An essay on conceptualization of issues in empirical accounting research

2013-06-28 16:41:44BinSrinidhi

Bin Srinidhi

Department of Accounting,University of Texas at Arlington,United States

An essay on conceptualization of issues in empirical accounting research

Bin Srinidhi*,1

Department of Accounting,University of Texas at Arlington,United States

A R T I C L EI N F O

Article history:

Conceptualization

Maintained hypothesis

Single-entity approach

Game theory approach

Empirical research in accounting has lately focused much on sophisticated statistical methodology and econometrics and relatively less on conceptualization of the issues concerned.This essay is written to highlight the conceptualization of the issues as an important ingredient of empirical research in accounting.I present two methods of conceptualization-the single-entity approach and the game theoretic approach.I give several examples in accounting research to explain the conceptualization process.I hope that this essay will fill a much needed void in the research process in accounting and restore the balance between conceptualization and methodology.

Ⓒ2013 Production and hosting by Elsevier B.V.on behalf of China Journal of Accounting Research.Founded by Sun Yat-sen University and City University of Hong Kong.

1.Introduction

This essay,as the title indicates,deals with the conceptual and philosophical aspects of accounting and auditing research.It is deliberately written to focus on aspects of accounting research that do not concern statistics,statistical methodology,and econometrics.I am motivated to write this essay because younger researchers,especially Ph.D.students,have begun to view the process of research and publication as a mechanical production process deploying a sophisticated statistical methodology,whereas the selection and conceptualization of the issues get relatively less focus.Continuing this trend might make accounting research more focused on narrow topics that are amenable to statistical analysis while ignoring the larger issues thatneed to be resolved for meaningful progress in accounting thought.My concern is similar to that of Johnstone (2013)who bemoans a similar progression in finance research thus:

·“Research students might once have discovered such issues for themselves,through curiosity and unstructured background reading,but the modern way of PhD research is much narrower and usually involves a substantial commitment of time and thought to learning statistical techniques,and how to implement them using different software packages,and to cleaning,merging and reconstructing large data files.There is obviously less time and appetite for philosophical critique,out of which potential research outcomes are no doubt less‘safe’than those from a well-conceived empirical investigation.”

In this essay,I address the above concern by identifying the important ingredients of relevant empirical research in accounting and giving several examples of how to conceptualize issues that are currently being researched in the field.In the interest of setting expectations from this essay,it is important for me to state that I do not present much original work of my own here.I also do not fully develop the models that I present here.My purpose is to highlight the importance of conceptualization in empirical accounting research and show that it is possible to do so with some thought and basic common-sense-driven logic.In particular,it does not need extensive quantitative theoretical modeling(though such a development is welcome)to have a conceptual framework for empirical research.

1.1.The purpose of accounting research and the definition of conceptualization

What really is the purpose of accounting research?Accounting practice is more than 10,000 years old (Dickhaut et al.,2010;Waymire and Basu,2007)and has developed as part of the cultural and social organization of human beings.In its essence,accounting is the process of measuring,keeping records,and reporting transactions and performance by the more informed players in organizations to less-informed players who might control the resources.The codification of the double entry system by Pacioli has helped the field to adapt to the growing organizational complexity of both business and non-business entities as well as interactions among them.In the context of such development,Ronen(2012)speaks of the objective of accounting research as“helping to set accounting policy that maximizes social welfare by improving resource allocation.”The implication of this objective is that accounting research should offer guidance to policy makers based on both theoretical and empirical research.It is therefore important to relate empirical research(the focus of this essay)to social policy to claim relevance.

How can empirical accounting research benefit social policy?We need to identify feasible information exchanges that can direct resources controlled by less-informed parties to their maximally productive uses. Such a task requires the accounting system to examine among others(i)the organizational forces that create information differences-say,between managers and investors or between managers and regulators;(ii)the incentives of the informed parties(managers,auditors)to transmit information to the less-informed but more endowed parties(investors who hold capital,regulators who hold policy-making power);and(iii)the accountability and protection of the resources while in use or otherwise-the governance issue.Such examination requires theoretically supported assumptions on human behavior as individuals and in teams as well as theoretically supported assumptions about market behavior in situations where individuals might not have the power to affect most outcomes.These assumptions naturally derive from known evidence in the psychology literature(individual behavior),sociology(team behavior),and economics literature(individual and team behavior under institutional constraints and market behavior).We refer to these assumptions as“maintained hypotheses.”I later discuss their role in framing research questions in accounting.While theoretical research might provide some clues on how different policy prescriptions,reporting conventions,and voluntary disclosures might affect resource allocation in different organizational contexts(different ownership and capital structures),empirical research serves to verify whether these theoretical predictions hold and if they do not, whether the theory needs to be refined.

I define“conceptualization of the issue”of a research project to mean the identification of the underlying assumptions(the maintained hypothesis)and the logical process of linking the potential outputs to inputs.I define“methodology”as the selection of statistical techniques and packages to examine the relation betweeninput proxies and output proxies.The interpretation of the result is determined by the conceptualization of the issue and the maintained hypothesis.All these aspects are essential ingredients of relevant accounting research.

1.2.The current framework of empirical research in accounting

The“real world”for which we seek betterment as researchers is typically very complex.There are myriads of interacting systems and subsystems(the subsystem in accounting-part of the economic eco-system -might be seen as a composite interacting set of the second level of subsystems-accounting standardsetting system,standards enforcement system,the legal system,the auditing system,the governance system,the regulatory framework and the political system;each second level subsystem consists of a number of interacting third level subsystems-for example,the auditing subsystem can be construed as comprising of audit education,auditor certification,competition between auditors in the jurisdiction,the auditing standards and the standard-setting system)each with several observable and unobservable,dynamically changing,uncertain variables that constitute the real world.Current accounting research has adopted the(western)philosophy of reductionism,wherein the researchers seek to understand parts of the system and then examine how they interact.This“bottom-up”approach differs from the Eastern philosophies that emphasize holism where the overall system is studied first and each subsystem derives its purpose from the overall system.Further,in the reductionist philosophy,we seek to limit our examination to a manageable number of observable variables-and assume that the effects of other potential(omitted)variables are either inconsequential or get randomized in the analysis.This process of reducing the scope of analysis to a limited number of variables is referred to as“modeling”and the hypothesized relationship is referred to as a“model”.

For the current framework in accounting,I borrow from Ronen(2012).First,I distinguish between normative and descriptive models.Normative models aid decision-makers by restricting the set of choices that they need to consider in making decisions,whereas descriptive models examine the current choices and identify the relationships that exist between those choices and the context in which those choices were made.Most empirical research in accounting falls in the“descriptive”category.A particular subset of descriptive empirical accounting research is known as“positive accounting research.”Positive accounting research has a theoretical base in the contractual view offirms-that every firm is a nexus of contracts.Managerial actions are explained in a framework where managers are assumed to be acting in their self-interest and are characterized by rational expectations within the confines of their contractual stipulations.Note that positive accounting researchers do not claim to“prescribe”behavior,and therefore,this kind of research is part of the descriptive category.The ultimate difference between normative and descriptive research has been questioned(Churchman, 1961).One could also argue that normative prescriptions are seen as“rational”by management students and managers who will conform to that behavior in making the prescriptions actually descriptive in practice over time(Ghoshal,2005).

