The reform of accounting standards and audit pricing

2012-07-01 17:09KiZhuHongSun

Ki Zhu,Hong Sun

aInstitute of Accounting and Finance,Shanghai University of Finance and Economics,China

bSchool of Accountancy,Shanghai University of Finance and Economics,China

The reform of accounting standards and audit pricing

Kai Zhua,Hong Sunb,*

aInstitute of Accounting and Finance,Shanghai University of Finance and Economics,China

bSchool of Accountancy,Shanghai University of Finance and Economics,China

A R T I C L EI N F O

Article history:

Revised 29 May 2012

Accepted 29 May 2012

Available online 24 July 2012

JEL classification:

L11

M42

M48

Reform of accounting standards

Audit market

Industry structure

Audit pricing

This paper focuses on the reform of accounting standards in China in 2007 and investigates its impact on equilibrium pricing in the audit market.We find that the concentration of the audit market and the probability of issuing modi fied audit opinions do not significantly change,but that audit fees increase significantly after the adoption of the new accounting standards in China.Deeper analysis suggests that(1)the implementation of the new IFRS-based Chinese Accounting Standards(CASs)has increased the market risk faced by listed firms and thus auditors’expected audit risk,causing an increase in audit fees, and(2)the degree of the increase in audit fees is positively related to the adjusted difference between net income according to the old CAS before 2007 and the new CAS after 2007.We thus conclude that the reform has had a significant impact on audit pricing in China.

Ⓒ2012 China Journal of Accounting Research.Founded by Sun Yat-sen University and City University of Hong Kong.Production and hosting by Elsevier B.V.All rights reserved.

1.Introduction

This study investigates the impact of the adoption of the new accounting standards in China in 2007 on audit pricing.Adopting or widely drawing on International Financial Reporting Standards(IFRSs)has become the trend in accounting standards in the current global capital market(Daske et al.,2008;Barth et al.,2008,Barth and Taylor,2009;IFRS).However,there is some controversy about whether or not theadoption of new accounting standards based on the measurement attribute of fair value improves accounting information quality or the resource allocation efficiency of the capital market(Dechow et al.,2009;Barth and Taylor,2009;Xianjie,2009;Kai et al.,2009).As a result,it is necessary to comprehensively test the impact of the change in accounting standards on the use of accounting information.

Accounting standards are an important basis that auditors use to issue audit opinions,so any change in accounting standards will affect the working base of auditors directly and thus the structure of the entire audit industry.We investigate how a change in accounting standards affects audit pricing from three dimensions:the concentration of the audit market,the attributes of the audit product and audit risk.Summary statistics show that audit fees clearly increased following the adoption of the new accounting standards.However,the concentration of the audit market has not changed.Product heterogeneity,measured as the proportion of modified audit opinions(MAOs),decreased.We thus conclude that the impact of the adoption of the new accounting standards on audit pricing has mainly occurred due to a change in expected audit risk.

We also discuss how the adoption of the new accounting standards in China has affected audit market pricing strategy according to economic theory.Based on previous relevant research,we argue that the adoption of fair value measurement in the new accounting standards makes firms disclose more information about their market risk,which increases the expected audit risk of auditors and also audit fees.The original sample that we select includes all listed firms in the A share market in China between 2004 and 2008.We use the same method as Kai et al.(2009)and employ the difference between net income under the old accounting standards and net income under the new accounting standards to measure the degree of the impact on earnings information.The results suggest that the larger the difference in net income between the old and new accounting standards,the larger the change in audit fees.That is to say,the adoption of the new CAS has had a significant impact on equilibrium pricing in the audit market and has increased audit fees.

The remainder of this paper is arranged as follows.Section 2 describes characteristics of the industry structure of the audit market before and after the reform of the accounting standards in 2007.Section 3 reviews the relevant literature and develops the hypothesis.Section 4 discusses the research design.Section 5 presents the empirical results and Section 6 concludes the paper.

2.Audit market structure:Summary analysis

The independent audit opinions offered by auditors are based on the legitimacy,rationality and consistency of the accounting information disclosed by firms.Accounting standards are the main benchmark used to assess the quality of accounting information.Changes in accounting standards not only lead to changes in the recording,measuring and reporting offinancial statements,but also directly influence auditors’work and the competitive behavior of auditors.This can lead to certain problems.For example,the adoption of IFRS may create more space for auditors to express a reasonable professional judgment,but this may confer a competitive advantage on high-quality auditors.Further,changes in standards may influence the differences between the audit products provided by auditors,which may cause the type and structure of audit opinions to change.The reform of Chinese accounting standards,in particular,may have affected the expected audit risk of auditors and in turn increase the audit fees paid by firms.

