exchange Stock market,in other words,earnings reported under the converged Chinese GAAP(with IFRS)tended to be more value-relevant than earnings reported under Chinese GAAP.This paper also use accounting data comes from AB-share companiesin the Shang Hai Exchange Stock market.And their study results were consistent with this paper’s.But there was no empirical evidence that book values reported under the converged Chinese GAAP were value-relevant,so I will make a further analysis on the basis of the yearly regression to get more details about the value-relevance ofbook values.

2.E-viewresults ofyearlyregression

Table 2 is the yearly regression of the coefficients of period 1,which indicated that the coefficients of earnings per share were positive at the significance level of 5%from 2002 to 2006 except for 2004,while the coefficients of book value per share are positive from 2003 to 2006 but not at a statistically acceptable level(all probabilities of t-statistics are more than 0.10).And such number was negative but also at a statistically unacceptable level(with a probability of0.407)in 2002.In 2004,the earnings per share were also not at a statistically acceptable level(the probability of the t-statistics is 0.13 which is more than 0.05).In other words,the book value reported under Chinese GAAP was not value-relevant in the A-stock market among AB-share companies during period 1 which is consistent with the results of the pooling regression we have discussed above.The adjusted R2was relatively stable from 2002 to 2006 ranging from 14.2%to 22.5%except for 2005(19.6%),which indicated that the earnings reported under Chinese GAAP were value-relevant in the A-stock market among AB-share companies during period 1. This is also consistent with the results of the pooling regression I havediscussedabove.Furthermore,accordingtotheyearly regression results,the R2increased from 14.2%to 20.3%during 2002—2004,and followed by a slight decline to 19.6%in 2005;then it increased to22.5%in 2006,which indicated that there was no regular trend on R2,but the yearly changes were relative small. So,in this paper,I regard changes on R2were relative stable during period 1.Thus,no convincing evidence was obtained to indicate whether the degree of value-relevance of A-stock has decreased or increased from2002 to2006.

Table 2 Yearly regression results of the coefficients of period 1

Note that the Pitand Pjtrepresent the stock price ofcompany i and company j 4 months after the fiscal year end of period t.And the numbers in the brackets represent the t-statistics.All the t-statistic results in the brackets are statistical significance at 0.05 level.

