MYTHICAL BEASTS

2018-07-02 22:34ByDengYaqing

Beijing Review 2018年24期

By Deng Yaqing

Chinas new-look economy is gain- ing momentum. With focus having been laid on entrepreneurship and innovation, a cluster of privately owned and rapidly growing startups have provided a boost for the country as it undergoes a momentous shift in growth drivers.

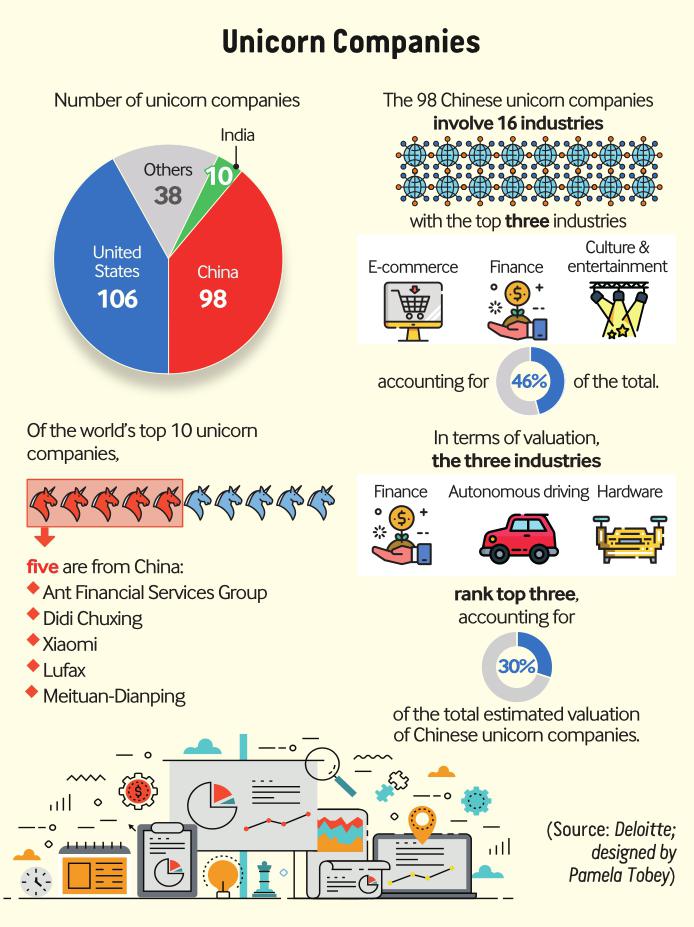

According to a study released by Deloitte, by the end of June 2017 there were 252 unicorns—startup companies valued at over$1 billion—worldwide, 106 and 98 of which were in the United States and China respec- tively, far surpassing every other country.

“Chinas innovation capacity is now largely on par with Americas, which is reflected by the robust growth of Chinese unicorns. Most of these companies are excellent performers and frontrunners in their respective fields,” said Albert Wang, founding partner of Maintrend Capital and former partner of SAIF Partners, in an interview with Beijing Review.

Xiaomi, a Beijing-based unicorn heavyweight specializing in consumer electronics, recently filed to go public in Hong Kong, where it could raise about $10 billion in the largest listing globally in almost four years. Meanwhile, there are sources suggesting that the smartphone giant may enter the A-share market through the issuance of Chinese Depositary Receipts (CDRs).

Chinese mainland and Hong Kong securities regulators are sparing no effort to attract unicorn companies by improving their listing policies. On June 6, China Securities Regulatory Commission (CSRC) issued rules on a test run for the issuance and trading of CDRs. The securities regulator has also released amended rules on IPO and a package of measures to support unicorn companies in their domestic issuance of stocks or CDRs. Meanwhile, the Hong Kong Stock Exchange has permitted the listing of innovative, highgrowth companies with a dual-class stock structure, according to which Xiaomi can get listed.

“Increasing consumption capacity, improving productivity and abundant entrepreneurship have provided the necessary conditions and resources for Chinese companies to grow and prosper,” Wang said.

“However, the strict requirements and high threshold for getting listed in the domestic market and the American stock markets lukewarm attitude toward Chinese firms have long denied these companies the opportunity to raise capital in the secondary market. They have no choice but to finance in the primary market, which explains the birth of so many unicorns,” Wang continued, predicting that an increasing number of Chinese unicorns will seek to accomplish IPOs in the Chinese mainland and Hong Kong as their business grows.

Core competitiveness

Innovation and a favorable business environment have set the stage for Chinas new era of fast-growing unicorns. Yet, while some of the top companies in this group will find success in the secondary market, other less competent ones could lag behind or even collapse.

“Besides the ability to attract capital, unicorns need to foster and maintain the ability to innovate in order to survive, which focuses more on integration and making use of various market resources than sticking to the development of a certain technology in the laboratory,” Gao Yuning, an associate professor with the School of Public Policy and Management at Tsinghua University, told Beijing Review.

