绝对破产下的总负持续时间

2011-01-04 02:08孙国红裴新年张丽维

天津师范大学学报(自然科学版) 2011年1期

孙国红,裴新年,李 慧,张丽维

(1.天津农学院 基础科学系,天津 300384;2.中共天津市委党校 基础课教研部,天津 300191;3.南开大学 数学科学学院,天津 300071)

绝对破产下的总负持续时间

孙国红1,裴新年2,李 慧3,张丽维3

(1.天津农学院 基础科学系,天津 300384;2.中共天津市委党校 基础课教研部,天津 300191;3.南开大学 数学科学学院,天津 300071)

考虑常利率下的贷款复合泊松模型,讨论了在绝对破产情况下的总的负持续时间,利用马氏性推导并解出总的负持续时间的拉普拉斯变换.

古典风险模型;绝对破产;负持续;借款利息

1 Introduction

Most companies request a loan with some debit interest to support debit when the surpluses turn negative.Managers hope that the surpluses will return to a positive level in the future and they also pay attention to the speed of recovery and the value of loan.The total duration of negative surplus is investigated,namely the surplus will stay below zero until absolute ruin during the time.It not only can help manager evaluate the company and find out the speed of recovery and the value of loan,but also can help creditor measure the insurer’s default risk.

C.Zhang et al(2002)investigated the compound Poisson process that is perturbed by diffusion and derived formulas for the Laplace transform,expectation and variance of total duration of negative surplus[1].M.Song et al(2007)researched negative surplus of the compound Poisson process with constant interest and continuous process[2].By researching the hitting time of the surplus process with constant interest when the initial value is less than the hitting level,J.He et al(2009)obtained the Laplace-Stieltjes transform (LST,simply)of the total duration of negative surplus when absolute ruin does not occur[3].The LST of the total duration of negative surplus is investigated when absolute ruin occurs.

The compound Poisson risk model with debit interest is described by

{N(t),t>0}is a Poisson process with parameterλ.{Xn,n≥1}(representing the sizes of claims and independent of{N(t),t>0})is a sequence of positive,independent and identically distributed random variables with common distribution functionF(x)which satisfiesF(0)=0and has a positive meanμ<∞.

Let the ruin time be

Define the ultimate ruin probability to beψ(u)=P(T<∞|U(0)=u)=Pu(T<∞).Obviously,whenu<0,ψ(u)=1.

WhenU(t)≤-c/δ,the surplus is decreasing and is no longer able to be positive,and so absolute ruin occurs at that moment.Then define the absolute ruin time to be