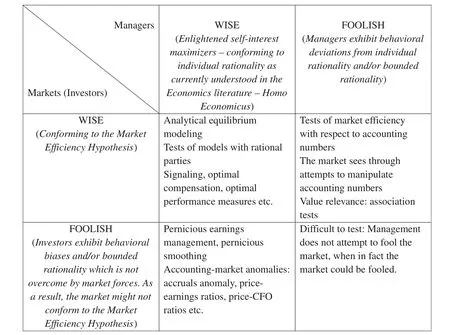

Ronen(2012)explores accounting research in the framework given in Fig.1.

In this framework,rational-expectations modeling is placed in the northwest cell where managers and investors are viewed as economically rational players acting in their self-interest with no behavioral biases. Most of the studies that fall in this cell are analytical studies.Empirical studies that show no deviation from market efficiency and no economic irrationality on the part of managers are difficult to publish because of the“lack of contribution.”Hence,we hardly find any published empirical-archival or empirical-experimental accounting studies that do not find deviations from expected behavior.

Studies that find opportunistic earnings management seem to assume that markets do not see through such opportunism.If they did,the stock price would not respond to managed earnings and if the stock price did not respond,the manager would not undertake the cost and effort involved in managing earnings.Therefore,these studies fall in the category where managers are considered rational but investors are either naive or do not care enough to see through the managed earnings.(Note that informative earnings management falls in the cell where both managers and investors are modeled as rational.)A particular naivete´that is often attributed to investors is called“Functional Fixation”.Believers in functional fixation assume that investors focus on reported earnings(and other financial statement numbers)but do not consider how that earnings number is derived.Unexplained anomalies such as accruals anomaly(Sloan,1996)are often attributed to such fixation on the part of investors.As Ronen(2012)points out,the law and courts in the US(and most countries)have held the view that managers can fool investors.Based on this view,they have sought to constrain managerial reporting-under the notion of“protecting the uninformed investor”,presumably from smart and manipulative managers.

The northeast cell where the market is assumed to be efficient but managers are not fully rational is populated by several early“event-study”accounting papers such as Ball and Brown(1968).The logic in these studies runs thus:the market is efficient and prices move only when there is unanticipated information(news); therefore,to the extent that accounting earnings changes are associated with changes in market returns,there is information content in accounting.By implication,any report that moves the market is informative and any report that is discarded by the market is non-informative.Managing the earnings report is fruitless because the market sees through and disregards these changes and only a naı¨ve manager would still try to manage the report.

The trend in empirical research in accounting is to explore deviations from market efficiency(behavioral biases of investors)or to explore the behavioral biases of managers.In the southeast cell,the researcher assumes that both investors and managers are driven by behavioral biases.There are few empirical studies that do this,because of the lack of consensus on behavioral theories that predict specific deviations for both investors and managers.

The above framework presents the overarching maintained assumptions underlying most of the empirical studies in accounting.In the next section,I discuss the role of maintained hypothesis in conceptualizing a research question.In Section 3,I explain the conceptualization of research questions using a single-entity approach.In Section 4,I discuss the conceptualization of research questions using game theoretic models where the focal entity is modeled as one of two or more strategic players.Conclusions are given in the last section.

Figure 1.A Conceptualization Framework(from Ronen,2012-the notation in italics are added by me).

2.The role of maintained hypothesis

Conceptualization of a research question is done in a framework that is shaped by an assumed theoretical basis that will not be explicitly tested in the paper.This underlying theory2Normally,the term“hypothesis”is a tentative idea awaiting confirmation or falsification whereas“Theory”is a hypothesis that has been confirmed overwhelmingly by evidence.In contrast,an axiom is an assumption that is generally held to be true,without confirmation. A fact is generally accepted as true,whether it is proved or not.For example,the existence of human beings is held to be true(and is accepted without proof or evidence)-a fact.How human beings have come into being is,on the other hand,a theory-the theory of evolution-a hypothesis that is supported by overwhelming evidence(see Dawkins,2009-Chapter 1-for a discussion of these terms).A maintained hypothesis is in between a hypothesis and a theory but is assumed without explicit testing as the basis for examining the research question on hand.Efficient Market Hypothesis,Utility theory,Prospect theory and Functional Fixation are examples of maintained hypotheses for most accounting studies.is referred to as the maintained hypothesis and is usually accepted well enough to not need a defense in the study.As an example,consider the case where you empirically examine the effect of an accounting standard-expensing of research and development expenditure-on the decision of how much to spend on research and development.Two possible maintained hypotheses are possible.First,let Functional Fixation be the maintained hypothesis.Under this assumption,the investors are unable to fully understand the valuation implications of the research and development expenditure and depend on the reported accounting income to derive their valuation.Under this maintained hypothesis,the following claims could be made:(i)firms with high research and development expenditures that are immediately expensed will be undervalued;(ii)allowing capitalization will increase their reported income and make investors increase their valuations of the firms.Anticipating this,managers will be more reluctant to undertake research and development expenditures in the former case(expensing)but less so in the latter case(capitalization).These claims allow us to hypothesize that under the maintained hypothesis of functional fixation,having an expensing rule for R&D expenditures will depress the R&D activities undertaken by research-based firms under that regime.Allowing capitalization will correspondingly boost R&D expenditure.However,if the maintained hypothesis is the efficient market hypothesis,we cannot use the above argument in our conceptualization.Investors will properly evaluate the research and development expenditure irrespective of whether the amount is expensed or capitalized or partially capitalized.However,under this assumption,we could invoke signaling implications to explain why allowing partial capitalization might be useful.Allowing such capitalization could provide managers with the means of communicating their successes in R&D projects in a credible manner without incurring significant proprietary costs.As a result,investors, using signals can better evaluate firms than if either expensing or capitalization were mandated.As you can see from this discussion,the same empirical result is theoretically supported in two different ways depending on the maintained hypothesis chosen to explain it.It is important to mention that the maintained hypothesis of functional fixation generally needs greater justification than the maintained hypothesis of efficient markets.

The maintained hypothesis could be different in different contexts.For example,the political setting and the economic infrastructure in China are such that most of the capital resources are controlled by the State.The maintained hypothesis of free markets has limited applicability in China.A private firm operating in the Chinese market might well depend on political connections and influence to gain access to capital and resources rather than appealing to investors by being transparent.In fact,exposure of political connections and extralegal dealings could expose the connected individual and the firm to extreme penalties,and therefore,it might be in the interest of both parties to be opaque.The maintained hypothesis here is one of political rent-seeking rather than the free market economy.

The maintained hypothesis allows us to hypothesize the predicted behavior of the entity in question as well as the behavior of the environment in which the entity is situated.In the next section,I will discuss the case where the environment is characterized by uncertainty but is not modeled to consist of strategic players.In the subsequent section,I discuss the case where the environment consists of strategic players.