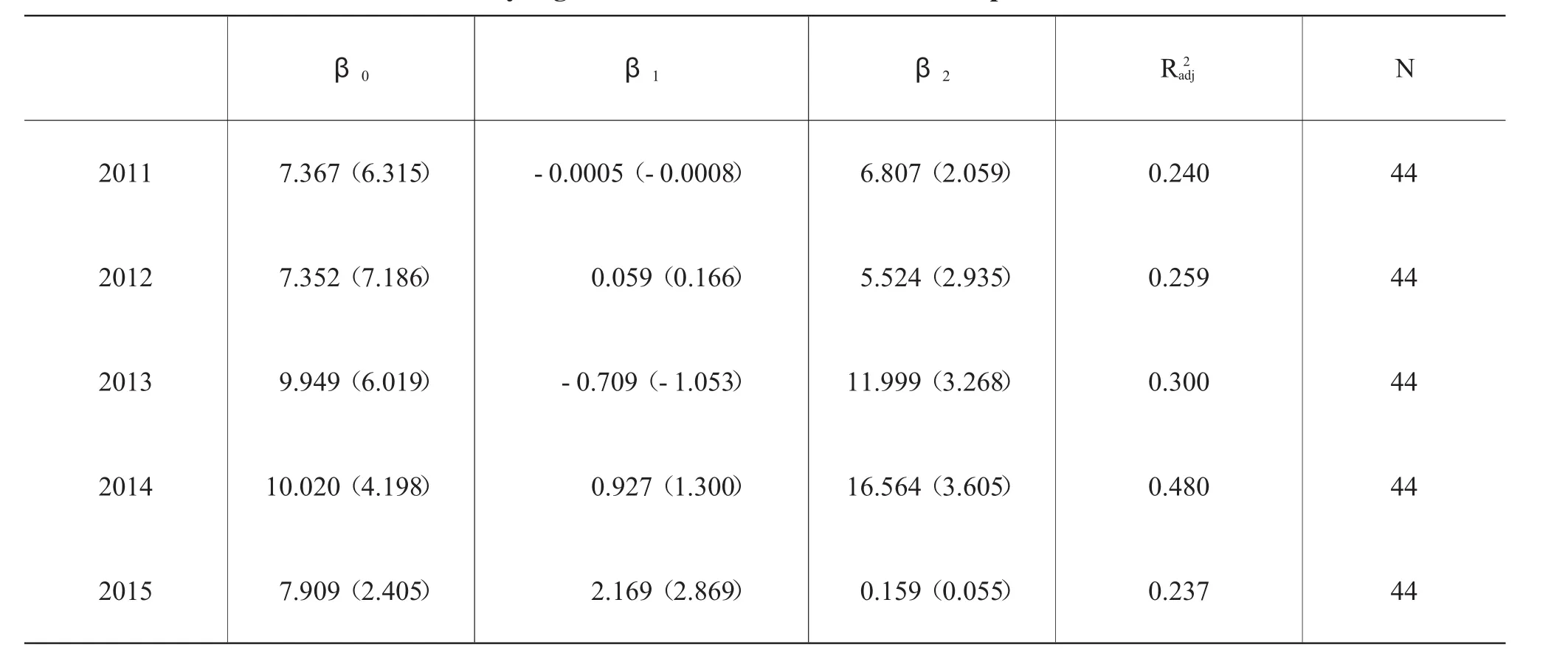

Table 3 is the yearlyregression ofthe coefficients ofperiod 2. The coefficient of earnings per share was at the significance level of 5%in 2011,and they are at the significance level of 1%from 2012 to 2014.But it was not at a statistically acceptable level(the probability of t-statistics is 0.957)in 2015.All the coefficients of earnings per share were positive.And the adjusted R2s were ranging from 23.7%to 48.0%which was higher than the ones during period 1 as a whole,which indicated that earnings per share were value-relevant from 2011 to 2014,but in 2015 earnings per share was not value-relevant,and earnings reported under Chinese GAAP were less value-relevant than earnings reported under Chinese GAAP converged with more IFRS in the A-stock market amongAB-share companies.

In addition,coefficients of book value per share were not at a statisticallyacceptable level from2011 to2014(the probabilities are more than 0.20).That is to say,book value reported under ChineseGAAPconvergedwithmoreIFRSwasnot value-relevant,which was inconsistent with the results of the pooling regression(the book value became value-relevant after theadoption of the new accounting policy).According to theaccounting data collected,the number of companies with negative earnings per share was 11 in 2004 accounting for one quarter of the total sample(44 companies),which may impose a significant impact to the results of both pooling regression and yearly regressio.

Table 3 Yearly regression results of the coefficients of period 2

Note that the Pitand Pjtrepresent the stock price ofcompanyi and company j 4 months after the fiscal year end of period t.And the numbers in the brackets represent the t-statistics.All the t-statistic results in the brackets are statistical significance at 0.05 level.

The yearly regression results confirm that earnings reported under Chinese GAAP have been reflected in A-stock prices except for 2004,and the book values were not value-relevant from 2002 to2006.And the adjusted R2increased steadily from 2011 to 2014 which was from 24%to 48%,which indicated that the degree of value-relevance of earnings reported under the converged Chinese GAAP increased from 2011 to 2014.But Lin and Chen(2005)studied the value-relevance of B-shares and found that the degree ofvalue-relevance deteriorates from 1995 to 2000.This paper’s result differs from the study results of Lin and Chen(2005),who found a decreasing trend of the explanatory power of earnings book value from 1995 to 2000.But it is consistent with the study results of Bao and Chow(1999),who alsofound an increasingtrend ofthe explanatorypower ofearnings duringthe testingperiod which was from1993 to1996.

On the whole,the adjusted R2s of period 2 were higher than thatof inperiod1,whichindicatesthatthedegreeof value-relevance increased in period 2 as a whole.This result is consistent with the pooling regression result I have discussed above.So,the yearly regression results confirm that the degree of value-relevance(earnings)increased after the Chinese GAAP converged with more IFRS.This result is consistent with study result of Liu et al.(2011),who found that the converged IFRS to Chinese GAAP imposed an important impact on accounting quality by improving the earning management and increasing the degree of value-relevance in a specific period of time which is from2005 to2008.

