Methods and empirical research on Chinese sea area resource assets value accounting

2023-11-28 11:13:28SHENJiawenGAOJinzhuQIAOLinTANLunLIYaning

Marine Science Bulletin 2023年1期

SHEN Jiawen,GAO Jinzhu,QIAO Lin,TAN Lun,LI Yaning

National Marine Data and Information Service, Tianjin 300171,China

Abstract:This paper establishes the theory and method of calculating the value of sea area resource assets,and uses the market method and the income method to calculate the expected net income of the resource assets in the sea area without right of use,and calculates the value of sea area resource assets comprehensively. The results show that the total value of resource assets in the sea area is high, mainly concentrated in the sea area without the right of use.The asset price of different areas of the sea area without right of use is related to the function type, offshore distance and sea structure.The price of sea area resource assets calculated by the market method and the income method is close to each other.The higher price of sea area resource assets calculated by the income method is related to the low marketization degree of sea area resource assets and the adjustment of the standard of sea area use fee in recent years. The classification accounting of sea area resource assets can scientifically and reasonably evaluate the expected income of sea area resource assets and calculate the value of sea area resource assets without the right of use based on the existing sea area pricing.It is necessary to carry out detailed management of marine resources assets in accordance with natural conditions and planned uses, price them scientifically and reasonably,and improve paid use and use control measures of assets,so as to ensure the preservation and appreciation of state-owned natural resources assets and promote the sustainable and efficient development of marine economy.

Keywords:sea area resource asset,value accounting,expected income

In recent years, the Party Central Committee and the State Council have attached great importance to the management of all natural resource assets.In December 2016,the State Council issued the Guiding Opinions of the State Council's Reform of the Reform of the Payment of All Natural Resources Assets for All Natural Resources which required"based on various natural resources investigation and evaluation to promote natural resources assets inspection and accounting ". In April 2019, the China Affairs Office and the State Council issued the "Guiding Opinions on Promoting the Reform the Natural Resources Asset Property System"and proposed to study on establishment of a system of natural resources asset accounting and evaluation system, carry out physical quantity statistics,and explore value accounting.

It is an urgent need and important task for natural resource assets management to carry out research on the accounting of marine resources assets, which can lay a foundation for finding out the number of marine resources assets, preparing the balance sheet of natural resources owned by the whole people, and carrying out the audit of outgoing leading cadres. The current scholars have conducted many related researches on the management of the sea area resource assets,mainly focusing on three aspects:the property rights of the sea area, the evaluation of use right price and the preparation of the balance sheet. In terms of property rights research, Cao Yingzhi et al. (2014) divided the property rights of sea area into the ownership and the right to use the sea area; Qin Lu(2006) analyzed the problems existing in the sea area right transfer system and put forward some suggestions for improvement by referring to the land transfer system and foreign sea area right transfer system. In terms of price assessment, Wang Miao et al.(2007) proposed the method of measuring sea area resource assets from three aspects:unit value, quantity and mixed aspects; Li Yanan et al. (2009) established the price evaluation method and model; Wen Demei et al. (2014) sorted out the research results of the field of resource price assessment, and summarized the scope of the application of various discounted cash flow methods;Shen Jiawen et al.(2018)established the method of benchmark price of sea area;Song Xiefa et al.(2018) carried out the empirical analysis of cost laws and income methods in the sea area assessment.In terms of the balance sheet,Fu Xiumei et al. (2017) designed a technical framework for marine biological asset liabilities; Wang Tao et al. (2017) (2021) established accounting framework of three types of sea area resource assets. Li Yanping et al. (2018) defined the accounting scope of marine assets and liabilities and designed the framework of Marine balance sheet with priority accounting scope.

Through many years of research and exploration, China has established a relatively perfect sea resource management system and a top-down management mode. With the reform of natural resources property right system proposed in recent years, the management of marine resources as assets has become an emerging research content.As for how to define marine resource assets, improve property rights system, carry out asset accounting and assessment, the academic research is mainly focused on natural resource assets. In terms of rights research, definition of natural resources assets and liabilities and balance sheet framework, there are few researches on accounting methods and technologies of marine resources assets, and empirical studies are relatively lacking.Different from the evaluation method of use right price, the value accounting of sea area resource assets covers a larger scope and contains relatively more contents. The current sea area management means dominated by paid use cannot meet the technical requirements of the value accounting of sea area resource assets, and cannot solve the problems of unclear sea area resource background and unknown account. It is difficult to form effective support for the further development of marine resource asset management.In view of this,this paper takes marine resources assets as the object to carry out the value accounting research.Based on the development and utilization status of marine resources assets and the expected income of the assets, it establishes the technical route and method of classifying the value of marine resources assets based on the physical quantity accounting. Finally, the accounting results are summarized and analyzed. So as to reflect the total value and distribution of marine resource assets, in order to provide theoretical and technical support for natural resource assets management, such as the inventory and accounting of natural resource assets, the preparation of natural resource balance sheet,and the audit of leading cadres’leaving office.

