Remaking“Made in China”

2013-04-29 13:44ByHUJIANGYUN

CHINA TODAY 2013年7期

By HU JIANGYUN

WHAT does “Made in China” mean to you? In the past, Chinese exports were synonymous with lowgrade throwaways, like plastic fittings, rubber tubes and Christmas decorations.

Those days are long gone. China currently ranks No. 1 in the world for both production and export of manufactures. With sharp rises in the countrys export volume of technologyintensive products, the image of “Made in China” is receiving a thorough makeover.

Since the most recent global financial crisis, Chinas industrial structure has been upgraded and the countrys industries have developed in leaps and bounds. Low quality and high volume has been replaced with high quality and, well, high volume.

Of the 500-plus industrial products that China produces, the outputs of over 220 products have climbed to the top of their respective world rankings. These include low value-added products like crude steel, cast iron, cement and coal, and medium value-added items such as automobiles and chemical fertilizers.

The financial crisis hastened the rise of Chinese exporters. In aspects of production, the three major developed economic entities, namely Japan, the U.S. and the E.U., have all seen recession. The impact of recession is shown in Graphic 1.

The index of industrial production (IIP) takes 2005 as the base year. The base value is 100 points. From the second quarter of 2008 to the first quarter of 2013, the IIP of Japan first dropped sharply from 107.9 to 75.2 by the first quarter of 2009. For the rest of the period it remained around 95. The IIP of the U.S. declined from 103.5 to a low point of 88.3 in the second quarter of 2009, before undergoing a four-year recovery to reach pre-crisis levels in the first quarter of 2013. The IIP for the 27 countries of the EU went from 108.7 in the first quarter of 2008 to 89.9 in the second quarter of 2009, before fluctuating under the impact of the European sovereign-debt crises. By the first quarter of 2013 European IIP was yet to recover to the 2005 base year level. Although China doesnt produce IIP statistics, the country has performed better post-crisis than Japan, the U.S. and the EU. By way of comparison we can gain a glimpse of Chinas industrial performance by contrasting the growth rate in Chinas industrial added value with those three entities IIP. (See Graphic 1)

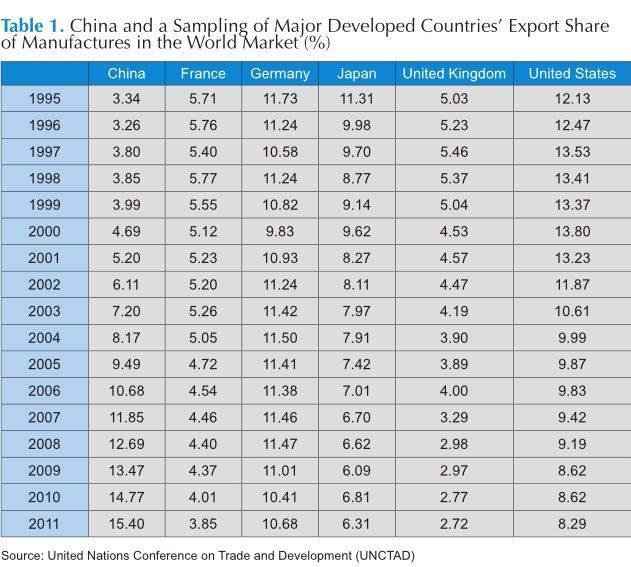

In terms of exports, from 1995 to 2011 the share of Chinese manufactures in the world market increased from 3.34 percent to a leading position of 15.4 percent, as shown in Table 1. Beginning in 2000 Chinas world market share ticked up by one integer every year, while that of other major developed countries, with the exception of Germany, continued to shrink.

The market shares of Chinese exports of both labor-intensive, resource-based manufactures and manufactures with low skill and technology intensity are No.1 globally. High-tech, high-value-added manufactures were late to the game, but today they are world-beaters as well. In the period from 1995 to 2011, the global market share of labor-intensive and resourcebased products rose 19.34 percentage points; that of low skill and technology intensity goods rose 13.01 percentage points, while market shares of manufactures with medium skill and technology intensity and high skill and technology intensity rose by 8.48 percentage points and 13.02 percentage points respectively. All four sectors registered higher growth rates than the average for Chinas overall exports.

Table 2 shows the rise in the world market share of Chinas exports of manufactures with medium skill and technology intensity. At the end of the period Chinas global position was not dominant; the countrys exporters held a 9.8 percent market share in 2011, roughly the same as Japans and slightly higher than that of the U.S., at 9.5 percent. In this category, Germany remains way ahead of the competition; its market share has remained stable at around 16 percent, which is remarkable considering the period includes the global financial crisis.

Although China-made manufactures are voluminous, they still remain relatively uncompetitive in the global market. Normally we adopt a measure called “Revealed Comparative Advantage” (RCA) to evaluate the competitiveness of a product. Products with an RCA exceeding 1.5 have certain international competitiveness, while those with an RCA exceeding 2 are classed as very competitive. According to statistics from UNCTAD, in the period from 2001 to 2011, the competitiveness of Chinamade products improved, though in general it remains weak. Chart 2 reveals that RCA values for Chinas manufactured goods were all below 1.5. The RCA values of the countrys labor-intensive and resource-based products, however, were all above 2.5, indicating they were competitive in global markets. Standouts included textile fibers, yarn, fabrics and clothing, all of which had RCA values in excess of 2.9.

The RCA values of manufactures with low skill and technology intensity were far lower than those of labor-intensive and resourcebased manufactures. The average RCA of manufactures with medium skill and technology intensity remained lower than 1. The RCA of iron and steel and road vehicles was especially low, signifying their poor international competitiveness, despite the high volume of production for export.

The average RCA value of Chinese manufactures with high skill and technology intensity has been steadily climbing, though it is yet to reach 1.5, signifying such goods are yet to be internationally competitive. Chinas global manufacturing position could still be improved; the countrys labor is still mostly put to use in industries with low skill and technology intensity. Furthermore, its manufactures lack brandname presence, and many manufacturers concentrate on merely processing medium and high skill and technology intensity goods. In short, China cant yet compete with developed countries in terms of design and marketing capabilities. But its getting better.

Over the past few years, the Chinese government has placed great importance on innovation and technology upgrading. The country has accelerated the elimination of excess production capacity in 19 industrial sectors. In 2011, R&D and internal investment stood at 5.71 percent of principal business revenues for large industrial enterprises. Mergers and reorganization efforts in key sectors have made much headway. In 2011, the concentration ratio of the top 10 enterprises in the automaking, steel, shipbuilding and cement sectors hit 87 percent, 49.2 percent, 47.7 percent and 26.5 percent respectively. In the coming years, China is aiming to make further adjustments to the structure of its industry by boosting scientific research and development and raising allocative and productive efficiency. Improving brand presence of the countrys exporters will also enhance overall competitiveness of “Made in China.”