Although there were not enough convincing empirical evidences on the findings because fewstudies had been conducted on the basis of the same time periods and the same data sample,the results of this paper are consistent with many previous studies related to value-relevance.I will make a further discussion in order toget more accurate results in the followingpart.

3.Discussion

Overall,this paper’s results are consistent with some previous studies’results.One possible reason that the results differ fromstudy to study is that different studies selected different time periods and used different data sample.

Firstly,one of reasons that the two regression results are different on the book values maybe the crazybooming(from 2015 to 2016) in the stock market in China which led to the unreasonable stock prices.In other words,investors purchase stocks in spite of the financial situation of specific companies.The unreasonable stock price may impose significant impacts to the results of the pooling regression.In other words,it was“other information”instead of earnings per share and book value per share that lead to such unreasonable stock prices.For example,at the start of the second half of 2015,some institutions allowedinvestors to borrow money with high leverage at relatively high interest rates to invest in the booming stock market,which is one of the reasons that caused the fast increasing stock prices. Unfortunately,the stock prices crushed down at the beginning of the second half of 2016.Because of the lack of financial regulations in China’s stock market,the stock prices in 2016 becameentirelyinconsistentwitheithertheaccounting information or the economic situation.It is also known to investors that the economy in China is experiencing a structure changing and therefore the economic fundamentals are not good.But the stock market has outperformed the economy in 2016.So,this may be one of the main reasons that the earnings were not value-relevant and the book value was value-relevant in 2015 according to the results of yearly regression.Furthermore,such great deviation ofthe stock prices in 2016 value may influence the results ofpoolingregression ofperiod.

Secondly,although the stock market of China is far from standardizedcomparedwiththedevelopedcountries,the regulation in the stock market ofChina was becoming increasingly perfect over time,which may allow the Chinese GAAP to have a better reconciliation with IFRS and therefore increasing the value-relevance ofaccountinginformation.

CHAPTER 5:CONCLUSIONS

In summary,considering the previous discussion,earnings reported under both Chinese GAAP and the converged Chinese GAAP were value-relevance except for some special years(2004 and 2015).Furthermore,earnings reported under the converged Chinese GAAP were more value-relevant than earnings reported under the Chinese GAAP as a whole,and the degree ofvalue-relevance increased over time under the converged Chinese GAAP. In other words,to some extent,the Chinese GAAP converged with more IFRS can improve the degree of value-relevance.But the book value was not value-relevant under both accounting standards except for 2015.The reason for such situation may be the unreasonable stock prices in 2016 that imposed great impacts to the regression results,so I can reach the conclusion that the book value was not value-relevant under neither Chinese GAAP nor converged Chinese GAAP(with IFRS).

This paper tested a sample of AB-shares companies in the A-stockmarket.Considering thefactthatthenumberof AB-shares companies is verysmall which is less than 100 and the number of Shanghai A-stock is 44.Subject to data available the size is relativelysmall and this paper collected the accountingdata of 10 years,which may make the results more accuracy.It is expected to study companies that are not included in the AB-shares companies,which may get more details about the value-relevance in different parts ofChina’s stock market.

Despite of the limitation,this paper’s results are partially consistent with many previous studies’,Such as Bao and Chow(1999)’s,Lin and Chen(2005)’s,Liu et al.(2011)’s,Liu et al.(2014)’s.It is reasonable to get different study results for the sample periods and sample data ofdifferent studies were very different.So,according to the discussions and comparisons with previous studies,the limitations in this study did not influence this study’s validity.Future studies can be conducted to contain more companies as sample.For example,future researchers can select all companies in the A-stock market except for companies that issue both A-shares and B-shares and make a comparison between two periods to get more details about value-relevance in different stock markets.Furthermore,future studies can be conducted t o study the value relevance at the industry level.For example,future researchers can divide companies into different groups and each group represents for one industry,which can also enrich the study findings about associations between accounting information and stock prices.

REFERENCES:

[1]Agostino,M.,Drago,D.and Silipo,D.B..“The value relevance of IFRS in the European banking industry”,Review of quantitative finance and accounting,2011,(3):437-457.