1 Theoretical research

This study carries out theoretical analysis and methodological research according to the framework of environmental economy comprehensive accounting system(SEEA 2012)and the principle of asset evaluation.

1.1 Sea area resources assets

The sea area provides space for economic activities and serves as an important territorial resources together with land. It falls under the category of environmental assets in the SEEA and should be included in environmental economic accounting. Sea area resources assets can be defined as those marine space resource assets with scarcity and usefulness (including economic, social and ecological benefits) that can bring benefits to the country at present or expected in the future.

1.2 Value of sea area resources assets

China implements a system of compensated use of sea areas. The state, as the owner of sea area resources assets,invests the resources assets into social and economic activities by transferring the right to use sea areas, and collects fees for the use of sea areas to gain profits.The value of sea area resource assets includes the value of the right to use generated by the transaction of the right to use the sea area and the expected value of the right to use the sea area with clear and measurable property rights, which is represented by the sum of the income or the present value of the potential income from the transfer of the right to use the sea area according to the maximum years.

1.3 Sea area resources assets accounting

The accounting of natural resource assets is mainly divided into material quantity accounting and value quantity accounting, which adopts the methods of classification before synthesis, material object before value, flow before stock. The accounting of sea area resources assets is the overall accounting and analysis of the actual quantity and value of sea area resources assets at a certain time (or moment) and space based on the investigation and statistics of sea area resources.

1.4 Sea resource assets value accounting

The value accounting of sea resource assets is based on the calculation period (or time point) of various types of resource assets value on the basis of physical accounting.The value of sea area assets shall follow the principle of marketization, and use market value to estimate the assets. If the asset does not have a measured market value, the net current value method is used for valuation (Wang Tao et al., 2018). According to the net current value method, the expected pure income of assets needs to be discounted and restored to the current price. The capital asset pricing model is used to calculate the discount rate. The discount rate of sea area resources assets consists of risk-free rate of return and risk-return rate.The calculation formula is as follows:

In the formula:rrepresents the discount rate of a certain asset;rfrepresents a risk -free return;rmrepresents a market portfolio yield, that is, the average yield of all assets in the market; (rm-rf) represents the difference between the average yield and the risk-free interest rate,or the risk premium;β represents the market risk coefficient of the asset.

The average yield of Treasury bonds with maturity of more than 10 years (4.17%),the accounting base date,is selected as the risk-free yield.A comprehensive analysis was made based on factors such as adjustment of sea area funds and asset management level,and 0.5 was scored by experts as the risk coefficient.The social discount rate (8%) in the Economic Evaluation Methods and Parameters of Construction Projects was taken as the average return on assets,and the discount rate was determined to be about 6.08%.

Calculate the sequence of the annual correction through comprehensive amendments to the formula:

In the formula 2,Yrepresents yearly revision coefficient;rrepresents the discount rate;nrepresents the highest use period of the sea area.Sea resources asset prices are:

In the formula 3,Prepresents the price asset price of the sea area;prepresents the innocent income of the year of the sea resource assets.