Such innovation could involve a variety of technologies which are not necessarily developed by China, but can nonetheless be consolidated by Chinese unicorns in an efficient way to form a new secure and effective business model.

“A unicorn should be able to grow into a platform company rather than relying entirely on a single technology, and only in this way can such a company realize sustainable and rapid development,” Li Lixin, Managing Director of Northern Light Venture Capital, told Beijing Review.

“Many great companies which have gone on to be listed are platform companies, such as Alibaba, Tencent and Didi Chuxing. Such a company represents a certain business environment in which a host of small and medium-sized companies reside,” said Li.

A unicorn also needs to maintain a leading position in a certain section of the market and dig deeper into this area rather than blindly seeking expansion so that it can develop superior services and products to better satisfy market demands, said Gao.

At the heart of a unicorns competitiveness is its ability to address the urgent needs of consumers, Gao added. Take shared bikes for example. The companies offering this service do not rely on particularly advanced or hard-to-come-by technology, but they have nonetheless managed to provide a service which people need and the demand for which is inexhaustible.

“Competition here is more brutal and fierce than in the American market and so a fast learning team is indispensable. Financing capacity as well as shareholder structure also play an important role. In some cases, companies which provide products and services of the same quality experience totally different outcomes due to disparities in the above-mentioned areas,” said Wang.

Potential challenges

“Funding and innovation are two essential factors for corporate growth. However, exces- sive financing and innovation may generate bubbles which, once they burst, may affect the confidence of entrepreneurs, investors and governments,” said Wang.

As the struggle among platform companies continues, competition over consumerstime, attention and energy is intensifying.

“What matters is whether a company can create the value that consumers really need. Here value means not economic benefit, but knowledge, entertainment, relaxation and so on,” said Gao.

Alongside market value, requirements for corporate social responsibility have steadily risen, as seen by Didi Chuxings supervision over its drivers and transactions, and Internet lending platforms duty to protect personal data and fend off financial risks, said Gao.

“Moreover, as established unicorns which thrive by adjusting their business models continue to expand their territories, fledgling companies may find themselves squeezed. On the flip side, if technology companies fail to grow fast enough, they will likely be outstripped by industry newcomers with greater momentum,” said Li.

Further opening up

There is no doubt that the Chinese Government wants to see successful companies choose to go public in the mainland or Hong Kong markets, so that Chinese people can share in the rewards of the new economy.

“In the past, the strict requirements and extensive restrictions of the A-share market deterred numerous unicorns from attempting to get listed at home. Now, with the threshold lowered, a new trend of domestic IPO applications is taking shape, and the international competitiveness of Chinas capital market will be further improved,” said Li.

Conversely, CDRs usually find their way in developed and mature fi nancial markets, and the issuance of CDRs in domestic stock markets necessitates higher requirements for supervision, access to information and investor protection.

From June 7, qualified innovative firms can submit applications for CDR issuance to the CSRC under the new pilot CDR program. The CSRC said it will strictly control the number of enterprises and the volume of funding for the pilot CDR program, and properly arrange the timing and pace of CDR issuance.

“By learning from more mature overseas market, China should establish a comprehensive financial supervision system featuring cross-market and joint operation,” said Gao, who also emphasized the protection of intellectual property rights and the release of more tax credits to encourage innovation.

“More efforts should be made in opening up, such as allowing cross-border capital and profi t fl ow for fast-growing privately held companies,” said Gao, who expects these enterprises to enjoy the same equal treatment and preferential policies as foreign-funded companies.

“As more Chinese unicorns look to go public by issuing CDRs in the mainland market, there will be a huge demand for capital, while giant companies currently listed in the A-share market will carry out additional issuance. It is beyond the capacity of the present capital market to fill the gap in capital demand,” said Li, noting that efforts need to be made to increase the supply of funds.

To address the problem, China needs to widen its capital sources by allowing more overseas funds to flow into its stock market. According to Wang, in the process of enabling unicorns to go public at home, the Chinese authorities should push for the free convertibility and internationalization of the yuan and press ahead with the opening up of Chinas stock market.

At the same time, investor structure should be optimized. “In Chinas stock market, about 80 percent of players are private investors, while in overseas markets the majority of market players are institutional investors. It follows that private investors should be encouraged to entrust their money to institutional investors who are more professional, rational and are better equipped to withstand fluctuations and risks,” said Wang, adding that the country should also allow more private and overseas money to enter the stock market.

“However, the steps toward opening up should be in line with Chinas current economic stature and global investorsconfi dence in the country. Otherwise, problems may occur,” said Wang, citing rampant speculation on the Thai baht and Russian ruble, which he believes is the consequence of disproportionate opening up.