3.Conceptualization of accounting and auditing research problems using a single-entity approach:the loss function

The concept of loss function is borrowed from Statistics and Decision theory where it is defined as a function that maps an event onto a real number intuitively representing some“cost”associated with the event.We use the notion quite broadly here to represent any situation where we could represent a trade-of ffaced by an entity in choosing a parameter by the entity’s total cost of choosing it at different levels.We normally use this mental model of trade-of fwhen the entity faces an uncertain environment but not when it faces one or more strategic players.

3.1.Example 1:Auditor loss function and auditing standards

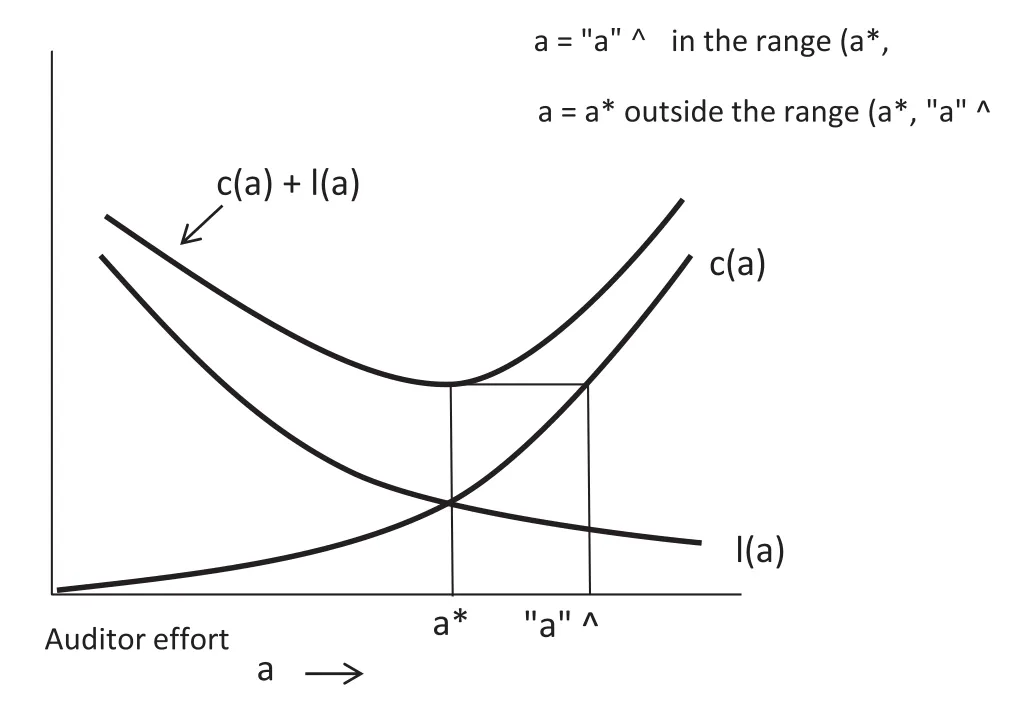

This example is developed using a simple auditor loss function but a more advanced analysis has been done in Ye and Simunic(2012).Consider the problem of audit standard-setting where the standard requires a minimum(floor)effort from the auditor.We view the effort of the auditor broadly to include the audit hours that are spent,specialist skills brought to bear,investments in technology,and other costs incurred on the audit.In that sense,the audit effort modeled in the loss function is for all practical purposes,a proxy for audit quality. Conceptualization of this issue proceeds as follows:

(i)How does the auditor choose effort in the absence of standards but within the current legal framework?

(ii)What effect does a standard have on this effort?When does a particular standard affect the auditor’s effort and when does it not affect the auditor’s effort?

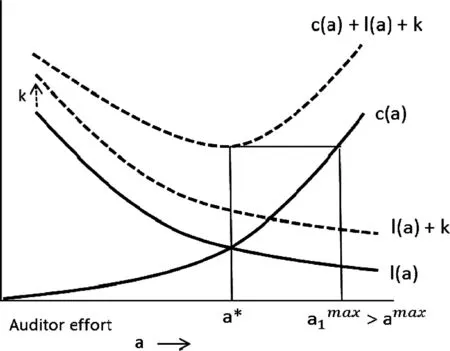

We model the direct cost of the audit-the expected cost that the auditor incurs in delivering the audit c(a)-as a function of the audit effort a.We model it as a cost that is increasing at an increasing rate-similar to most cost functions,i.e.,c′(a)>0 and c′(a)>0.The countervailing cost is the expected aggregate cost of litigation.The cost of litigation follows a joint distribution of the probability that the auditor will be sued by a plaintif fand the distribution of the(i)penalties and cost that might be imposed on the auditor;(ii)the opportunity cost of lost future business because of the potential loss of reputation;and(iii)the cost of preparing for the defense or arbitration.We expect this cost l(a)to decrease in auditor effort at a decreasing rate,i.e., c′(a)>0 and l′(a)>0.In the absence of any standards,the auditor will minimize c(a)+l(a).If the continuity and differentiability assumptions hold,this will happen at a point a*where c′(a*)=0.Consider an auditing standard that can precisely require the auditor to put in an effort ar.The standard will be effective in the range (a*,amax)where amaxis defined by the equation c(amax)=c(a*)+l(a*)but not outside that range.The reason is that if the regulated effort is less than a*,the auditor still minimizes the total cost at a*(higher than the regulated value of the effort)and if the regulated effort is more than amax,the auditor takes the risk of violating the standard and is still better of fsupplying the effort a*.This is illustrated in Fig.2.

The advantage of this simple conceptualization is that we can draw inferences on a number of propositions. Consider the following:

(iv)In legal regimes such as the US where the litigation costs are higher,the optimal audit effort is higher, ceteris paribus.

(v)In jurisdictions where it is very costly to improve audit quality(effort)[could be because not many auditors are trained well;the independence of auditors cannot be assured;there is no support from the governance structure],the first derivative c’(a)is higher and this decreases the optimal audit quality.

Figure 2.Auditing Standard&Auditor Loss Function.

Figure 2a.Effect of increase in l(a)on the range of effectiveness.

Many of the above propositions are not obvious unless the conceptualization using the auditor loss function is made.In other words,even having this simple conceptualization can improve the understanding of the effect of standard setting on audit quality.Ye and Simunic(2012)consider two dimensions of auditing standards:toughness which is akin to the minimum effort level alluded to above;and vagueness which is the uncertainty in the enforcement of the standard resulting mostly from the vagueness in the language of the standard. In that case,they show that if the toughness of the audit standard requires effort from the auditor above the (otherwise)optimal level,the auditor would prefer a vague standard over a precise standard.

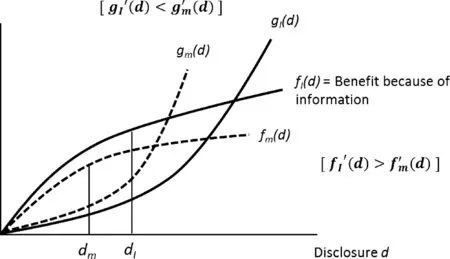

3.2.Example 2:Optimal disclosure and competition

Some of the propositions that follow from this conceptualization are:

(i)In a setting where proprietary costs are high,the optimal disclosure demanded by investors is low.