1.5 Principles of expected returns

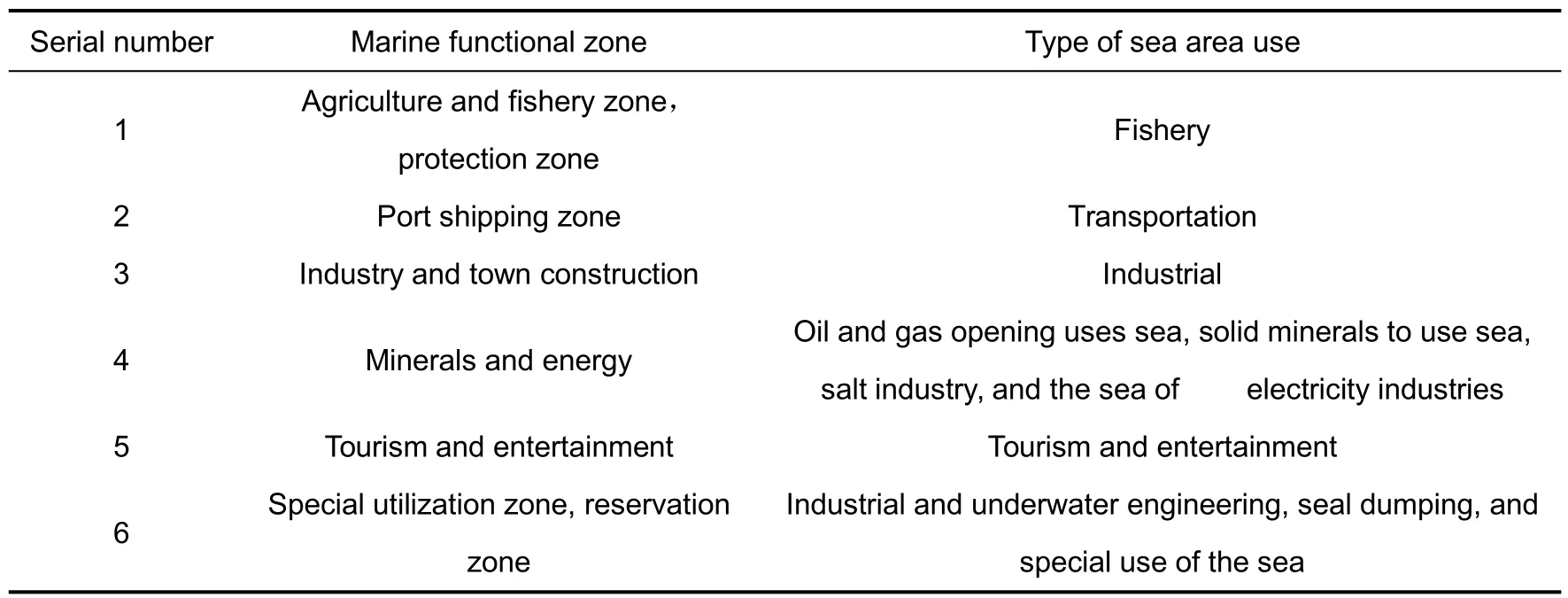

For the sea area resources assets whose right to use has not been traded, that is,the assets have not been transferred,and the net income of the assets cannot be obtained through the transfer price, the expected use of the sea area resource assets can be determined by sea planning and use control, thus the expected value of the sea area resource assets without the right to use the sea area resource assets can be estimated.Marine functional zoning is an integral, fundamental and binding document for the development, control and comprehensive management of marine space.According to the location of the sea area,natural resources,environmental conditions and the requirements of development and utilization, the sea area is divided into different types of basic functional areas of the sea area.According to the natural attributes of the sea area and the degree of social demand, the optimal function of the sea area is determined with the goal of maximizing the economic,social and ecological benefits of the sea area.Marine function zoning divides the sea area into different basic marine functional zones,which is the spatial guide for marine development activities and the main basis for marine use approval.It can reflect the future direction of marine development and utilization. According to the functional types and control requirements of marine function zoning, it should be connected with the current marine area use classification system(Tab.1).The value of sea area resources assets is calculated based on the expected net income of sea area resources under different development and utilization conditions.

Tab.1 Expected type of sea area use of marine functional zonation

2 Technical method

2.1 Accounting range

The asset scope in the System of Environmental Economic Accounting (SEEA 2012)includes all economic territories that provide all resources and space for economic activities.Land as an environmental economic asset has also been extended to areas such as coastal waters and a country's exclusive economic zone(EEZ).

Land as an environmental and economic asset has also been extended to areas such as coastal waters and exclusive economic zone.According to the accounting scale,which is consistent with our current sea area administrative management system, the accounting of sea resources assets can be divided into macro accounting, mesoscale accounting and micro accounting. Macro accounting refers to the national-scale asset accounting, and the scope of accounting is the jurisdiction of country; the mid-view accounting refers to the provincial as the subject, and the scale of accounting is the provincial jurisdiction.

2.2 Accounting unit

The base map is extracted and cut, and the base map is segmented, integrated and extracted according to ownership information, reclamation survey, functional zoning and boundary demarcation of sea area.The map pattern is taken as the accounting unit.

2.3 Accounting classification

Based on the definition of sea area resources assets and the methods of environmental economic accounting, the right to use resources assets in sea area is divided into two categories: obtained right of use and not obtained right of use. Under the current sea area management system in our country, the rights-to-use areas refer to the areas where certificates of the right to use sea have been issued or approved for sea use.There are clear ways and types of sea use,and the rights-to-use areas have stable income.The sea area without right to use refers to the sea area without the certificate of the right to use the sea area or the approval for the use of the sea area, and only the construction of the reclamation project in the early stage or the sea area is completely vacant.According to the development, utilization and construction, the sea area without right to use the sea area can be further divided into two categories: developed and undeveloped. Developed area refers to the sea area with the land reclamation completed but without right to use the sea area. Compared with the undeveloped sea area, the property of land assets and relatively high economic value should be considered as a separate category of accounting;Undeveloped area refers to the undeveloped land sea area without right to use.Compared with the reclamation construction, the resource assets in this type of sea area have not been developed in the early stage,and are relatively vacant with relatively low asset value.

