Why China’s Socialist “Supply Side Reform” Outperforms the West’s “Half Keynes” Model

2016-02-05 07:13:16ByJOHNROSS

CHINA TODAY 2016年11期

By JOHN ROSS

Why China’s Socialist “Supply Side Reform” Outperforms the West’s “Half Keynes” Model

By JOHN ROSS

John Ross is a senior research fellow at Chongyang Institute for Financial Studies, Renmin University of China. From 2000 to 2008 he was director of economic and business policy in the administration of Mayor of London Ken Livingstone. He previously served as adviser to several major international mining, finance and equipment manufacturing companies.

AS the end of 2016 approaches, the results of the two main international approaches taken this year by major economies to deal with the negative trends in the global economy which have continued since the international financial crisis can be compared. These are China’s “supply side”policies compared to the G7’s “demand side” ones –the latter primarily being monetary policies such as quantitative easing (QE).

Data on the global economy confirms the success of China’s response compared to the West’s. But this success of China’s supply side approach is not merely “pragmatic” but flows from fundamental issues of economic theory. China’s “supply side” approach further refnes the point emphasized by Xi Jinping that China is prepared to use both “visible” and ‘invisible” hands in economic development. Within the overall framework of a “socialist market” economy China is able to use the “visible hand”to close excessive capacity, upgrade supply and infrastructure, which aids market development and division of labor, and to undertake investment to stimulate growth and regional and industrial development.

In the fnal analysis, China’s more successful response to the international fnancial crisis compared to the Western economies shows in practical terms the superiority of a socialist to a capitalist economic system. In contrast the incoherence of contemporary Western economics is shown in it presenting even Keynes as a purely “demand side” economist – which as will be seen is a misrepresentation of Keynes’ own views.

First the facts regarding trends in the major economies will be established and then why China’s supply side response has been more successful than the West’s demand side one will be analyzed.

The Global Economy

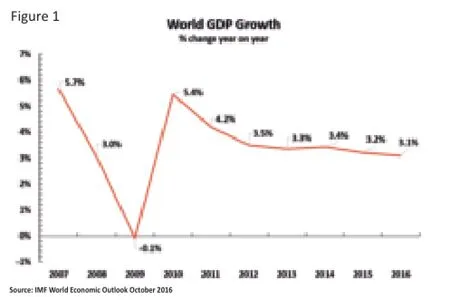

Taking frst the international context, negative trends in the global economy have continued since the international fnancial crisis. As Figure 1 shows, world economic growth, after recovering in 2010 to essentially pre-crisis growth rates, has slowed since. Global economic growth fell from 5.4 percent in 2010 to the IMF’s latest estimate of 3.1 percent in 2016.

Figure 2 shows in more detail the recent developments in main global economic centers – the U.S., China, EU, and Japan – giving the trends in economic growth from the beginning of 2015 to the second quarter of 2016.

• Japan has only recovered from negative to a very small 0.8 percent positive growth.

• EU annual growth has fallen slightly from an already low level – declining from 2.1 percent to 1.8 percent.

• The U.S. economy, which after 2008 achieved more substantial recovery than other Western countries, suffered a sharp slowdown in 2015-16 with annual growth declining from 3.3 percent to 1.2 percent.

• China continues to substantially outperform the Western economic centers. In the second quarter of 2016 China’s growth of 6.7 percent was over fve times as fast as the U.S. Unlike the U.S., annual growth in China’s economy has only slowed slightly in the recent period from 7.0 percent to 6.7 percent.

China’s economy has therefore not only outperformed over the period since the international fnancial crisis began, with cumulative China GDP growth in 2007-15 being 93 percent compared to 10 percent for the U.S., but has also continued to outperform in the most recent period.

Supply Side vs Demand Side Responses

Turning to the reasons for these global trends, the difference in approach between China’s supply side reform and the West’s demand management is clear.

The fundamental policy tool used by all major Western economies to attempt to deal with the consequences of the international fnancial crisis has been monetary QE. The aim of QE’s massive asset, above all bond, purchases by central banks has been to try to lower interest rates.