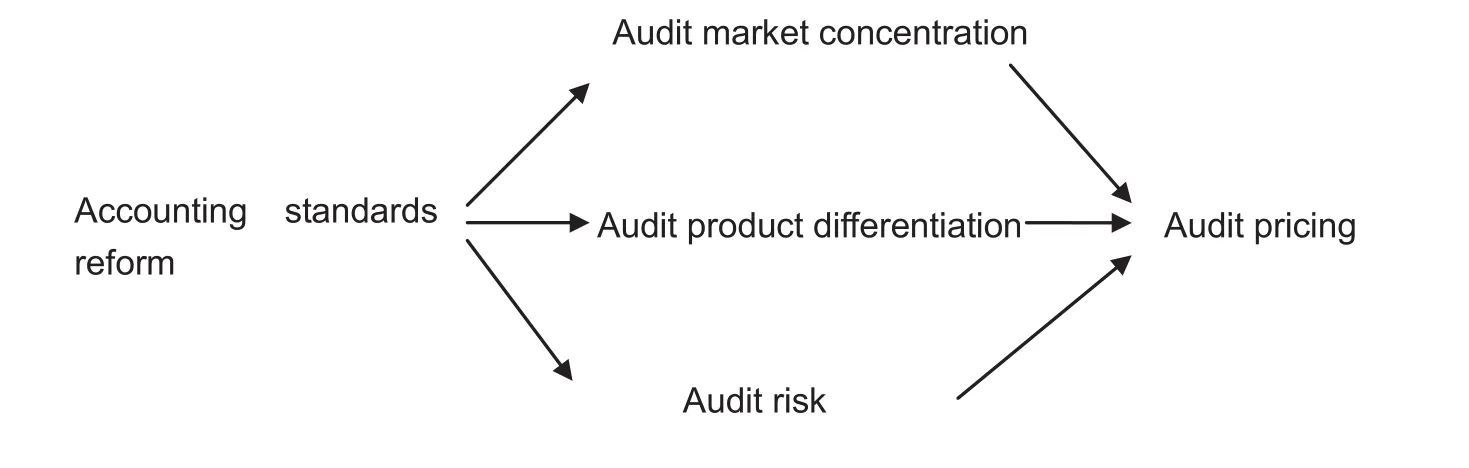

If the adoption of new accounting standards has affected the equilibrium in audit pricing,it is necessary to evaluate the characteristics both of the supply side and demand side of audit services.This study assumes the main characteristics of the supply side to be audit market concentration and audit product differentiation,and the main characteristic of the demand side to be audit risk.If audit prices increase due to the increased concentration of the audit market and differentiation of audit products,then we can conclude that it may lead to market monopoly or market segmentation.Thus,the adoption of new accounting standards may decrease the resource allocation efficiency of the audit market.Conversely,if an increase in audit risk leads to an increase in the marginal cost of audit services,that is,if audit fees increase as compensation for the additional risk assumed by auditors,then the equilibrium price of audit services will remain effective,which suggests that the adoption of new accounting standards does not change the resource allocation efficiency of the audit market.

At the beginning of 2006,the Ministry of Finance issued the new Chinese Accounting Standards(CASs), comprising one basic standard and 38 specific standards,which listed firms were required to fully follow from2007.The introduction of the CAS offers an important institutional setting to investigate how the adoption of new standards affects equilibrium pricing in the audit market.We first look at whether the reform of accounting standards has affected audit fees.

2.1.Audit fees

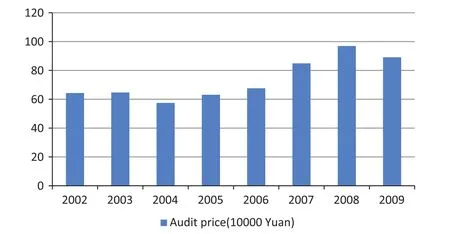

We summarize the audit fees paid by listed firms between 2002 and 2009(see Chart 1).Before the accounting standards reform(2002-2006),the average fee paid by listed firms for audit services was 6,00,000 yuan, whereas the average fee in 2007 was 8,40,000 yuan.Chart 1 clearly shows that audit fees increased sharply in 2007,but in 2008 and 2009 were more or less the same as in 2007.The price change corresponds to the time when listed firms were required to follow the new accounting rules.We thus conclude that the reform of the CAS has affected pricing in the audit market.

The price of audit products is determined by both the supply side and demand side.We argue that the main characteristics of the supply side are audit market concentration and audit product differentiation,and that audit risk is the main characteristic of the demand side of audit services.If the change in the CAS has affected audit fees,it must also be the case that the change in the CAS has led to a change in the concentration of the audit market,audit product differentiation or audit risk,or a combination of these,which in turn relates to a change in the final pricing of audits,as shown in the following diagram.

2.2.Audit market concentration

The new CAS implemented from 2007 onward are very different to the old CAS.First,many of the new accounting methods give firms more discretionary power.For example,according to the new rules,the consolidation difference in an acquisition at a premium is defined as goodwill.Intangible assets such as goodwill and trademarks need not be amortized and need only be evaluated annually.The impairment,if any,must be extracted.Further,one of the most important characteristics of the new CAS is the use of fair value as a new measurement attribute,which gives firms more room to change their accounting policy.Although the rules on asset write-downs reduce the opportunity for income management,the rules on the measurement of fair value,debt restructuring,non-currency asset exchange,R&D expenses relative to intangible assets and the capitalization of borrowing costs increase the opportunity for income management among listed firms.

Chart 1.Average audit price by year.

When firms comply with the new CAS to account for transactions,auditors must use more of their professional judgment in the audit process.As a consequence,high-quality audit firms may possess a greater competitive advantage,which will improve their market share and alter the concentration of the audit market.

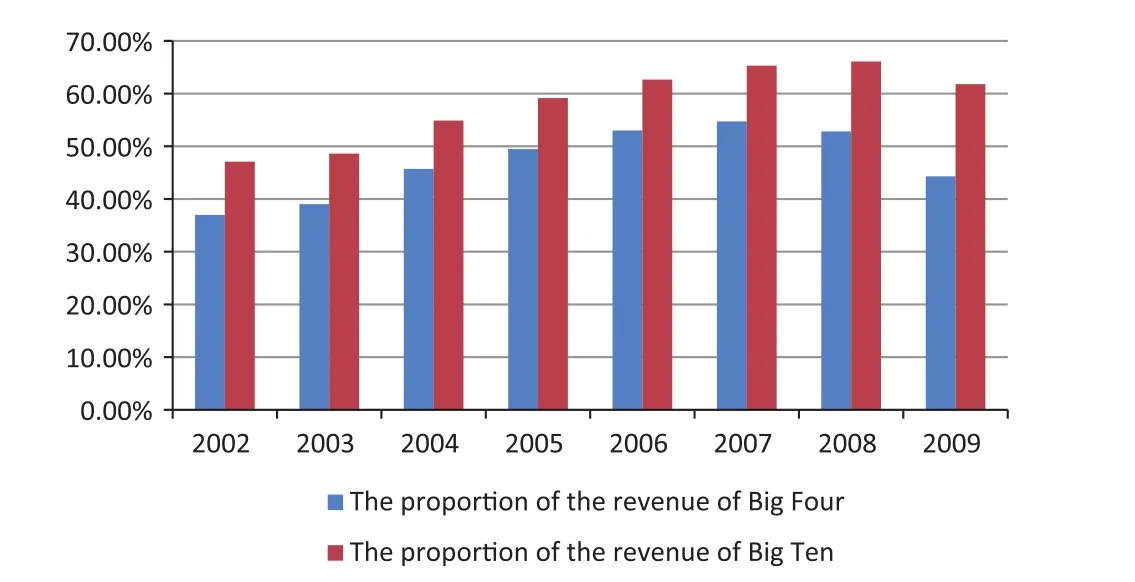

We use the ratio of revenue of the four(ten)largest audit firms(“Big Four”and“Big Ten”)to the 100 largest audit firms as the proxy for audit market concentration(see Chart 2).Past studies usually consider the Big Four to be a measure of high-quality audit firms,which is the reason why we use the ratio of the revenue of Big Four(Ten)to the 100 largest audit firms to measure audit market concentration.