2.4 Accounting method

Under the framework of SEEA2012, the net income of the right to use sea area resource assets is estimated by combining environmental economics theory and asset evaluation method,and the value of sea area resource assets is classified according to the income or potential income from the right to use sea area, mainly including market comparison method,income reduction method, cost method and residual method (Tab.2).The transaction price of the right to the use of sea area is taken as the net income of the asset,and the transaction price is amended as the asset price of sea area with the right to use.According to the development and utilization status and income of the resource assets in the sea area, the market method and income method are adopted to calculate the expected net income of sea area without right to use, and the value of the sea area resource assets is calculated comprehensively.

2.4.1 Sea area resource assets with right to use

According to the usage and the service time of the sea area, the transaction price is revised into the price of the sea area resources assets with right to use under the connotation of accounting.

2.4.2 Sea area resource assets without right to use

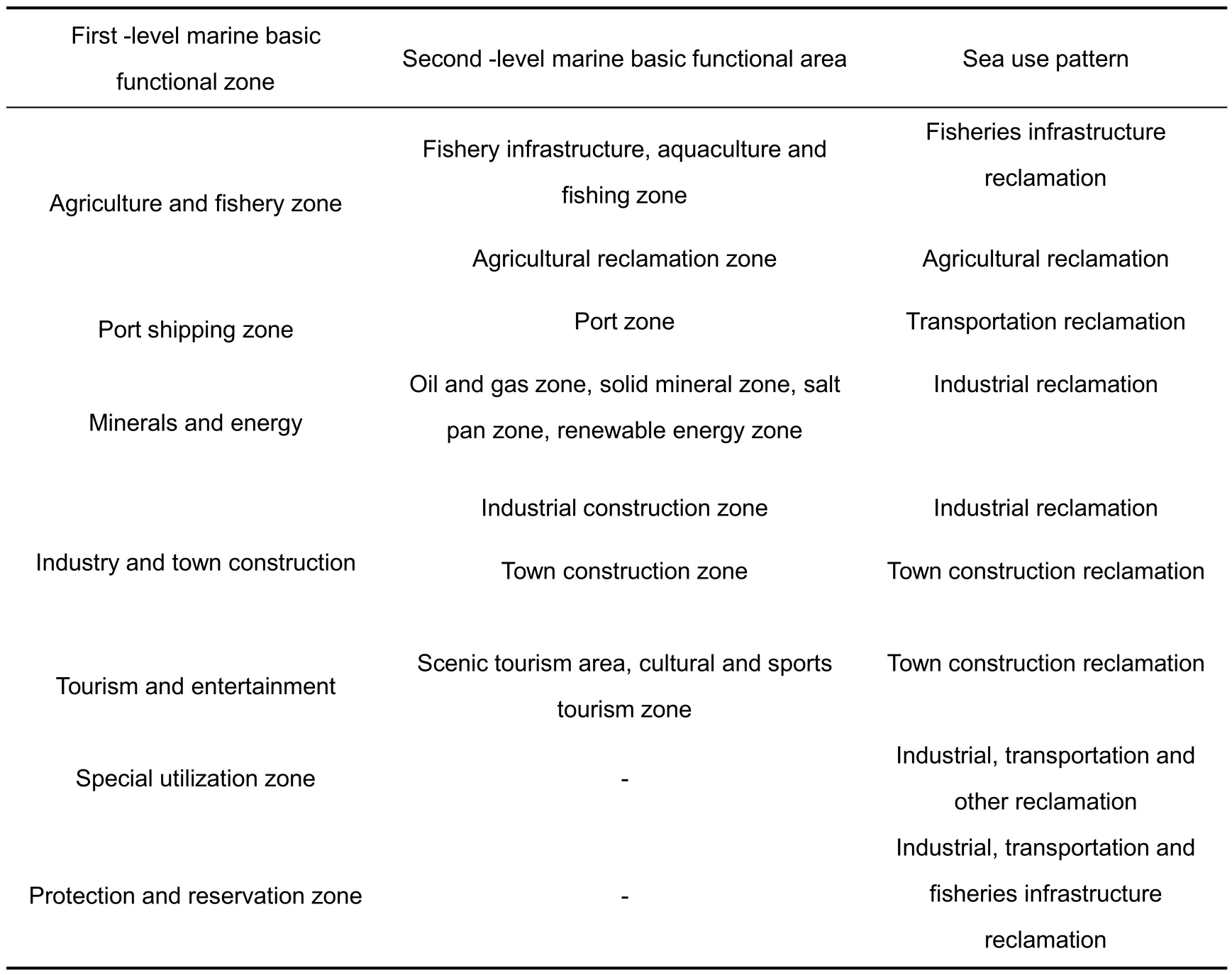

Under the principle of expected return, according to the control requirements of marine function zoning,the expected use of the sea area without right to use is judged,and the area with homogeneous price is established according to the planned use, resource endowment and expected income of assets.Using the marketing method,the sea projects with the same usage and intended use in the homogeneous area are taken as the comparison samples of the sea area without right to use. Based on the sample screening and the calculation and correction of the net income of the right to use,the average price of the sample is used to calculate the price of sea area without right to use. The income method is adopted, and the sea area use charge standard is used as the calculation basis of expected income. For the land reclamation area without right to use, the current sea area use charge standard is further divided according to the specific use type of reclaimed land. By combing the types and the control requirements of functional zones, it can be judged that the sea is expected to be mainly used for various functional zones(Tab.3).The expected usage of land reclamation area without to use is corresponding to the classification of sea area use charge standard.