2 The LST of TT

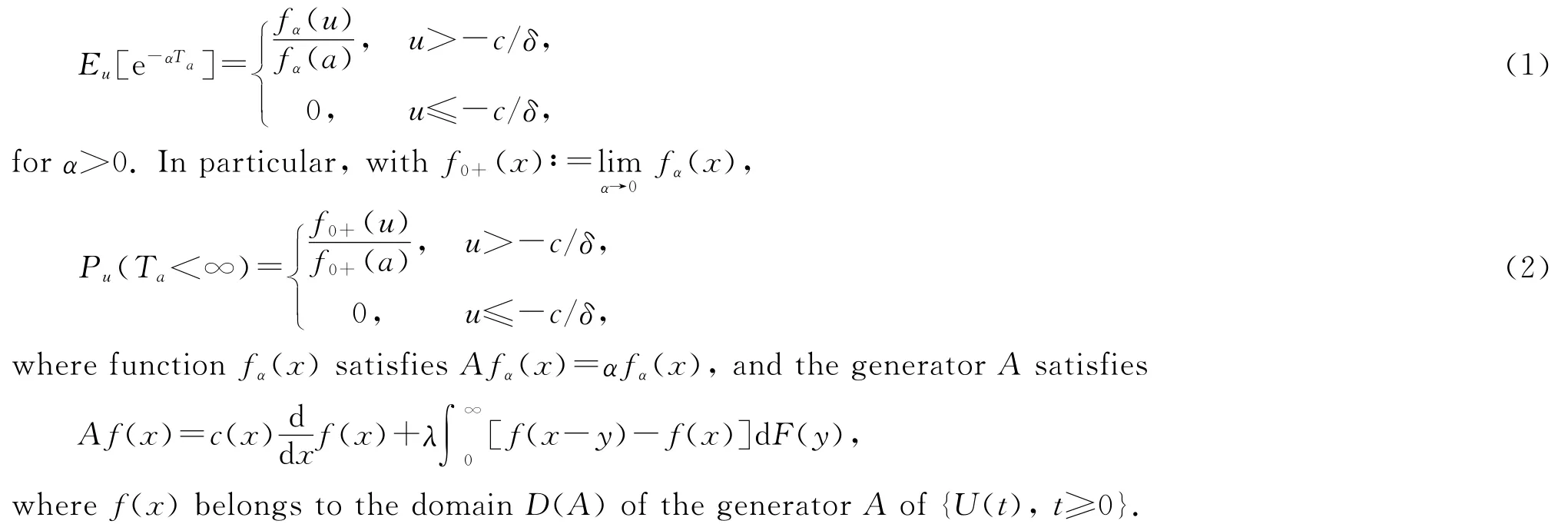

Lemma[3]The LST of the time to hita,given that initial surplusu<ais given by

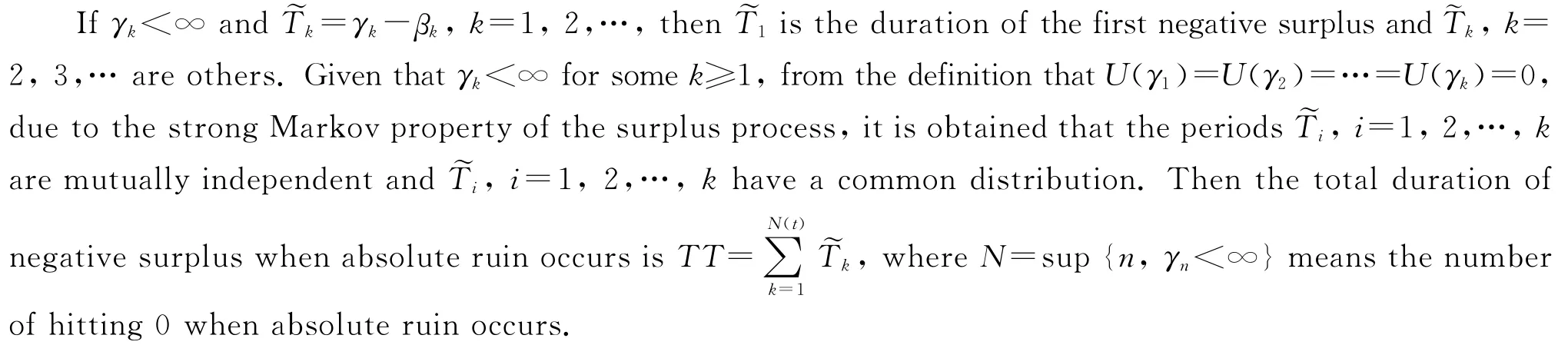

Definition Define the sequence of zero points on the time scale of the surplus process as follows:

β1=inf{t>0:U(t)<0},β1=∞if the set is empty,

γ1=inf{t>β1:U(t)=0},γ1=∞if the set is empty.In generally,fork=2,3,…,recursively define

βk=inf{t>γk-1:U(t)<0},βk=∞if the set is empty,γk=inf{t>βk:U(t)=0},γk=∞if the set is empty.

Obviously,β1=T.There are four conditions needed to discuss as shown in Figure 1.

Figure 1 Diagram about four conditions

Theorem 1 Whenu≥0,the numberNof hitting 0when absolute ruin occurs has the following probability function:

Whenn≥1,from definition and the strong Markov property,it follows that

Remark:In the case ofδ=0andc>λμ,the equationa(u)=ψ(u)is obtained,and soPu(N=n)=0.This shows that whenδ=0,absolute ruin is impossible to happen and its probability is 0.