The largest 100 audit firms are ranked based on the revenue of audit firms in a fiscal year.This information comes from the“Information on the National Top 100 Accounting Firms”announced by the Chinese Institute of Certified Public Accountants(CICPA).Between 2002 and 2009,the four largest firms were Price Waterhouse Coopers,KPMG,Deloitte and Ernst and Young.The remaining six firms in the Big Ten changed every year.

Chart 2 suggests that the concentration of the Big Four increased year by year in the sample period.Their market share was 36.98%in 2002,reached 54.72%in 2007 and then began to decrease.The ratio in 2009 was 44.3%.Using the information on the Big Ten to measure market concentration produces a similar result.We thus conclude that the adoption of the new CAS has not affected the concentration of the audit market significantly.

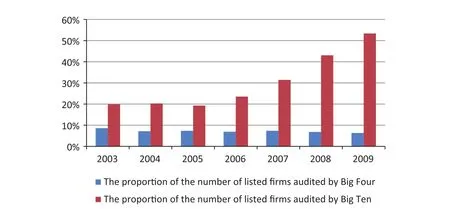

In accordance with the stipulation of the Ministry of Finance,listed firms began to follow the new CAS from 2007.The revenue of audit firms announced by CICPA include audit fees from non-listed firms,which may not match our sample firms,so we use another proxy for audit market concentration to reflect the influence of the adoption of the new accounting standards on the structure of the audit market:the total number of listed firms audited by the Big Four(Big Ten).

In Chart 3,we calculate the ratio of the number of listed firms audited by the Big Four to the number of all listed firms.We find that the ratio does not change significantly after the adoption of the new CAS,but that the ratio calculated with the number of listed firms audited by the Big Ten rises slightly.These results indicate that the change in the CAS has not led to a change in the concentration of the audit market.

2.3.Product characteristics:audit opinion

Chart 2.Ratio of the revenue of Big Four(Big Ten)to the revenue of the 100 largest audit firms.

An audit opinion is the judgment about a firm by auditors using accounting standards as the criterion.It provides assurance of the information contained in financial statements.We explore whether the change in the CAS has affected the type and content of audit opinions issued by audit firms,or more specifically whether the characteristics of the product provided by audit firms has changed with the adoption of the new accounting standards.Compared with the pre-2007 CAS,the new CAS place more emphasis on the professional judgment of auditors.This may have caused a change in audit quality requirements.If the required audit quality has increased,then auditors who possess greater professional knowledge are more likely to issue modified auditopinions(MAOs)when they audit the financial statements of listed firms.The number of MAOs should thus increase following the adoption of the new CAS.We examine the classified statistics on the audit opinions of listed firms between 2002 and 2009(see Table 1)and find that the number of MAOs and the ratio of the number of MAOs to the total number of audit opinions slightly decreased over the period,which is contrary to our conjecture.However,the decrease in the proportion of MAOs may in fact indicate that information disclosure quality has improved.In all,there is no conclusive evidence to indicate that the implementation of the new CAS has had a significant impact on the structure of the audit opinions of listed firms from the perspective of the industry structure of the audit market.

One of the most important characteristics of the new accounting standards is the adoption of fair value as a measurement base,in compliance with the IFRS.This raises the question of whether,in issuing their opinions, auditors pay more attention to the fair value factor since the change.To answer this question,we need to investigate the specific reason why some listed firms were given MAOs after the adoption of the new CAS. We examine all of the audit opinion reports and find that the reasons why auditors issued MAOs are mainly related to traditional problems such as uncertainty about accounts receivable,the possession of the funds of listed firms by controlling shareholders and related parties,obscure long-term equity investments caused by the losses of subsidiaries or affiliated companies,and so on,and that no firm was given an MAO because there was some flaw in the quality of information disclosed due to fair value.In all,we conclude that the change in the CAS has not had a significant impact on the content and quality of the products provided by auditors.

The results from these summary statistics show that the change in the CAS has not affected the concentration of the audit market or the differentiation of audit products.However,we do find that audit fees increased significantly after 2007.We thus argue that the change in CAS has caused expected audit risk to increase, which has in turn caused an increase in audit fees.

Whatever the audit market structure,the marginal return of audit services is always equal to the marginal cost in equilibrium,which is the condition that determines the audit price.As the audit market is not always competitive,the equilibrium price may be higher than the marginal cost.If the increase in audit fees is caused by supply side factors(audit market concentration and audit product differentiation),that is,if the increase in audit fees is caused by an increase in the degree of monopoly,then the difference between the audit price and its marginal cost will increase,which indicates that the resource allocation efficiency of the audit market willdecrease.Conversely,if the increase in audit fees is caused by demand side factors,that is,if audit fees are reasonable compensation for the elevated audit risk,then the increase is due to the increase in the marginal cost of the audit.In this case,the difference between the audit price and its marginal cost has not widened, which means that the resource allocation efficiency of the audit market has not deteriorated.

Chart 3.Ratio of the number of listed firms audited by the Big Four(Big Ten)to the total number of listed firms.

Table 1Proportion of each type of audit opinion.

We now examine how the adoption of the IFRS-based accounting standards has affected the expected audit risk and the determination of price when the audit market is in equilibrium.

