May 2019

2019-06-17 16:56:26

China Textile 2019年5期

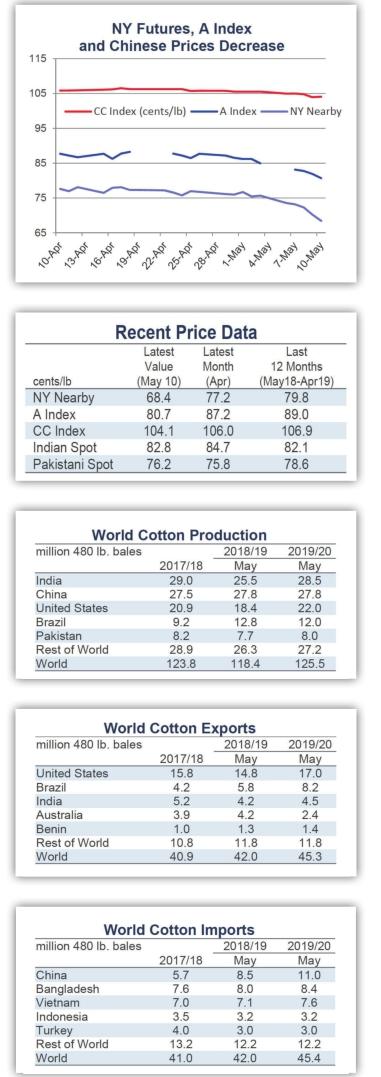

Recent price movement

Nearly all benchmark prices moved lower over the past month.

Prices for the July NY futures contract fell from values near 77 cents/lb in mid-April to those below 70 cents/lb most recently.

The A Index fell by about the same amount, with values decreasing from 88 to 82 cents/lb.

Losses for the China Cotton Index(CC Index 3128B) were smaller. Levels decreased from 106 to 104 cents/lb in international terms but were stable in domestic terms (near 15,600 RMB/ton).

Indian cotton prices (Shankar-6 quality) decreased slightly, dropping from 85 to 83 cents/lb in international terms but were also stable in domestic terms(near 46,000 INR/candy).

Pakistani prices were stable in international (near 76 cents/lb) and domestic terms (near 8,800 RKR/maund).

Supply, demand, & trade

This USDAs May supply and demand report is the first to feature a complete set of forecasts for an upcoming crop year. The figures for 2019/20 suggest growth in both global cotton production and mill-use. At 125.5 million bales, world production is projected to increase 7.0 million bales year-over-year to a level just below the record of 127.2 million set in 2011/12. At 125.9 million bales, world consumption is expected to increase 3.2 million bales year-over-year and is pre- dicted to surpass the existing record of 124.2 million set in 2006/07.

With only 474,000 bales of separation between production and use, world ending stocks are expected to be relatively stable (76.5 million bales in 2018/19 and 75.7 million in 2019/20). However, the distribution of global stocks has proven more important for prices than the global volume in recent years. Chinese ending stocks are projected to decrease 2.9 million bales in 2019/20 to 30.7 million bales. This is less than half the record set in 2014/15 (66.4 million), but remains about ten million bales above levels common before the unprecedented accumulation of Chinese stocks that followed the 2010/11 price spike.

With global ending stocks expected to be stable and Chinese stocks predicted to be lower, an implication is that stocks will increase outside of China. The largest country-level increase in stocks is forecast for the U.S. (+1.8 million bales or +38%). Since the U.S. is the worlds largest exporter, this has the potential to weigh on prices globally.

The forecast for the steep increase in U.S. stocks is primarily a result of the projection that the U.S. crop will increase 20% in the new crop year (up 3.6 million bales, from 18.4 to 22.0 million). U.S. planted acreage is expected to be relatively stable (-2%, 13.8 million acres in 2019/20 versus 14.1 in 2018/19). The larger U.S. harvest number is based on an assumption of lower abandonment. Lower abandonment is expected because of improved soil moisture in West Texas, where U.S. cotton acreage is concentrated, where little irrigation is applied, and where the drought conditions experienced in 2018/19 have dissipated.

India is also expected to have a significantly bigger crop due to improved growing conditions (+3.0 million bales, from 25.5 to 28.5 million). Together, these two countries account for most of the expected increase in global production. After a record crop in 2018/19, the Brazilian harvest is forecast to be slightly lower in 2019/20 (-0.8 million bales, from 12.8 million in 2018/19 to 12.0 million bales in 2019/20). Australian production is projected to remain low due to the ongoing drought (production was over four million bales in 2016/17 and 2017/18, was only 2.5 million bales in 2018/19, and is forecast to be only 2.2 million bales in 2019/20).

Growth in global mill-use is primarily expected to result from increases in China (+1.0 million bales year-over-year to 41.5 million in 2019/20), Vietnam(+600,000 bales to 7.6 million), India(+500,000 bales to 25.3 million), and Bangladesh (+400,000 bales to 8.4 million). All other major spinning countries are predicted to have flat or slightly higher consumption in 2019/20.

Trade is anticipated to increase next crop year (+3.3 million bales to 45.4 million) and to approach the record (47.6 million, set in 2012/13). The largest change on the export side is predicted to come from the U.S. (+2.3 million bales, from 14.8 to 17.0 million). The largest change on the import side is expected to come from China (+2.5 million bales, from 8.5 to 11.0 million).

Price outlook

The deterioration of trade negotiations between the U.S. and China has been coincident with the recent downturn in cotton prices. Nonetheless, there are other factors that also likely contributed to the decline. One factor was the onset of another round of auctions of supply held in Chinese reserves (began May 5th). Another is the prospect of a very large U.S. crop with continued precipitation in West Texas. Ironically, these two developments would normally suggest more trade between the worlds largest importer and the worlds largest exporter (as China draws down its reserves, it has less supply available to fill its production deficit and a bigger U.S. crop means more fiber can be exported).

Although China has threatened retaliation for the latest increases in tariffs (beginning May 10th, a list of U.S. imports from China valued at$200 billion face a 15 percentage point increase in duties, this is on top of the 10 point increase on the same set of goods that went into effect in September), it is unknown if there will be further consequences for U.S. cotton exports to China (which have suffered a 25 percentage point tariff increase since July 7th).

Beyond the increases that just went into effect, the U.S. has threatened to raise tariffs on all goods from China that have not been covered by previous implementations. It is unknown if and when this set of increases might happen, but it would cover apparel and home furnishings (HS Chapters 61-63). China represents more than 40% of U.S. apparel imports and over half of U.S. home furnishings imports, so this would be highly disruptive for U.S. supply chains. This could lead U.S. retailers to decrease order volumes, and therefore have a direct impact on global cotton demand. Greater consequences, however, could be indirect. To the extent that the trade dispute slows macroeconomic growth in the U.S. and China, spillover effects can be expected around the world. Weaker global economic growth is associated with weaker growth in consumption and could emerge as a heavier weight on cotton price direction.

- China Textile的其它文章

- Deepening opening and collaboration to lead high quality development

- April 2019

- China Fashion Week A/W 2019/20:Meeting the future

- Young Entrepreneurs Village and 17QCC.com start the new eco—economic engine of e—commerce in 2019

- Shishi Fashion Week 2019:Design & Times

- MSREXPO2019 and STCF2019 successfully held in Shishi