Tab.3 Marine functional zonation corresponds to the usage category of reclamation

The sea area use charge standard shall be regarded as the expected net income of the land reclamation area without right to use.

For the unreclaimed sea area without right to use,it is difficult to determine the usage of sea only through marine functional zoning, and it cannot be classified with the sea area use charge standard. By analyzing the expected use and usage structure of the sea area,the price of the area is established based on sea area use charge standard of different types and modes of sea area.At the same time, the State has implemented the policy of strict management and control of reclamation, strictly controlled new land reclamation,tightened the examination and approval of reclamation projects (State Council, 2018), and screened out those projects that are reclamation projects or land reclamation projects by sea.If there is no use of sea in the area consistent with the intended use or the use of sea projects are rare, considering the restrictions of the use of sea conditions, other open use of sea area use charge standards are adopted for amended,as the area price.

3 Empirical analysis

3.1 Scope of the study

This paper takes the scope of marine functional zonation as the base, and uses the market method and income method to measure the expected net income of sea area resources assets without right of usage, and carries out comprehensive accounting of the value of China’s sea area resource assets.

3.2 Connotation definition

Based on the definition of the value of sea area resource assets, the right to use asset is the right to use the sea area, and the right period is set to 15 years, 25 years and 50 years in combination with the type of sea area use or intended usage according to the Law on the Administration of the Use of Sea Space, and the accounting period is December 31,2020.

3.3 Data sources

This paper collects the ownership data, boundary survey data, marine functional zonation data and other data for homogeneous area division and value accounting, and produces a data format for base map processing and value accounting,the data types and sources are shown in Tab.4.

Tab.4 Data types and sources

Tab.5 Price of sea area resource assets without right to use by market comparative method Unit:million yuan

Tab.6 Price of sea area assets without right to use by income restoration method Unit:million yuan