[2]Chen,J.and Thomas,S.C..“The ups and downs of the PRC securities market”,The China Business Review,2003,(1):26-45.

[3]ChinaSecuritiesRegulatoryCommission(CSRC),StandardforContentAndFormatforInformationDisclosurebyPublicCompanies-No. 2:Content And Format for Annual Reports,1995.

[4]Hung,M.Y.and Subramanyam,K.R..“Financial statement effects of adopting international accounting standards:the case of Germany”,Review of Accounting Studies,2007,(4):623-657.

[5]IFRS.“IFRS application around the world”,Available on[EB/OL].http://www.ifrs.org/Usearound-the-world/Documents/Jurisdictionprofiles/China-IFRS-Profile.pdf.

[6]Lin,Z.J.and Chen,F..“Value relevance of International Accounting Standards harmonization:evidence from A-and B-share marketsin China”,Journal of International Accounting Auditing and Taxation,2007,(2):79-103.

[7]Liu,C.,Gould,G.and Burgan,B..“Value-relevance of financial statements:Evidence from A-and B-share markets in China”,International Journal of Managerial Finance,2014,(3):332-367.

[8]Peng,S.,Tondkar,R.H.,van der Laan Smith,J.and Harless,D.W..“Does convergence of accounting standards lead to the convergence of accounting practices?A study from China”,International Journal of Accounting,2008,(4):448-468.

[9]Philip P.M.Joos and Edith Leung.“Investor Perceptions of Potential IFRS Adoption in the United States”,The Accounting Review,2013,(2):577-609.

[10]Tamer Elshandidy..“Value relevance of accounting information:Evidence from an emerging market”,Advances in Accounting,incorporating Advances in International Accounting,2014,(1):176-186.

[11]Xiao,J.Z.,H.Yang,and C.W.Chow..“The determinants and characteristics of voluntary internet-based disclosures by listed Chinese companies”,Journal of Accounting and Public Policy,2004,(3):191-225.

[责任编辑陈丹丹]

The Value-Relevance of Chinese GAAP Converged with IFRS——Evidence fromthe AB-share Companies in China’s A-stock Market

LI Shi-xiang

(UniversityofSurrey Surrey,Guildford,London,UK,GU2 7JL)

This paper discussed the value-relevance in the A-stock market using accounting data disclosed by companies issuing both A-shares and B-shares simultaneously.Adopting the Price-levels Model,this paper investigated the value-relevance between Chinese GAAP and the converged Chinese GAAP(with IFRS)in the A-stock market and tested associations between accounting numbers(book value per share and earnings per share)and stock prices byusingthe pooled least square methods tostudythe twoperiods separately.Then made a comparison between the two periods(from 2002 to 2006 and from 2011 to 2015)which were before and after the adoption of the newaccounting policy(companies were requested to adopt a newset ofaccounting standards converged with more IFRS).The accounting data was regressed with the randomtime effect and the fixed time effect(the yearly regression),which found that earnings reported under the converged Chinese GAAP in the A-stock market are more value-relevant in determining the share prices of A-stocks.In other words,the IFRS reconciliation is able to improve the value-relevance of accounting information in terms of earnings.However,this paper found that book value of owner’s equity determined under both accounting standards is not value-relevant in the A-stock market among the AB-share companies under both accounting standards.Furthermore,according to the regression results,before Chinese GAAP converged with more IFRS,the degree of value-relevance was relatively stable over time.But after the adoption of the converged Chinese GAAP,earnings reported under the converged Chinese GAAP increased over time except for 2015.

value-relevance;Chinese GAAP;converged Chinese GAAP;A-stock market;AB-share companies;earnings per share;book value per share;stock prices

F230

A

1673-291X(2016)27-0056-08

2016-08-16

李世祥(1991-),男,山东临沂人,硕士研究生,从事金融学研究。

猜你喜欢

中国注册会计师(2021年9期)2021-10-14

中央财经大学学报(2021年8期)2021-08-30

现代经济信息(2020年34期)2020-06-08

时代金融(2016年29期)2016-12-05

时代金融(2016年29期)2016-12-05

商(2016年33期)2016-11-24

商(2016年27期)2016-10-17

三联生活周刊(2016年2期)2016-01-08

新会计(2014年3期)2014-06-13