3.Reform of accounting standards and audit fees:Theoretical analysis

As both direct users and assurers of the accounting information offirms,auditors need to assess the relevant audit risk based on the quality of the accounting information provided by firms.Accounting information risk(accounting information quality)is an important factor affecting audit risk.For example,when accrual items are higher(accounting information quality is lower),auditors are more likely to issue MAOs(Bartov et al.,2000),the probability of audit failure is greater(Geiger and Raghunandan,2002)and firms are more likely to change auditors to obtain a clean opinion(DeFond and Subramanyam,1998).These previous empirical results indicate that changing accounting information quality will influence audit risk.There are some similar empirical findings in China on this topic.For example,a return on equity(ROE)in the range of“Baopai”[In China,if losses have been incurred for 3 years in succession in any listed firm,then the stock of the listed firm is likely to be delisted.To avoid the occurrence of this situation,the listed firms will make use of various measures to be pro fitable and the behavior of these firms is called“Baopai”.The range of“Baopai”refers to ROE that falls in the range of 0-2%]is an important factor that significantly affects annual audit fees(Lina, 2003).The ratio of the amount guaranteed by other firms to total assets and the ratio of accounts receivable to total assets also significantly affect audit fees(Jixun et al.,2005).When listed firms change auditors,the new auditors are prone to use the degree of earnings management of the firm to measure audit risk and require higher fees as a result(Yanheng and Dequan,2005).Audit fees are also positively related to the difference between book income and taxable income(Qian and Zhou,2005).These research results from China suggest that the lower the accounting information quality of a firm,the higher the risk that auditors must bear and the higher the audit fees that they require as compensation for the elevated risk.Although the CAS changed,the ability offirms to generate cash flow did not change and the impact of the change in the CAS on audit pricing can thus be explained as the impact of the change of CAS on auditors’expected audit risk.

As stated,an important characteristic of the new CAS is that it uses fair value as an additional basic measurement attribute.When we examine the specific content of the new accounting standards,such as the standards on inventory,the restructuring of debt,consolidated financial statements,financial instruments and income taxes,we note that there are many changes.In general,the new accounting standards are greatly different in content and the application of the standards has become more complicated.Thus,the ability and professional judgment required of accountants is greater.

Under the old accounting standards,auditors formed stable expectations of the quality of accounting information and the related audit risk of the firms that they audited.Under the new accounting standards,auditors need to fully assess the audit risk offirms,especially the change in detection risk.The main factors of audit risk-inherent risk and internal control risk-did not change with the change in accounting standards.However,due to the introduction of the fair value measurement,auditors must reevaluate the fairness of the disclosed accounting information.The consequence for the whole audit market is an increase in detection risk and thus the overall audit risk,which has caused an increase in audit fees.

To control for the impact of the change in accounting standards on the comparability offinancial information,listed firms in China had to disclosure how their net income under the old standards changed under the new standards.Thus,there are two numbers for net income in 2006.Kai et al.(2009)argue that the adoption of the new CAS will increase the expected uncertainty of investors about accounting information quality. Under the old standards,investors could form relatively stable expectations about accounting information quality.In the transition to the new accounting standards,however,these expectations disappeared and new expectations had yet to be effectively formed,which increased investors’expected uncertainty about firms’accounting information quality and increased the cost of capital offirms and reduced their value.The change in the CAS may also have affected auditors’assessment of the risk offirms.There are two specific aspects offirm risk:market risk and information disclosure risk.According to the old accounting rules, which were based on historical costs,firms were not required to disclose their market risk.However,when the new accounting standards were implemented for the first time,the difference between the net income according to the old and new accounting standards reflected the market risk faced by firms to a certain degree.Market risk here refers to the potential impact of the change in the market price of assets on the continuing operations offirms.Even if investors can obtain information about firms’market risk through other channels,the duty of auditors is to provide assurances about the accounting information disclosed in financial reports.Once the information relevant to the risk is disclosed in the financial report,auditors must adjust their own risk expectations.When the influence of the change in accounting standards on the new income information is greater, the continued viability of the firms is more risky and the expected audit risk is higher.To compensate for the elevated expected audit risk caused by the increase in market risk,auditors must demand higher audit fees. This leads to our main hypothesis.

H1.The greater the impact of the change in CAS on firms’accounting information,the greater the increase in audit fees.

4.Research design

4.1.Sample selection

We select 802 non-financial listed firms that disclosed in their financial reports the relevant adjustment data about net income according to the rules for the fiscal year 2007 as our research sample.We exclude the following firms:(1)financial firms;(2)firms for which the relevant data cannot be found(including observations for which the audit fee or the value of equity is missing);and(3)firms with MAOs(including clean opinions with an emphasis of matter,modified opinions,opinions with disclaimers and adverse opinions).