Tab.7 Price of sea area assets with right to use Unit:million yuan

Tab.8 Total amount of sea area resource asset Unit:million yuan

3.4 Technical Route

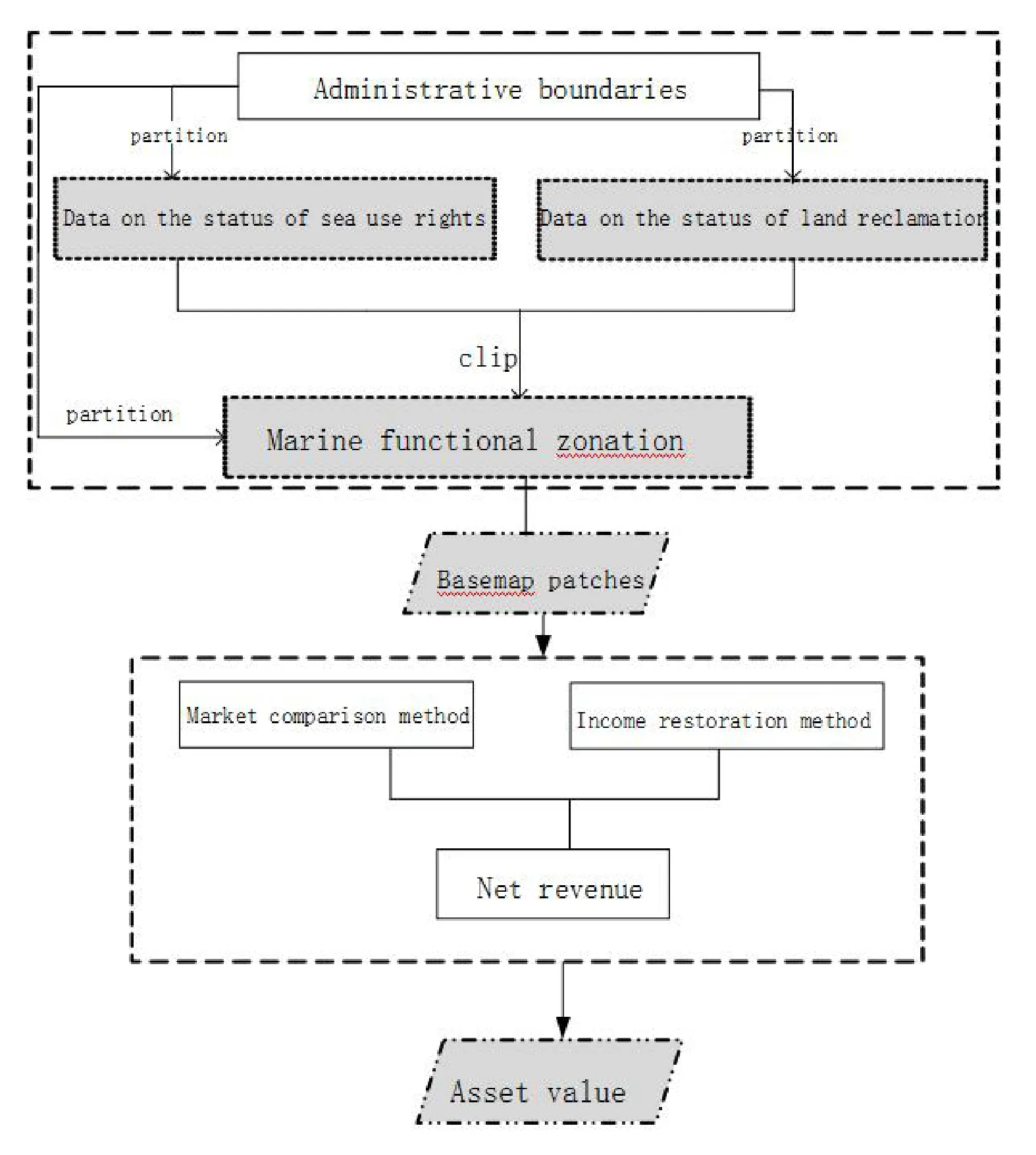

The base map data are superimposed and attribute information is integrated to carry out value accounting by classification. On the basis of marine functional zoning,homogeneous areas of sea area resource assets are divided.The expected net income of resource assets in the sea area without right to use is calculated by the market method and the income method. The price of each homogeneous area is established, and the transaction price of resource assets in the sea area with right to use is revised to comprehensively calculate the value of sea area resource assets.

Fig.2 Technological route

3.5 Accounting for the value of marine resource assets

Marine functional zonation divides the sea area into different basic marine functional areas, and divides coastal and offshore functional areas according to the differences between the sea area near the coastline and other sea areas in terms of resource and environmental characteristics, development and utilization status and management requirements. The functions include agriculture and fishery, port shipping, industry and town construction, minerals and energy,tourism and entertainment zone.According to the requirements of sea area location, natural resources, environmental conditions and development and utilization, the national sea area resource assets are divided into 142 homogeneous areas without reclamation,and the land reclamation areas are divided into 6 homogeneous areas according to the distribution and intended usage.