(ii)In settings where the disclosure does not result in competitive disadvantage-could persuade competitors to even withdraw from the market or reduce capacity-investors demand higher disclosure

(iii)In settings where managers’compensations are not tied to firm value,the first derivative,f′m(d)is smaller compared to the benefits to the investor and managers are likely to supply much lower disclosure relative to what is demanded by investors.

(iv)In highly competitive settings where the first mover advantage is very valuable,investors demand less disclosure.

(v)In settings where managers have invested significant human capital into new product development and other projects,the proprietary cost to the manager of disclosing the details would be very high.Therefore,managers would supply much lower disclosure than what is demanded by investors.

(vi)In a high litigation environment such as the US,managers might face high litigation costs if there is discovery of delay in(bad news)disclosures.In effect,the benefit of disclosure for managers becomes higher,i.e.,fm(d)and f′m(d)are high.This results in more(and early)disclosure of bad news(Skinner, 1994)

Figure 3.Disclosure from investors’and managers’viewpoints.

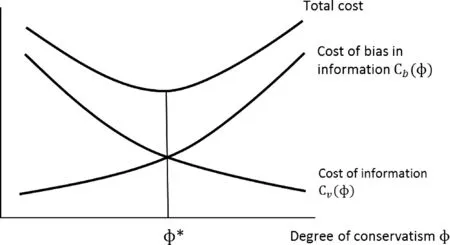

Figure 4.Trade-of fin conservatism.

3.3.Example 3:Optimal degree of conservatism

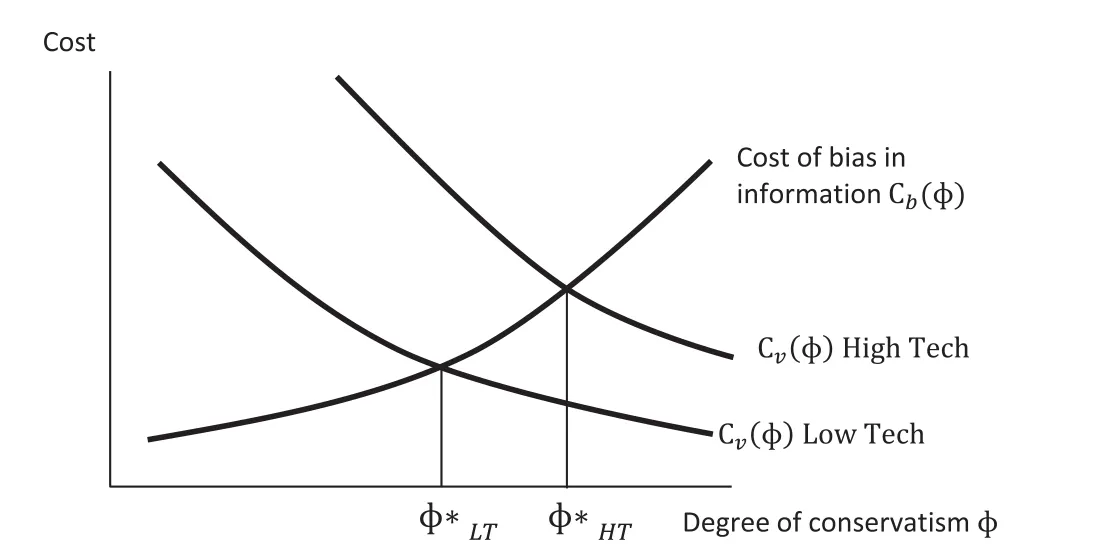

Investor demand for conservatism can be conceptualized based on the above trade-o ff.As an example,consider the difference between high-and low-technology firms.High-technology firms and high growth firms have very uncertain futures.This increases the direct cost and the risk of verifying any news about the future. For example,verifying that inventory does not lose value till they are sold in a few months’time would be more difficult in a high-technology firm than say in a firm that manufactures farm equipment.Therefore, the cost of veri fication and its rate of decrease are both higher,i.e.,c′ν(φ*)is lower(more negative).This makes the optimal conservatism for high-tech firms,φ*HThigher than that for similar low tech firms,φ*LT.Optimally, investors demand conservative reports from high growth and/or high-tech firms that are characterized by greater uncertainty.This trade-of fis shown in Fig.4a.

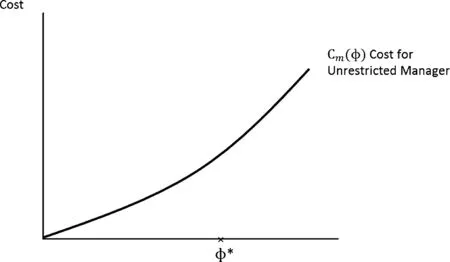

Managers,however,personally incur a very small part,if at all,of the verification costs.The cost of bias is borne by investors.Conservatism could be costly to managers if their compensation depends on accounting income because deferring good news will also defer their compensation.In the absence of any restriction,managers will perhaps choose unbiased reporting of good news and perhaps withhold some of the bad newsresulting in an aggressive report.The“supply”of conservatism by managers will be lower than the demand for conservatism by investors.The cost of conservatism for the unrestricted manager is shown in Fig.4b.Inthe absence of restrictions,there is no corresponding benefit,and therefore,managers find the optimum in the lowest degree of conservatism.