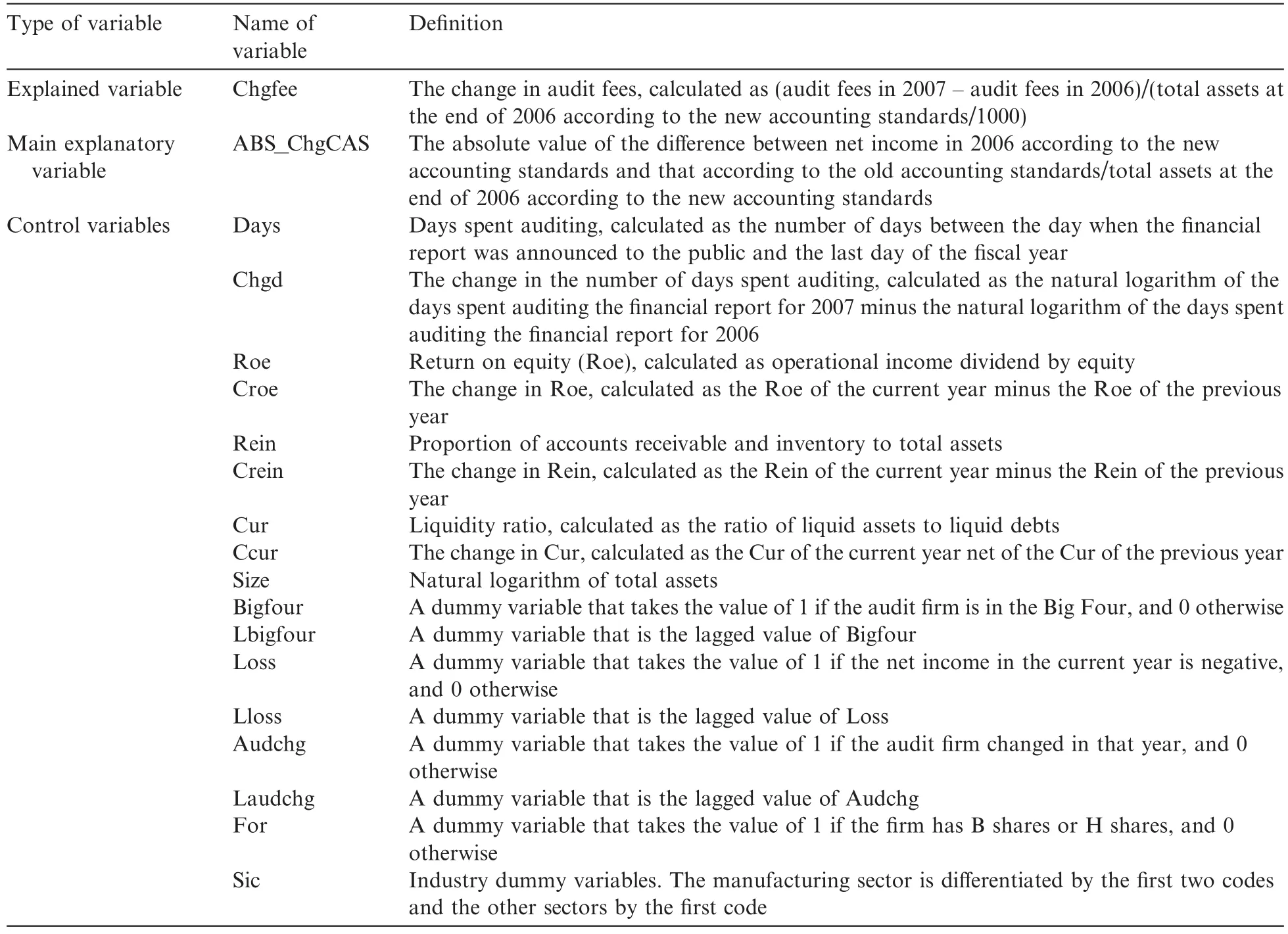

To test the main hypothesis,we construct the following model.Based on the research of Kai et al.(2009), we use the absolute value of the difference between the old and new accounting standards(the degree of adjustment between the two standards)as the proxy for the impact of the change in accounting standards on earnings information,and test how this value is related to the change in audit fees.The specification of the variables is shown in Table 2.

The main explanatory variable ABS_ChgCAS is a proxy for the degree of adjustment between the old and new accounting standards.According to the theoretical analysis,the greater the impact of the adoption of the new CAS on the earnings information offirms,the higher the market risk embedded in earnings information and the higher the audit fees paid.Thus,the coefficient β1of the main explanatory variable ABS_ChgCAS should be significantly positive.

The increase in audit fees may also be caused by an increase in auditors’expenditure on learning the new rules and carrying out their business.The new CAS based on fair value are significantly different from the old CAS.As a result,auditors have had to study the new rules to use the new standards effectively.When auditors spend more time on or devote more energy to auditing,they charge higher audit fees in compensation.We thus add Chgd to the model as a control variable.

According to the research of Simunic(1980),Wang(2002)and Bing et al.(2003),the main factors that affect audit fees include firm size,the complexity of the audit,the audit risk of the firm,the characteristics of the audit firm and other characteristics of the audited firm.Much research indicates that firm size is the main determinant of audit fees,and total assets are usually considered to control for the influence of size.Here,we use the natural logarithm of the total assets of the firm(Size)to proxy for the size of the firm.We use the ratio of the sum of accounts receivable and inventory to total assets(Rein)to proxy for the complexity of auditing the firm.Return on equity(Roe),current ratio(cur)and a loss dummy variable(Loss)to measure the audit risk caused by firmcharacteristics.We use another dummy variable(Bigfour),which is equal to 1 if the audit firm is in the Big Four,to measure the main characteristic of the audit firm.Whether or not listed firms change auditors may be correlated with instances where firms and auditors do not agree on the amount of audit fees payable.Thus weuse a dummy variable to control for this situation.Because the dependent variable is the change in auditfees, we use the change in the continuous variables Roe,Rein and Cur(Croe,Crein,and Ccur)as control variables and add the lagged variables(Lbigfour,Lloss,and Laudchg)of the indicator variables Bigfour,Loss and Augchg as control variables.As the purpose of establishing the new accounting standards was to align with international conventions,the new CAS often refer to IFRS.As listed firms that have issued B shares or H shares are more familiar with IFRS than those that have not issued such shares,the costs of implementing the new standards are different for these two types offirms.Thus we add another dummy variable that is equal to 1 if the listed firm has B shares or H shares(For)to control for this difference.

Finally,to remove the influence of potential outliers,we winsorize the top and bottom one percent of the distributions of all of the continuous variables.

Table 2Variable definitions.