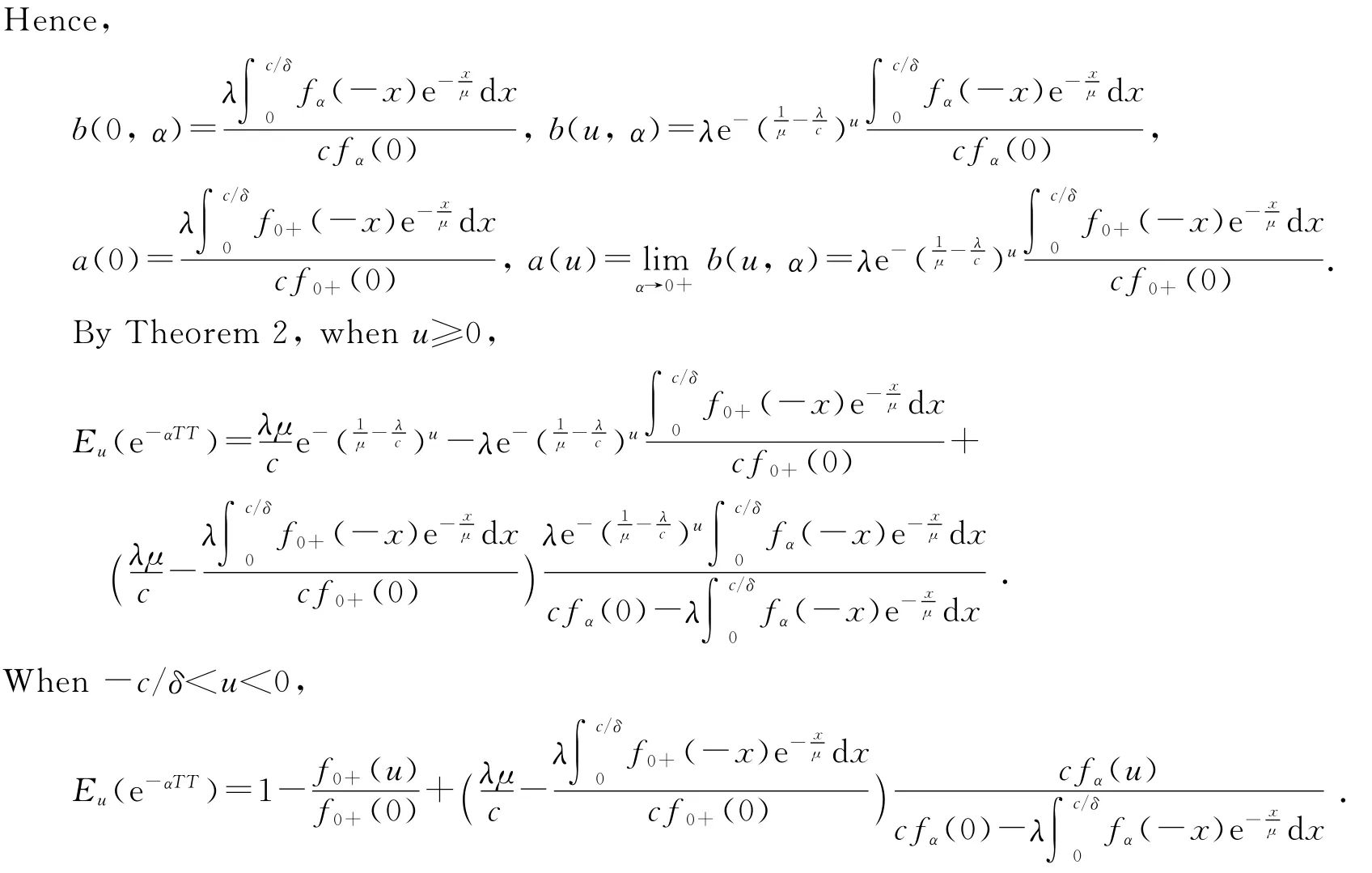

Theorem 2 Forα>0,whenu≥0,the LST ofTTis given by

3 Examples

[1] Zhang C,Wu R.Total duration of negative surplus for the compound Poisson process that is perturbed by diffusion[J].Journal of Applied Probability,2002,39:517-532.

[2] Song M,Wu R.Total duration of negative surplus for the risk process with constant interest force[J].Stochastic Analysis and Applications,2007,25:1263-1272.

[3] He J,Wu R,Zhang H.Total duration of negative surplus for the risk model with debit interest[J].Statistic and Probability Letters,2009,79:1320-1326.

[4] Gerber H,Goovaerts M,Kass R.On the probability and severity of ruin[J].ASTIN Bulletin,1987,17:151-163.

Total duration of negative surplus under absolute ruin

SUNGuohong1,PEIXinnian2,LIHui3,ZHANGLiwei3

(1.Department of Basic Science,Tianjin Agricultural College,Tianjin 300384,China;

2.Department of Basic Courses,Party School of CPC Tianjin Municipal Committee,Tianjin 300191,China;

3.School of Mathematical Sciences,Nankai University,Tianjin 300071,China)

The compound Poisson risk model with debit interest is considered,and the total duration of negative surplus when absolute ruin occurs is discussed.By the strong Markov property of the model,the Laplace-Stieltjes transform of the total duration of negative surplus is obtained.

classical risk model;absolute ruin;duration of negative surplus;debit interest

date:2010-04-10

Financial support from National Basic Research Program of China(973Program,2007CB814905),the National Natural Science Foundation of China(10871102)and the Natural Science Foundation of Tianjin(08JCYBJC02200)

's biography:SUN Guohong(1967—),female,associate professor,direction of research:probability and statistics,multivariate statistical analysis.

O174.5;O211.6

A

1671-1114(2011)01-0021-04

(责任编校 马新光)

猜你喜欢

古今农业(2022年1期)2022-05-05

大学生(2021年9期)2021-09-28

——社会科学教研部

国家教育行政学院学报(2020年7期)2020-09-03

纺织科学研究(2020年1期)2020-05-21

广东党史与文献研究(2020年6期)2020-03-03

中国校外教育(2019年3期)2019-01-31

中等数学(2018年9期)2018-11-10

中共乐山市委党校学报(2017年3期)2017-10-21

咸阳师范学院学报(2016年6期)2017-01-15

人间(2015年10期)2016-01-09

- 天津师范大学学报(自然科学版)的其它文章

- 可微C0-半群的谱

- OⅡ空位BaZrO3晶体的第一性原理研究