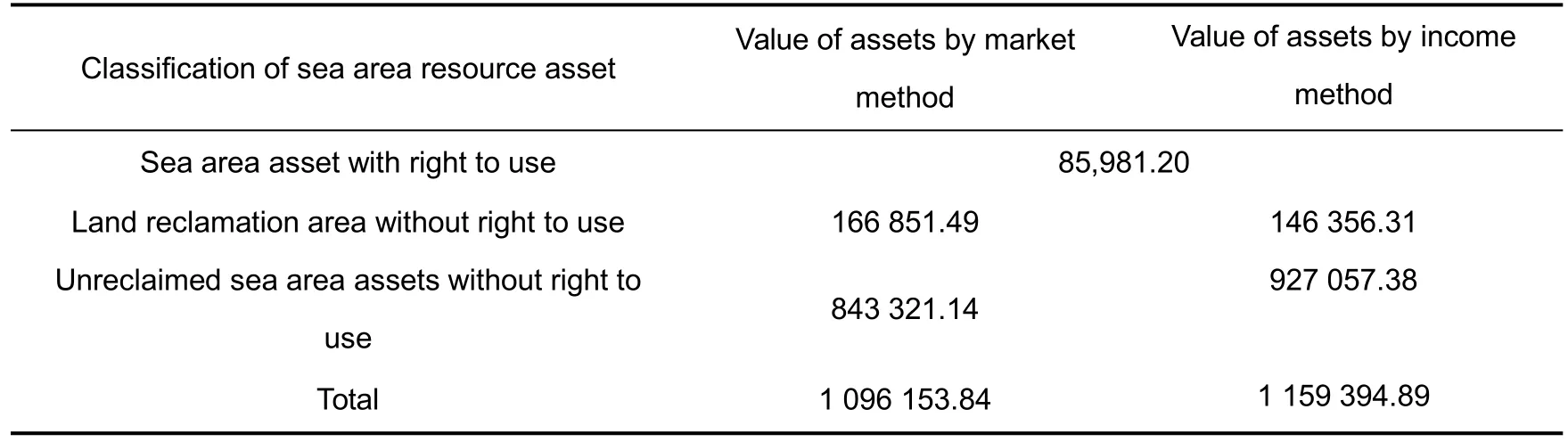

The marketing method was adopted to collect the sea projects in the area in the last five years as samples to establish the homogeneous area price. For the land reclamation area without right to use, to collect the land reclamation projects in the past five years as comparison samples,and the price of each homogeneous area is between 172 700-930 400 yuan/hm2.Among them, areas with higher price are mainly concentrated in the tourism and entertainment zone and port shipping zone,while the lower areas are mainly concentrated in the agricultural and fishery zone and special utilization zone. According to the homogeneous area price, the total amount of land reclamation area without right to use is 166 851.50 million yuan, of which the highest provincial price is 31 621.57 million yuan in Shandong, and the lowest is 12.32 million yuan in Shanghai. For unreclaimed sea area without right to use,projects in the past five years were collected as comparative samples.After the sample screening (Tab. 1) and the evaluation and correction of the right to use price, the price of each homogeneous area is between 0.10 - 748 700 yuan/hm2. The higher price areas are mainly concentrated in industry and town construction zone and tourism and entertainment zone. The lower areas are mainly concentrated in agricultural and fishery areas and protected zones. According to the area price, the total amount of land reclamation zone without right to use is 843 321.14 million yuan, of which the highest price is 163 193.93 million yuan in Zhejiang,and the lowest price is 29 059.07 million yuan in Tianjin. By market comparative method, total amount of sea resource assets without right to use is 1093 908.87 million yuan.

The income method was used to extract the information of the categories and functional divisions of land reclamation area without right to use, and calculate the value according to the sea area use charge standards.The total price of sea area without right to use is 146 356.31 million yuan. Among them, the highest price of land reclamation area without right to use is 23 964.24 million yuan in Liaoning Province, and the lowest price is 117.34 million yuan in Shanghai. According to the function of different areas, the proportional structure of sea use status, and the grades of sea areas, etc., prices of 87 homogeneous areas were initially established, and prices of 56 areas were established according to the minimum standard for open sea use in homogeneous areas with few sea use projects and less than 5%use of the sea area.The price of each homogeneous area is between 5 100 - 331 300 yuan/hm2, which is obviously affected by the marine functional zonation, sea use structure and offshore distance. Among them, the prices of areas with similar functions are relatively concentrated, and the areas with higher prices are mainly coastal industrial and town construction zone,whereas the lower areas are mainly offshore agricultural and fishery zone.Total amount of sea area assets without right to use is 927 057.38 million yuan, of which the highest price in Shandong Province is 234 691.21 million yuan,and the lowest price in Tianjin is 15 266.84 million yuan.

After extracting the national sea area right confirmation data and revising the transaction price with the sea type and collection method, the total amount of resources and assets in the national sea area is 85 981.20 million yuan. Among them, the highest asset price of sea area with right to use in Shandong is 1 957 692.24 million yuan, the lowest in Shanghai is 222.791 6 million yuan.

Using the market method, the total value of sea area resources assets is 1 096 153.84 million yuan,among which the value of unreclaimed sea area without right to use is the highest,which is 84 332 144.16 million yuan,accounting for 76.93%of the value of sea area resource assets in China, followed by the value of land reclamation area without right to use, which is 166 851.49 million yuan. The value of sea area with right to use is the lowest,which is 85 981.20 million yuan,accounting for 7.85%.Using the income method, the total value of sea area resource assets is 1 159 394.89 million yuan, among which the value of unreclaimed sea area without right to use is the highest, which is 927 057.38 million yuan, accounting for 79.96% of the total value of sea area resource assets.The value of land reclamation area without right to use is 146 356.31 million yuan.Accounting for 12.62%, the value of sea area with right to use is the lowest, which is 85 981.20 million yuan,accounting for 7.42%.