The QE policy is directly taken from Keynes and fows from his observation that in a modern economy investment is fundamentally fnanced by borrowing. Therefore, willingness to invest depends on the relation between the proft and interest rates. Lowering interest rates aims to reduce borrowing costs compared to profts, thereby increasing the attractiveness of investment, and therefore demand for investment. This half of Keynes’ analysis and policies focusing on the demand for investment, accurately follows from these views.

But unfortunately for the coherence of contemporary Western economic policy this was only half Keynes’ argument. Keynes argued that measures to increase demand for investment by lowering interest rates would be inadequate. Therefore, the state would have to undertake direct supply side measures – ensuring an adequate investment supply.

Keynes noted: “I am now somewhat sceptical of the success of a merely monetary policy directed towards infuencing the rate of interest… I expect to see the State…taking an ever greater responsibility for directly organizing investment.” Consequently, Keynes believed regulation of the level of investment would have to be undertaken by the state, not by the private sector: “I conclude that the duty of ordering the current volume of investment cannot safely be left in private hands.” It was necessary to aim at“a socially controlled rate of investment.” But if the state were to determine “the current volume of investment,” this led Keynes to his conclusion: “It seems unlikely that the infuence of banking policy on the rate of interest will be suffcient by itself to determine an optimum rate of investment. I conceive, therefore, that a somewhat comprehensive socialization of investment will prove the only means of securing an approximation to full employment.”

Keynes noted that this “somewhat comprehensive socialization of investment” did not mean the elimination of the private sector, but of state investment operating together with a private sector – rather similar to the combination of the “visible hand” and “invisible hand” analyzed by Xi Jinping. As Keynes noted: “This needs not exclude all manner of compromises and devices by which public authority will cooperate with private initiative… apart from the necessity of central controls to bring about an adjustment between the propensity to consume and the inducement to invest there is no more need to socialize economic life…. The central controls necessary to ensure full employment will, of course, involve a large extension of the traditional functions of government.”

“Half Keynes”

There are other reasons to reject Keynes overall analysis, for example he was a protectionist, nevertheless the presentation of Keynes as a purely “demand side” economist is false as shown above. What the West has presented as “Keynesianism” since the international financial crisis may be accurately termed “half Keynes.” The U.S. and other economies actively used Keynes’ demand side tools, with QE to lower interest rates, but they rejected Keynes supply side measures, the “somewhat comprehensive socialization of investment” and the need for “a socially controlled rate of investment.”

But events since the beginning of the international fnancial crisis have vindicated Keynes’ view that “I am…sceptical of the success of a merely monetary policy directed towards infuencing the rate of interest.” The huge QE programs have failed to relaunch investment and growth in Western economies. But Western economies have rejected the “supply side” of Keynes’ argument –that “the duty of ordering the current volume of investment cannot safely be left in private hands.” The reason for this is straightforwardly that Western economies are capitalist economies.

China’s socialist economy, however, has no compunction about using the visible hand as well as the invisible one – the state as well as the private sector. Once, however, the state begins to undertake a role in investment it cannot invest, or hold back investment, “in abstract” –that is without investing in particularly sectors. It must decide on the key investment priorities – it must have an“industrial strategy.” Given China’s orientation to create a socialist market economy and its present level of development these must include in particular:

• To lay the basis for more effective market functioning and division of labor – for example, China’s per capita has only seven percent of the railway length, 16 percent of the road length of the U.S., and less than one third of the electricity power supply of the U.S., making it impossible for China’s logistics and market infrastructure to function as effectively as the U.S.

• To upgrade productivity and proftability by closing low productivity/low profitability production in industries with excess capacity.

This is the combination of the “visible hand” and the“invisible hand” outlined by Xi Jinping.

The facts since the beginning of the international financial crisis confrm that China’s response has been superior to that of the West. But the reasons are therefore not purely pragmatic. They are rooted in fundamental questions of economic theory and the superiority of the structure of China’s socialist economy compared to Western capitalist economies.