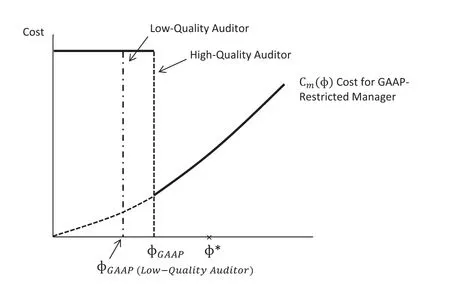

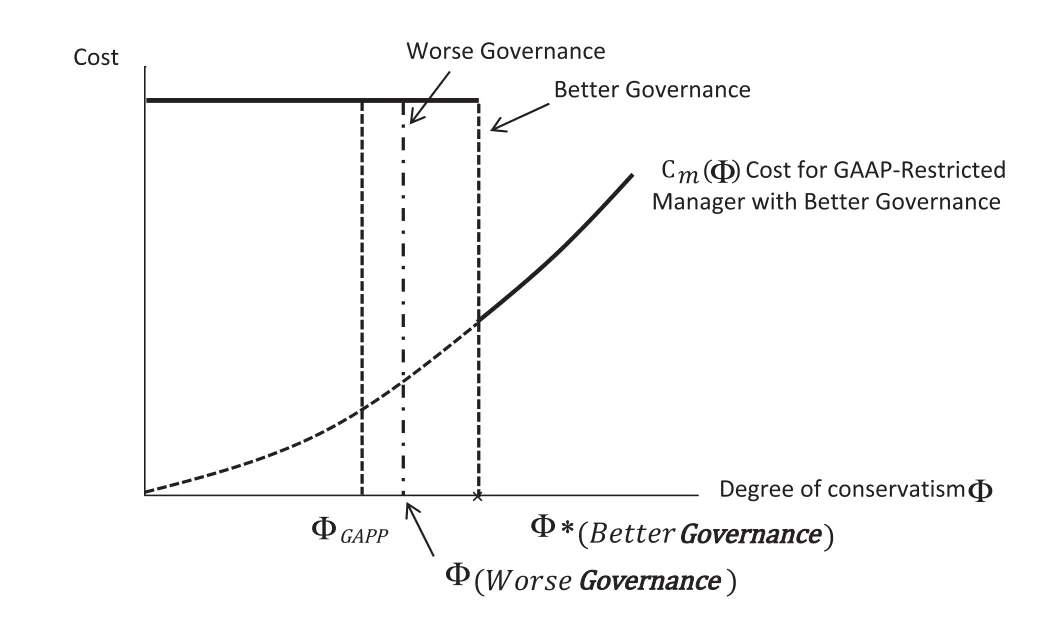

This conceptualization shows that if investors’demand for conservatism is to be satisfied,it needs to be imposed on managers.GAAP does this by requiring managers to comply with conservative accounting rules and having a third-party auditor audit the report.If the auditor is strict and GAAP is followed,the minimum conservatism will be set at φGAAP.If the auditor is lax,GAAP might not be strictly enforced and the manager might supply a level of conservatism,φ<φGAAP.In the case of most firms,φGAAP≤φ′.If that is not the case, i.e.,if φGAAP>φ′,the conservatism deployed by managers will be forced to be higher than that demanded by investors,which is a sub-optimality caused by onerous GAAP regulations.However,when φGAAP≤φ′,theminimum conservatism supplied by the manager can be increased by independent boards that uphold investor rights and would institute internal procedures to satisfy the investors’demand.These trade-offs are shown in Figs.4b-d.

Figure 4a.Conservatism demanded in high and low tech firms.

Figure 4b.Cost of conservatism for the unrestricted manager.

Figure 4c.Cost of conservatism for the GAAP-restricted manager-different audit quality settings.

Some of the propositions that follow from this conceptualization are:

If GAAP reflects investor demand for conservatism,jurisdictions with stronger enforcement,stronger legal system,and a non-interfering political system will exhibit greater conservatism than other jurisdictions (Bushman and Piotroski,2006).

Firms with institutional ownership will exhibit higher conservatism because institutional investors are better able than retail investors to impose their demand on managers(Ramalingegowda and Yu,2012).

Figure 4d.Cost of conservatism for the manager under different governance settings.

4.The use of multiple entity approach to conceptualize problems in accounting and auditing research:game theory

Although the conceptualization of many accounting issues using a single-entity perspective facing trade-offs is useful,it is often not appropriate in situations where the entity faces one or more strategic players who react to the actions of the entity.The trade-of f/loss-function approach assumes implicitly that the entity is facing an uncertain environment where the probability distributions facing the entity are not affected by its actions.In contrast,in an environment with strategic players,each player will try to maximize its own self-interest and therefore,for different actions,there will be different reaction functions that determine the resulting equilibrium.In that sense,conceptualization using strategic games could be different and richer than conceptualization using the single-entity framework.

The concept of equilibrium that is most useful in conceptualization of accounting problems in the gametheoretic framework is that of Nash equilibrium.A Nash equilibrium is one in which no player has a unilateral incentive to seek out a different action.On the other hand,the Pareto-optimal solution is one in which it is not possible to improve the payof fof any one of the players without decreasing the payof fof another.The Nash equilibrium could be different from the Pareto-optimal solution.In other words,the players in Nash equilibrium could be better of fusing a different set of actions but by definition,no player has the incentive to unilaterally deviate from the Nash equilibrium strategy.Such Nash equilibrium would be a dysfunctional Nash equilibrium.A particular class of problems with dysfunctional Nash equilibrium is the Prisoner’s dilemma illustrated in the payof fmatrix between two players below.There are two parties A and B who cannot credibly communicate(meaning that even if they could communicate and arrive at an agreement to cooperate with each other,there is no ex-post enforcement mechanism to enforce the agreement.As a result,the agreement will be broken at will and such a break will be anticipated correctly by the other party)with each other and have to choose one of the two actions each-Cooperate(C)or Defect(D).The payoffs(Party A payof f,Party B payof f)are given in the corresponding cells of the Table.The notations are R:reward for mutual cooperation;T:Temptation payof f;S:Sucker’s payof f;P:Punishment for mutual defection.

Party B Party A Cooperate(C)Defect(D) Cooperate(C)(R,R)=(3,3)(S,T)=(0,5) Defect(D)(T,S)=(5,0)(P,P)=(1,1)

Consider the payoffs of the choices of Party A if Party B cooperates.A would prefer D over C because T>R(i.e.,he can get 5 by defecting,which is higher than the 3 he gets by cooperation).If Party B defects, then also A would prefer D over C because P>S(i.e.,he can get 1 by defecting,which is higher than the 0 he gets by cooperation).In this case,irrespective of B’s strategy,A prefers to defect.This strategy choice is called dominant strategy.Because of symmetry,a similar logic applies to B who prefers to defect also.This results in Nash equilibrium(D,D).It is easy to see that the Pareto-optimal choice is(cooperate,cooperate),but that is not Nash equilibrium and will not be deployed.Even if this game is repeated and the two parties agree to alternate between(defect,cooperate)and(cooperate,defect)strategies,each will,on average,get a payof fof 2.5, which is still lower than the Pareto-optimal payof f.[Mixing two strategies using a pre-defined probability will make it a game that allows randomized strategies but I will limit this essay to pure strategies,because the motivation of the essay is to conceptualize,rather than develop sophisticated models.]Dysfunctional Nash equilibrium will prevail as long as two conditions are satisfied:T>R>P>S;(T+S)/2<R.I reiterate that the Prisoner’s dilemma is only one class of games where the dysfunctional Nash equilibrium exists and is dominant.

4.1.Implications of dysfunctional Nash equilibrium for accounting research

The first implication of the existence of dysfunctional Nash equilibrium in games is that the optimization carried out using the trade-o ffand loss functions in Section 1 might not be feasible.This observation goes to the heart of many arguments I have found in papers that implicitly or even explicitly assume that the empirical findings must represent the best strategies for the concerned parties.Unfortunately,this assertion is often incorrect.

The second implication concerns the role of regulation and standard setting.One way of understanding the role of regulation and standard setting(which clearly put restrictions on the workings of the free market)is that they could prevent some dysfunctional Nash equilibrium and thereby nudge the parties towards a Paretooptimal solution.

I give below some examples of conceptualization using game theory.