5.Empirical results and analysis

5.1.Descriptive analysis

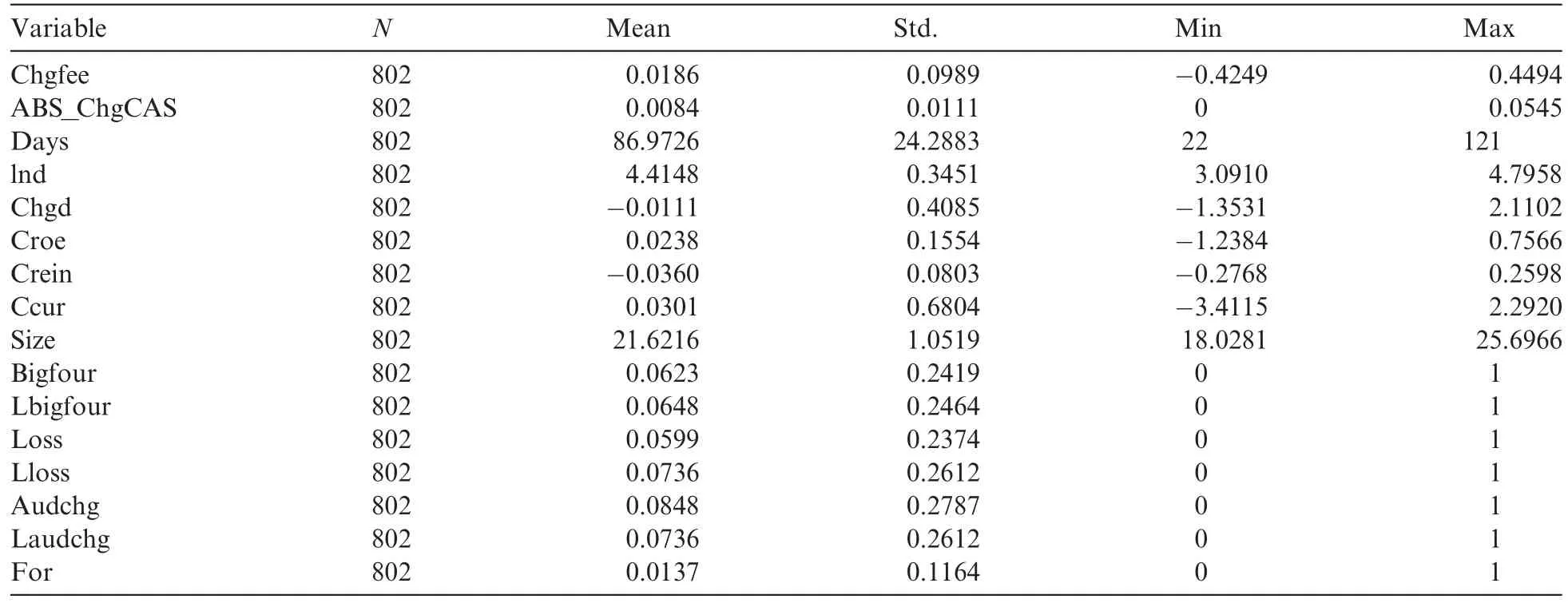

The descriptive statistics in Table 3 show that the average change in audit fees in 2007 is 0.0186.The average audit fee in one thousand-yuan total assets caused by the reform of the CAS is about 0.02 yuan.The difference between net income according to the old and new CAS(ABS_ChgCAS)is 0.008 on average, which suggests that the difference in net income in one-thousand-yuan total assets is 0.8 yuan.

Days is the time between the end of the fiscal year and the announcement date of the financial report,and lnd is the natural logarithm of Days.Among the 802 firms,the shortest period is 22 days,the longest period is 121 days and the average period is 86.9726 days.Chgd is the difference between lnd in the current year and lnd in the previous year.The average Chgd is-0.01,which suggests that the time spent on auditing financial reports in 2007 is only slightly less than the time spent in 2006,which implies that the change in the CAS has not significantly increased the time that audit firms spend auditing.

Table 3Descriptive statistics.

5.2.Regression analysis

To control for the potential influence caused by sample selection bias,we first use our sample to test the model of Simunic(1980)and Gul(1999).If the result is generally consistent with the results in these past studies,then we can conclude that our findings are not caused by the uniqueness of the selected sample.The descriptive statistics for the industry structure of the audit market suggest that audit fees increased signif icantly after the change in the CAS.The question then arises as to whether this increase in audit fees is due to changes in the characteristics offirms or to the changes in the CAS.The foregoing analysis does not give direct evidence on this,which is the question that the hypothesis testing is attempting to answer.