4 Conclusion and discussion

4.1 Conclusion

Under the framework of System of Environmental Economic Accounting (SEEA 2012), this paper establishes the theory and method of macro-accounting for the stock value of sea area resource assets in combination with the asset valuation method, and takes China's sea area resource assets as an example for empirical analysis. The conclusions are as follows:

(a) Based on the current situation of sea use and the pricing situation of sea area in China, the income method and market method can be applied to calculate net income of sea area resource assets without right to use, so as to provide support for the comprehensive accounting of sea area resource assets.Accounting by market method can more accurately reflect market supply and demand and price fluctuations based on the market price of China’s sea area use rights.The calculated net income of sea area without right to use can reflect the price level of sea area resource assets more accurately. The income method can be connected with the current sea pricing. Under the background of the current allocation of sea use right based on application approval and not highly marketized, the risk of market fluctuations can be internalized, and the asset prices calculated have more stability and authority;

(b) The total assets accounted by the market method and the income method are similar, which is closely related to the market-oriented development degree of resource assets and the resource pricing policy. The high price of land reclamation assets without right to use accounted by the market method is mainly due to the relatively common market-oriented transfer of land reclamation and the high price of market-oriented samples,which causes the price of the assets to be higher than the sea area use charge standard under the same conditions.However,the price of sea area assets without reclamation and right to use accounted by the market method is lower than the price accounted by the income method, mainly due to the low market-oriented transaction level of the overall sea area and the increase in the sea area use charge standard since 2018.

(c)The value of China's sea area resource assets is high,mainly concentrated in the sea area without right to use. The early understanding of the value of resource assets is insufficient,the market is not developed perfectly,and the standard for the collection of sea area use fee is low. Sea area use right obtained through the market-oriented way is few.Thus, the value of sea area resource assets calculated by price of the use right revision is much lower than the value of resource assets without the use right.The value of sea area without right of use is high, and the total value fluctuates significantly with the price of homogeneous area.

4.2 Discussion

At present, the academic research on the value of natural resource assets mainly focuses on the evaluation of use right price and theory and framework of the balance sheet.There are few empirical studies on how to carry out the asset accounting, and no unified method and cognition has been formed yet. The accounting system of natural resource assets has not been established yet.

(1) When carrying out the accounting of sea area resources assets, the principle of clear ownership and legal use should be adhered to, the existing various price standards and the status quo of sea use should be fully referred to. The factors affecting the value should be internalized on the basis of scientific accounting,and the sustainable and stable income from the use right or potential income should be taken as the basis for the asset value. We should strengthen the detailed management of land reclamation and sea area resource assets without right to use,scientifically calculate their value,and prevent the loss of state-owned resource assets.

(2) The expropriation of sea area use charge is an important means to realize the ownership rights and interests as the owner of sea area resource assets. The standard of sea area use charge can be used as the main basis for the transfer price of the right to use the sea.But the standard for setting the price according to the sea use method is similar to the"floor area ratio"in the land,which is difficult to connect with the planned usage,thus is not suitable for measuring the price of vacant sea area resource assets. By dividing homogeneous area, combining market method, income method and other methods to calculate the net income of assets, and establishing homogeneous area price, we can scientifically calculate the value of sea area resource assets without right to use.

(3) The calculation method of sea area resources assets established in this study is suitable for macro and meso-scale accounting of sea area resources assets. Provinces and cities can divide homogeneous area according to the accounting scope, usage of sea area and planning control.Based on the division of homogeneous area,they can verify the expected income and calculate the value of sea area resource assets without right to use.

(4)As the main carrier of sea-related economic activities, the accounting of sea area resource assets is of great significance to finding out the background of property of China's natural resource assets,promoting the reform of the property rights system in marine field,preventing the loss of state-owned assets, and promoting the sustainable development of marine economy.

Marine Science Bulletin2023年1期

Marine Science Bulletin2023年1期

- Marine Science Bulletin的其它文章

- Characteristics of storm surge disasters along Fujian coast in recent 10 years

- Leveraging open source software and programming best practices for sustainable web applications in support of marine data sharing-BCO-DMO case

- Design and development of international buoy data operational processing system

- Isolation and purification of diketopiperazines with antialgal activity from marine macroalgae

- Data analysis of HF surface wave radar in Zhoushan sea area

- Priority conservation pattern and gaps of Guangxi sea area based on systematic conservation planning