4.2.Example:Conceptualization of the auditor-manager game using game theory

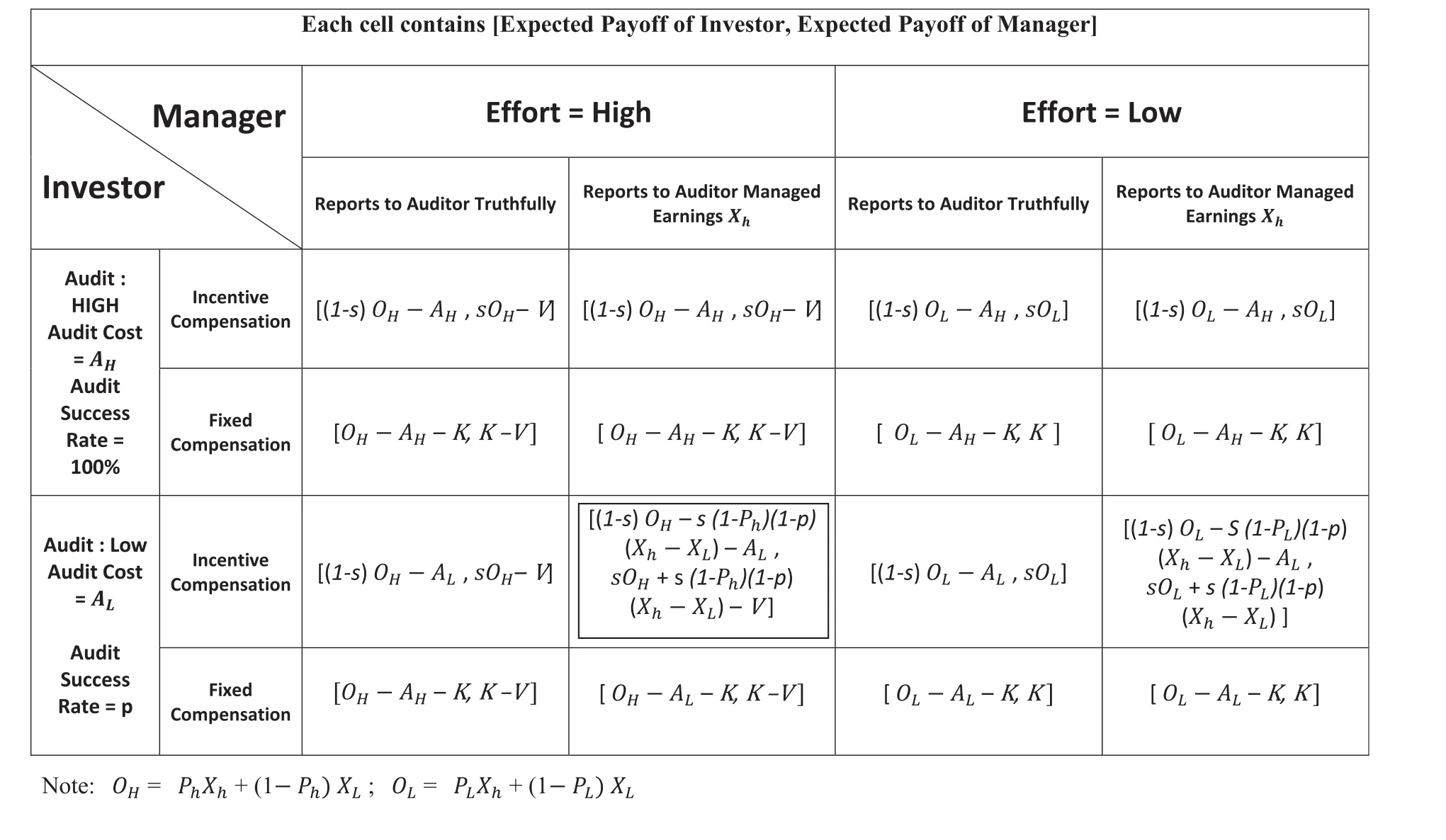

The details of the conceptualization of the reporting by managers and the resulting effort and investment that the auditor puts into the engagement at two levels of expected litigation cost are given in Appendix A.The investor is also a player but is not explicitly modeled here to keep the game simple.The investor is assumed to affect the payof fof the auditor through the credibility offinancial statements.The manager is modeled as having two choices-reporting truthfully(Honest)or reporting with some manipulation(Dishonest),whereas the auditor has the choice of providing a low or high quality audit.In the auditor loss function modeling given earlier,higher auditor quality increased direct audit costs but decreased the expected loss from litigation and reputation loss that accompany an audit failure.However,if the manager is honest,there is no loss from litigation costs from a low quality audit,but there might be lower credibility for the investor,resulting in lower audit fees(through board negotiations).When the manager is dishonest,and the auditor provides a lower quality audit,there could be litigation costs as well.In other words,the auditor loss function depends on the manager’s action and so,the auditor could implement different qualities depending on his expectation of the manager’s actions-and the manager’s actions could differ based on the manager’s expectation of whether the auditor provides a high or low quality audit.

In this scenario,when litigation costs are low,the Nash equilibrium is obtained at(Dishonest reporting, Low quality audit)-which points to an implicit collusion between the manager and the auditor.The desired outcome is(Honest,High quality audit)but if the manager is honest,the auditor has an incentive to provide a low quality audit.Further,if the auditor provides a low quality audit,the manager has the incentive to be dishonest.In the example that is given,increasing the litigation cost removes the dysfunctional Nash equilibrium above but replaces it with(Dishonest,High quality audit).If the high quality audit“exposes”the dishonest manager,the manager’s payof fcould be modeled as being less under when the manager is dishonest (In the southwest cell,the manager’s payof fcould be l00)and this could make the Pareto-optimal solution (Honest,High quality audit)the only Nash equilibrium.

4.3.Example:Conceptualization of opportunistic earnings management as equilibrium in manager-investor game

Recall the argument made earlier in the Introduction that opportunistic earnings management might not be in the equilibrium solution if investors are rational and see though such manipulations by management.In that case,they discount the earnings report and the manager gains nothing by managing earnings -which inevitably leads to the conclusion that opportunistic earnings management requires behavioral deviation from economic rationality on the part of the investor.However,this logic ignores an important aspect of the game.The effort of the manager is not observable,and therefore,it is rational for the investor(principal)to transfer some risk in the output to the manager(agent).Moreover,the output is not observable to the investor but will be known to the manager.The investor could require the manager to report the output but constrain misreporting by an auditing-governance system.The report can be made completely truthful about the output only at an exorbitant cost of audit and governance.At normal governance and audit levels,the manager could manage earnings by reporting high earnings when the actual output is low and to the extent that the audit system does not correct it,the“managed”earnings will be in the final report to the investor.Under reasonable conditions given in Appendix B,it is seen that the equilibrium is reached when the manager manages income but puts in high effort and the investor provides incentive compensation.The two ways in which the investor can get truthful reporting are by(i) providing fixed compensation in which case,the manager does not mind telling the truth but has no incentive to deploy high effort;or(ii)employing a very costly monitoring procedure that ensures truth telling but has a very high deadweight cost.Neither of these solutions is palatable to the investor.The better solution is for the investor to provide incentive compensation that is increasing in the reported outcome and have a moderate governance and auditing system that constrains but does not eliminate earnings management.In equilibrium,the investor fully expects the manager to manage income but is still willing to use the managed income as the basis of incentive compensation.Note that this equilibrium holds even in multi-period settings as long as the effort in a period produces output only in that period and contingent contracts are not feasible.This conceptualization enables us to understand why we observe opportunistic earnings management even within rational modeling of both the manager and the investor.