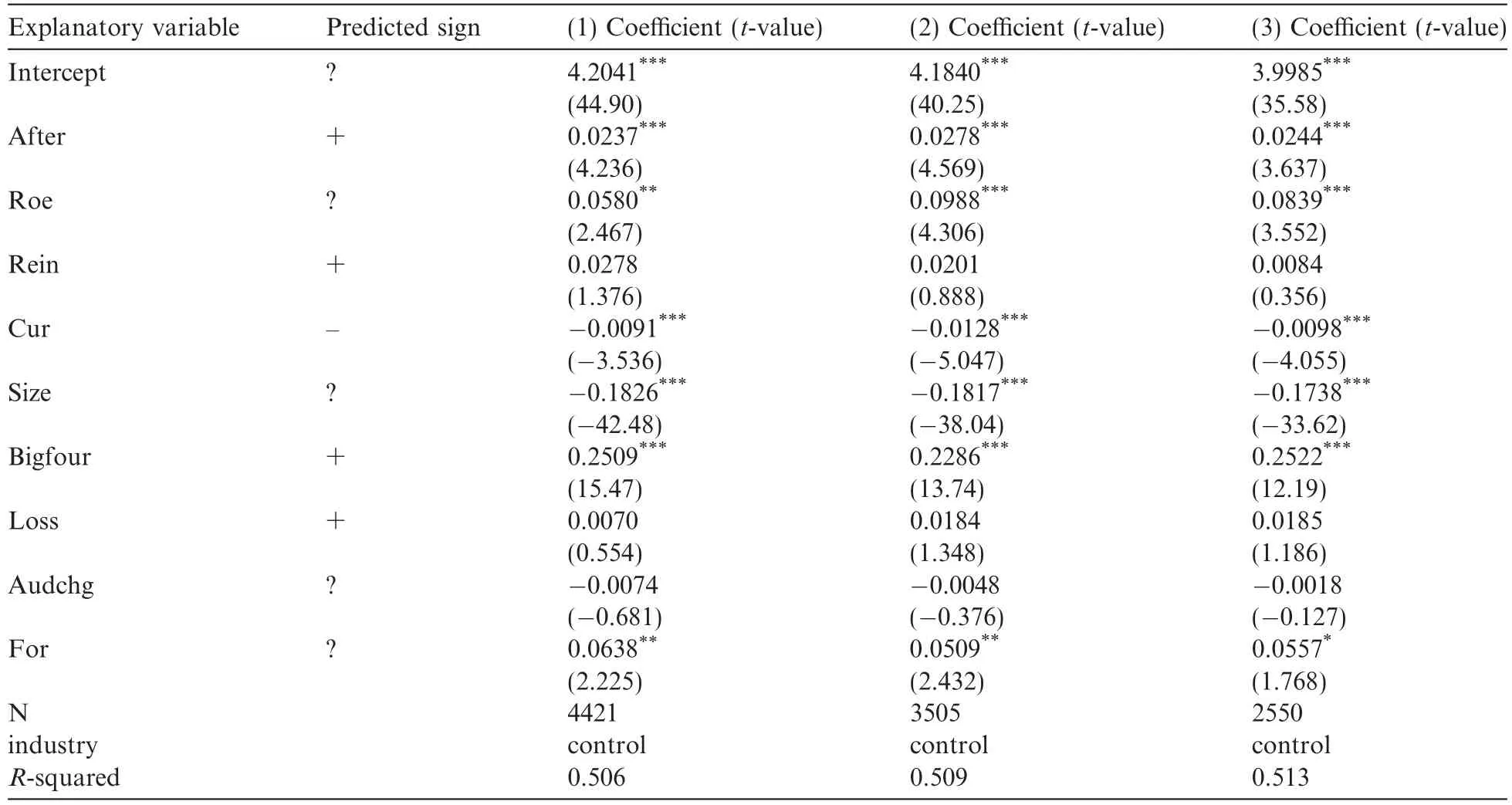

Table 4 shows the results of a regression using our sample of the main variables from the model of Simunic (1980)and Gul(1999)to test for the influence of sample selection bias in our research sample and to test whether audit fees increased significantly following the change in the CAS.

The first regression in Table 4 presents the results for the sample of all listed firms for the period 2004-2008. The second regression presents the results for the sample excluding the observations from 2006,as we consider 2006 to be the transitional period during which the CAS changed.The sample in the third regression includes only observations of listed firms that existed in all years between 2004 and 2008(balanced panel data).The regression results are generally consistent those reported by Simunic(1980)and Gul(1999).Specifically, the coefficient of Cur is significantly negative,which suggests that the higher the liquidity of a firm,the lower its financial risk,the lower the audit risk and the lower the audit fee charged by auditors to audit the firm.The coefficient of Bigfour is significantly positive,which means that the audit fees paid to the largest four audit firms are significantly greater than those paid to other audit firms.The coefficients of Rein and Loss are positive as predicted,but the results are not statistically significant.All of the results based on our sample are generally consistent with previous results,indicating that there is no selection bias in our sample.

Table 4Regression results for the traditional audit pricing model.

In the regression results for the three samples,the coefficient of the dummy variable After is significantly positive and the magnitude of the coefficient ranges from 2%to 3%,which suggests that audit fees increased significantly after the implementation of the new CAS in 2007 and 2008.In other words,the implementation of the new CAS led the audit fees for every thousand yuan in assets to increase from 2%to 3%.The actual audit fees increased from 6,00,000 yuan to 8,00,000 yuan after the adoption of the new CAS,an increase of almost one third(80/60-1).Thus,the impact of the change in the CAS on audit market equilibrium pricing is not only statistically significant,but also economically significant.

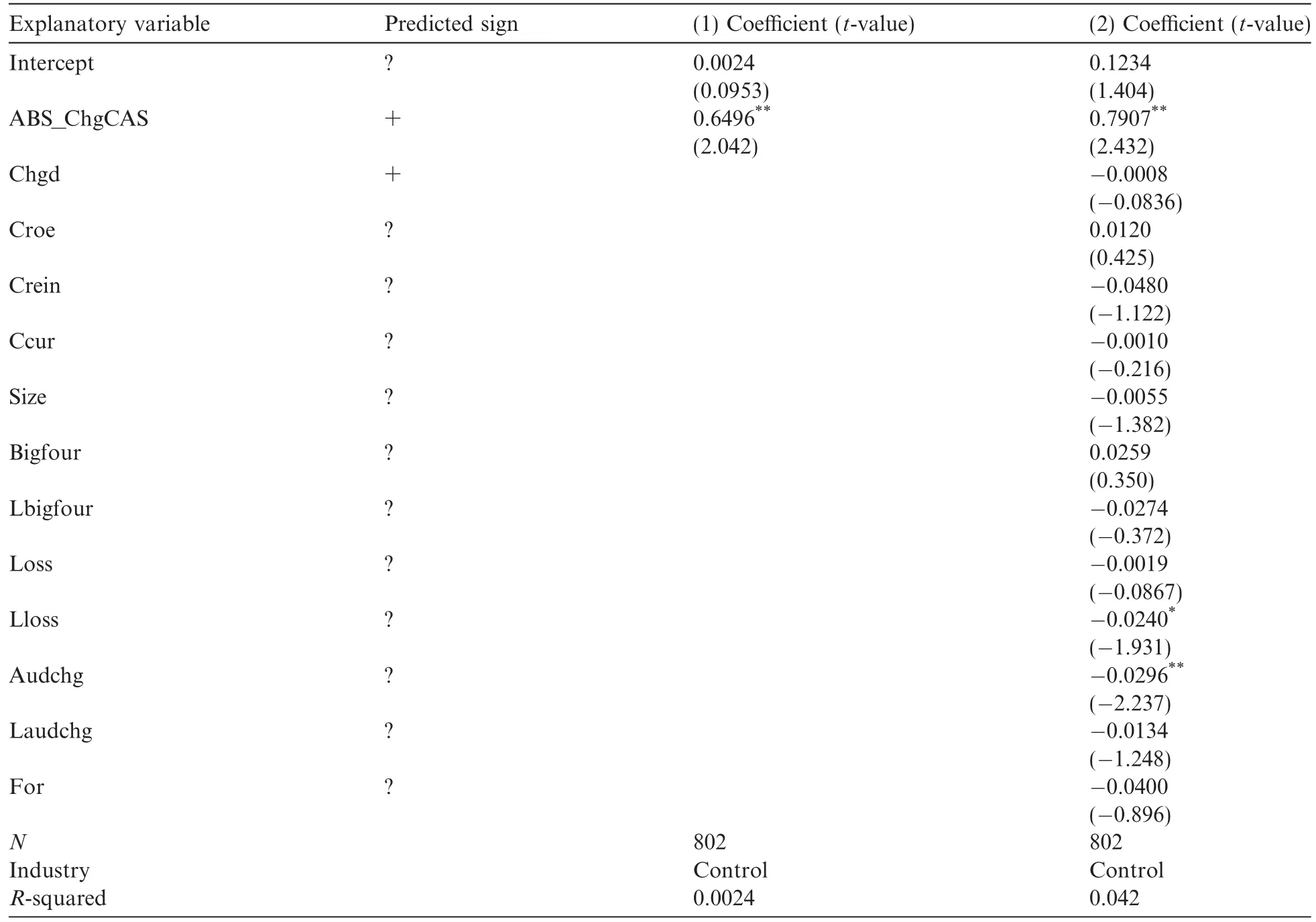

Table 5 presents the regression results for our main hypothesis test.The first regression considers ABS_ChgCAS to be the main independent variable and does not control for any other variables except for industry.The second regression controls for all of the other variables.Whether or not we control for other variables,the coefficient of ABS_ChgCAS is significantly positive at a significance level of greater than 5%. This result supports our main hypothesis that the larger the impact of the change in the CAS on firms’accounting information,the greater the change in audit fees.This result is economically significant.When the difference in net income under the two standards increases by 1%in every thousand-yuan assets,the audit fee increases by 0.79%.