4.4.Example:Conceptualization of the Analyst-Manager game to explain biases in analyst forecasts and recommendations

In the absence of strategic responses from managers of the firms that they cover,it would be rational for analysts to provide unbiased earning estimates and recommendations to investors.In such equilibrium, the accuracy of the analyst forecast will be normally high and the precision depends on the skill and effort levels of the analyst.However,there is considerable literature on analysts being optimistic or otherwise biased in their earnings forecasts and recommendations of the stock of the firms they cover(Lim, 2001;Das et al.,1998).The game tree given in Appendix C provides the rationale for the bias in analyst forecasts.Consider the case where the prior information on the firm is bad in that it is facing some financial difficulties.The analyst has the choice of being truthful and making a sell recommendation on this stock as well as giving a downbeat prediction of earnings.Alternatively,the analyst could present a rosierpicture than deserved by the firm and not give a sell recommendation.In the former case,the manager is likely to be ruffled because of the increased probability of the firm going bankrupt and thereby wasting the non-diversifiable human capital that the manager has put into the firm.The consequence to the analyst is likely to be reduced access to the manager’s and firm’s closely held information.On the other hand, if the analyst produces an optimistic forecast,the access to future information is not reduced.This makes it likely that the analyst will choose the latter course and produce an optimistic report.The investor will rationally anticipate this optimism and is not hurt much because he will trim the recommendation of the analyst.In the case where there is no financial difficulty for the firm,the dynamics are different.An optimistic forecast will make it difficult for the manager to beat the estimate and thereby try to maximize his incentive compensation.A non-optimistic forecast will make the process of beating the estimate a little easier for the manager.Therefore,one could expect a rational analyst to provide a non-optimistic forecast for firms that are doing well.

5.Conclusions

This essay has provided two ways of conceptualizing several accounting and audit research problems. The first one is the single-entity approach in which the problem is conceptualized as a trade-of fbetween different costs or the maximization of costs and benefits when the world outside the entity in question is modeled as non-strategic but uncertain.This is a reasonable model if the entity operates in relative isolation or if the environment consists of a large number of players each one of whom has little ability to control the reaction to the actions of the entity.A competitive market is a good example of such an environment.However,in most cases that we encounter in accounting and auditing research,this assumption is not satisfied.There are other entities that are strategic and their reaction is driven by their own self-interest and therefore cannot be modeled as random.In these cases,game theory provides a good framework for conceptualization of the problems.I have provided some examples of conceptualization using these frameworks.

In conclusion,it is my hope that this essay contributes in a small measure to transforming the nature of accounting and auditing research undertaken by Ph.D.students and several younger colleagues.In particular, I hope that the extreme focus on econometrics and statistical reasoning is balanced by a greater conceptualization of the issues in a way that allows the researcher to better interpret and understand empirical results.

Dedication and Acknowledgements

I dedicate this essay to my mentors and fellow students during and after my Ph.D.program in Columbia University in the 1980’s in shaping and molding my thinking,in particular to Profs.Joshua Ronen,Kashi Balachandran and Miklos Vasarhelyi for providing intellectual stimuli during that time and to Prof.Ferdinand Gul for sharing his extraordinary insights into empirical research in accounting and auditing with me during the last decade.I acknowledge Dr.Chandra Subramaniam at UTA for his constructive comments on the essay.For the preparation of this paper,I thank the help of my graduate assistants,Yvonne and Wei.

Appendix A.

Auditor-manager.game

Auditors can provide a high quality audit(with cost)or a low quality audit(no cost).

Managers can be completely honest or engage in income manipulation(dishonest).

When the audit quality is low,manager’s compensation might be lower because there is less credibility in the manager.

Auditor’s payof f=Audit fees-Audit cost.

Manager’s payof f=Expected compensation+Expropriation.Now,consider the following payof fmatrix. The payoffs in cells are(manager’s payof f,auditor’s payof f).

Auditor High Quality Audit(HQA)Low Quality Audit(LQA) ManagerHonest(H)(100,10)(80,15) Dishonest(D)(100,0)(90,10)

Cell(H,HQA):This payof fmatrix is based on the following assumption when the manager is honest and the auditor provides a high quality audit,manager’s compensation is$100,and the auditor incurs the normal audit cost$5 and gets a fee$15.His payof fis$15-$5=$10.

Cell(D,HQA):When the manager is dishonest but the auditor provides a high quality audit,the manager’s report is corrected and he receives the same compensation of$100.(It could be more because of residual expropriation but I choose to ignore it)The auditor has to put in additional effort to identify the managed amounts and revise the report.His cost increases to$15 and the payof f=$15-$15=$0.

Cell(H,LQA):The manager is honest but the auditor provides a low quality audit and the decreased credibility in the report reduces the manager’s compensation to$80.The auditor incurs no cost and gets a fee of $15.His payof fis$15.

Cell(D,LQA):The manager is dishonest and expropriates an amount of$10 in addition to the compensation of$80.The manager’s payof f=$90.The auditor gets his fee of$15,but suffers an expected litigation cost of$5.His payof f=$10.

Analysis:This is a prisoner’s dilemma case.

If the manager is honest,the auditor gets a higher payo ffof$15 by providing LQA($15>$10).If the manager is dishonest,the auditor gets a higher payoffof$10 by providing LQA($10>$0).Irrespective of the manager’s action,the auditor is better of fwith LQA.

If the auditor provides HQA,the manager is indifferent between being honest and dishonest(gets$100 in both cases).

If the auditor provides LQA,the manager is better of fbeing dishonest(gets$90 instead of$80).Irrespective of the auditor’s action,the manager is better of fbeing dishonest.Therefore,the equilibrium in this period game is(Dishonest,LQA).The preferred outcome is(Honest,HQA).

If the expected litigation cost for the auditor providing LQA=$18(say)[Any number≥15].The payoffmatrix will be changed to the following:

Auditor High Quality Audit(HQA)Low Quality Audit(LQA) ManagerHonest(H)(100,10)(80,15) Dishonest(D)(100,0)(90,-3)

We have assumed that the litigation cost=0 if the manager is honest or if the auditor supplied a high quality audit.Only in the case of(Dishonest,LQA),auditor payof f=$15(auditor fee)-$18(litigation cost)=-$3.

In this case,the manager’s equilibrium action is not changed.If the manager is dishonest,however,the auditor anticipates this and given that the manager’s action is dishonest,the auditor’s optimal response is HQA.The equilibrium in this game would change to(Dishonest,HQA).

The conceptualization is different from the earlier loss function conceptualization in that the auditor’s loss depends on the manager’s action which is not random.

Appendix B.

Investor.-manager game-earnings management

In this example,I model the interaction between investors and managers as a one-period principal-agent game.The description of the game follows.