To measure the potential influence of time spent auditing on audit fees,we add the period between the end of the fiscal year and the announcement day of the yearly financial report Chgd as the proxy for auditing time. The results in Table 5 shows that the coefficient of Chgd is negative but not significant.This result suggests that the actual time spent auditing does not significantly affect the audit pricing decisions of auditors.The coefficients of Bigfour and Lbigfour are not statistically significant,which confirm the conclusion reached from the descriptive statistics that the change in the CAS has not significantly influenced audit market concentration,and thus the concentration of the audit market does not have the ability to explain the change in audit pricing.All of the other control variables are generally not statistically significant,except for Audchg, which is significantly negative,indicating that the reason why firms replace their audit firm may be that they do not want to pay excessive audit fees.

Table 5Regression results for the main model.

6.Conclusion

This study investigates how the change in accounting standards in China in 2007 has influenced audit equilibrium pricing.As auditors are the direct users of accounting information,the questions of whether and how the change in accounting standards has affected the industry structure and audit prices has become a common concern for academics and business practitioners alike.

We investigate the impact of the change in the CAS on audit pricing from three dimensions:the concentration of the audit market,the differentiation of audit products and audit risk.The results suggest that audit fees increased significantly after the adoption of the new CAS.However,the change in accounting standards did not increase the concentration of the audit market significantly,as larger audit firms have not displayed scale superiority or further increased their market share.The structure of audit opinions(the ratio of the number of MAOs to the total number of audit opinions)as the final product of audit services has also not changed significantly,and the specific reason why MAOs were issued in the sample period is not directly linked to the change in the CAS.We thus argue that the change in the CAS has affected audit pricing due to changes in audit risk.

We analyze the potential influence of the change in the CAS on audit pricing from the perspective of information disclosure risk.The change in accounting standards makes firms disclose more information that is relevant to market risk,which increases firms’information disclosure risk.As a consequence,auditors are confronted with higher audit risk and charge higher fees as compensation.

An important implication of our research is that the increase in audit fees during changes in accounting standards should be considered as a potential cost of the reform of the rules.However,although audit fees increase from the perspective of a single firm,the resource allocation efficiency of the audit market as a whole does not deteriorate.This is because the marginal return is always equal to the marginal cost in equilibrium, and it is the increase in audit risk caused by the change in the accounting standards that leads to an increase in the marginal cost of auditing that elevates audit fees.That is,the change of rules does not widen the gap between audit prices and the marginal cost of auditing,and does not lead to a deterioration of the resource allocation efficiency of the audit market.However,the increase in the expected risk of auditors caused by the difference between the old and new accounting standards causes auditors to pay more attention to audit risk relative to asset value and to charge higher audit fees as a result.This can be regarded to a certain extent as a signal to investors to pay more attention to the market risk of the operating activities of listed firms.

Barth,Mary.,Taylor,Daniel.,2009.In defense of fair value:weighing the evidence on earnings management and asset securitizations. Journal of Accounting and Economics 49,26-33.

Barth,M.E.,Landsman,W.R.,Lang,M.H.,2008.International accounting standards and accounting quality.Journal of Accounting Research 46,457-498.

Bartov,E.,Gul,F.A.,Tsui,J.S.L.,2000.Discretionary-accruals models and audit qualifications.Journal of Accounting and Economics 30,95-119.

Bing,Liu.,Jianzhong,Ye.,Yingyi,Liao.,2003.The empirical research about the affecting factors of the audit charge in listed firms in China.Auditing Research 1,44-47.

Dechow,P.,Myers,L.,Shakespeare,C.,2009.Fair value accounting and gains from asset securitizations:a convenient earnings management tool with compensation side-benefits.Journal of Accounting and Economics 49,2-25.

DeFond,M.L.,Subramanyam,K.R.,1998.Auditor changes and discretionary accruals.Journal of Accounting and Economics 25,35-67.

Geiger,M.,Raghunandan,K.,2002.Auditor tenure and audit quality.Auditing:A Journal of Practice and Theory 21,187-196.

Gul,F.A.,1999.Audit prices,product differentiation and economic equilibrium.Auditing:A Journal of Practice and Theory,90-100.

Jixun,Zhang.,Yin,Chen.,Xuan,Wu.,2005.The analysis of the impact of the risk factors on the audit fee in listed firms in China. Auditing Research 4,34-38.

Kai,Zhu.,Xuyin,Zhao.,Hong,Sun.,2009.The reform of the accounting standards,information precision and value relevance. Management World 4,47-54.

Lina,Wu.,2003.The analysis of the impact of earnings management on the audit fee.Accounting Research 12,39-44.

Simunic,D.A.,1980.The pricing of audit services:theory and evidence.Journal of Accounting Research 16,161-190.

He Xianjie,2009.The implementation effect and the economical consequence.Doctoral dissertation at the Shanghai University of Finance and Economics.

Yanheng,Song.,Dequan,Yin.,2005.The change of audit firm,audit fee and audit quality.Auditing Research 2,72-77.

3 November 2011

*Corresponding author.

E-mail addresses:aczhuk@mail.shufe.edu.cn(K.Zhu),sophiesun126@gmail.com(H.Sun).

China Journal of Accounting Research2012年2期

China Journal of Accounting Research2012年2期

- China Journal of Accounting Research的其它文章

- State control,access to capital and firm performance

- Board independence,internal information environment and voluntary disclosure of auditors’reports on internal controls

- Relative performance evaluation and executive compensation: Evidence from Chinese listed companies

- Government auditing and corruption control:Evidence from China’s provincial panel data