Description.of the game

We model a risk-neutral manager who engages in a productive effort that can take two values:High and Low.The effort itself is not observable.The output of the agency is valuable to the investor who is also risk neutral.The output is uncertain and can take two values:xhand xLwhere xh>xL.The probability of getting the high output xhis higher with high effort.I denote the probability of high output conditional on high effort as phand the probability of getting high output conditional on low effort as pL,i.e.,Prob(xh|High effort)=phandProb(xh|Loweffort)=pL.Correspondingly,Prob(xL|Higheffort)=1-phandProb(xL|Low effort)=1-pL.

The output is privately observable to the manager but is not observable to the investor.The investor engages a third-party auditor to verify the reported outcome.The manager reports the outcome to the auditor who verifies it and presents the final report(after revision if the audit reveals a wrong report)to the investor. The auditor can be asked by the investor to apply an intensive audit which is very costly(the audit is denoted as HIGH and its cost is denoted as AH)that will ensure that the manager’s report is always corrected(100% success rate for the audit)to the actual output.With this audit,the investor always gets an accurate report of the output.Alternatively,the investor can ask the auditor to apply a moderate audit denoted as LOW with a much lower cost denoted by ALand a success rate of p,i.e.,it detects wrong reports with a probability p and corrects them before sending them to the investor.There is a probability of(1-p)where the manager can get away reporting the high output when the output is low.

The investor compensates the manager either by a share of the output s,i.e.,the compensation=s*Final report by the auditor(called INCENTIVE COMPENSATION)or by a fixed amount K(called FIXED COMPENSATION).In either case,the expected compensation should cover the reservation wages of the agent (which is the same as K).

The manager incurs a cost(disutility of effort)of V if he supplies the HIGH effort but no cost if he supplies the LOW effort.

The payof ftable and the equilibrium

The payof ftable given here shows the payof fs to the investor and manager under different choices.We make the following assumptions on the values of the variables:

AH≫AL.Moreover,AHis too costly to implement for the investor.Therefore,the AUDIT=HIGH rows in the table are dominated by the AUDIT=LOW rows.

For ease of presentation,I denote the expected outputs as follows:

The expected output with high effort=OH=PhXh+(1-Ph)XL

The expected output with low effort=OL=PLXh+(1-PL)XL

Iffixed compensation is given,it is clear that the manager prefers K over K-V and therefore chooses low effort.This will produce an output OL<OHand the investor will have a payof fof OL-K-AL.On the other hand,if incentive compensation is given,the manager will work for this agency and choose HIGH effort over LOW effort if the following conditions are satisfied:

When these conditions are satisfied,the equilibrium is where the manager puts in high effort and manages the earnings report and the audit technology allows some earnings management to go undetected and uncorrected.Because of condition(ii),the manager is at least weakly better of fwith the incentive compensation and because of condition(i),the manager prefers to put in high effort instead of low effort in spite of the higher cost of doing so.The investor benefits by higher outcome that he can retain.

I note that the investor benefits from higher effort because of two reasons:(i)xh>xL;(ii)ph>pL.The higher the differential between high and low outputs and the higher the differential between high and low efforts in determining the probability of higher output,the greater is the incentive for the investor to induce higher effort.From condition(i),these two reasons can reduce the minimum value of s.Because the audit is not always successful,the manager exploits the system to manage earnings.However,from condition(ii),note that if p is low,the reservation utility of the agent can be satisfied by a low s because the manager rationally expects to manage earnings,“mislead”the investor and earn higher compensation.The investor,on the other hand,rationally expects the manager to engage in such behavior and correspondingly can reduce s and still expect the manager to work for the firm.

I also caution here that this is a highly stylized and simplified model and should not be mistaken to be a comprehensive model for explaining earnings management.I have assumed a risk-neutral manager which, technically,should result in an optimal solution where the investor rents out the facility to the manager and the manager implements the first best solution.I have also reduced the problem to simple binary values of effort,output,and audit technology.Yet,it captures the intuition that information asymmetry about the outcome forces the investor to tolerate earnings management in order to reduce moral hazard and motivate a higher effort on the part of the manager.

Equilibrium is the boxed square in the table.Investor provides incentive compensation.Manager chooses high effort but manages earnings.

PAYOFF Table.

?

Appendix C.

Ball,R.,Brown,P.,1968.An empirical evaluation of accounting income numbers.Journal of Accounting Research 6(2),159-177.

Basu,S.,1997.The conservatism principle and the asymmetric timeliness of earnings.Journal of Accounting&Economics 24(1),3.

Bushman,R.M.,Piotroski,J.D.,2006.Financial reporting incentives for conservative accounting:The influence of legal and political institutions.Journal of Accounting and Economics 42(1-2),107-148.

Churchman,W.,1961.Prediction and optimal decision:philosophical issues of a science of values.Prentice Hall,Englewood-Cliffs,New Jersey.

Das,S.,Levine,C.B.,Sivaramakrishnan,K.,1998.Earnings predictability and bias in analysts’earnings forecasts.The Accounting Review 73(2),277-294.

Dawkins,R.,2009.The Greatest Show on Earth.Bantam Press,U.K.

Dickhaut,J.,Basu,S.,McCabe,K.,Waymire,G.,2010.Neuroaccounting:consilience between the biologically evolved brain and culturally evolved accounting principles.Accounting Horizons 24(2),221-255.

Ghoshal,S.,2005.Bad management theories are destroying good management practices.Academy of Management Learning and Education 4(1),75-91.

Johnstone,D.J.,2013.The CAPM debate and the logic and philosophy offinance.Abacus 49,1-6.

Lim,T.,2001.Rationality and analysts’forecast bias.The Journal of Finance 56(1),369-385.

Ramalingegowda,S.,Yu,Y.,2012.Institutional ownership and conservatism.Journal of Accounting and Economics 53(1-2),98-114.

Ronen,J.,2012.The state of accounting research:objectives and implementation.Asia-Pacific Journal of Accounting and Economics 19 (1),3-11.

Skinner,D.J.,1994.Why firms voluntarily disclose bad news.Journal of Accounting Research 32(1),38-60.

Sloan,R.G.,1996.Do stock prices fully reflect information in accruals and cash flows about future earnings?The Accounting Review 71 (3),289.

Watts,R.L.,2003a.Conservatism in accounting part I:explanations and implications.Accounting Horizons 17(3),207.

Watts,R.L.,2003b.Conservatism in accounting part II:evidence and research opportunities.Accounting Horizons 17(4),287.

Waymire,G.B.,Basu,S.,2007.Introduction:Why Accounting History Research is Valuable:Now Publishers,pp.1-6(Chapter 1).

Ye,M.,Simunic,D.A.,2012.The Economics of Setting Auditing Standards,Forthcoming.SSRN:<http://www.ssrn.com/ abstract=1815707>.Contemporary Accounting Research.

30 April 2013

*Tel.:+18172721310.

E-mail addresses:bin.srinidhi@gmail.com,srinidhi@uta.edu1Carlock Endowed Distinguished Professor.

Accepted 24 May 2013

Available online 19 August 2013