Sharing the Pie

2011-11-17 15:27:12ByLANXINZHEN

Beijing Review 2011年6期

By LAN XINZHEN

Sharing the Pie

By LAN XINZHEN

China’s securities market opens further to foreign investment banks

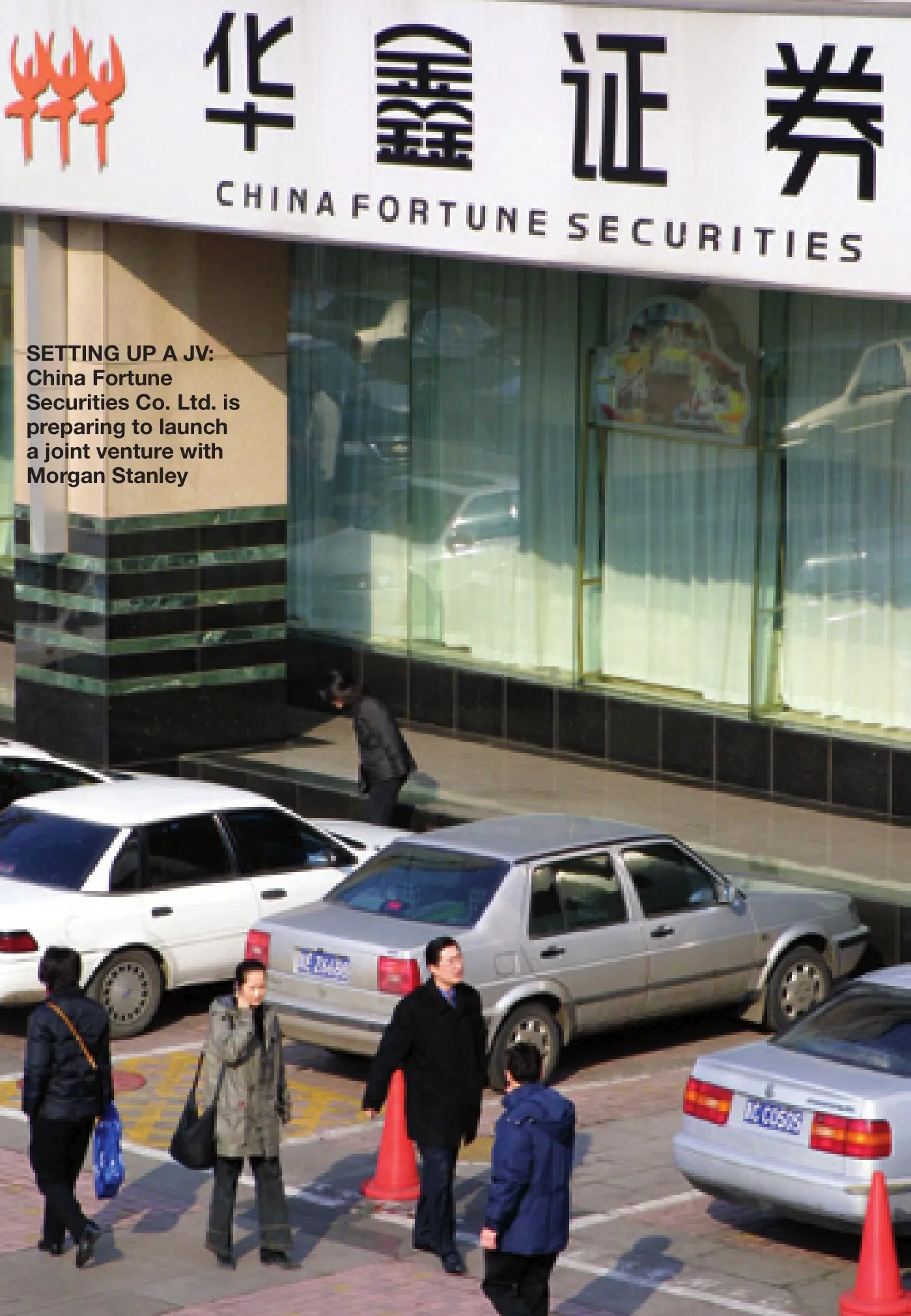

New members will soon join the roster of Chinese foreign securities joint ventures—JPMorgan Chase is preparing one with First Capital Securities Co. Ltd., and Morgan Stanley is partnering with China Fortune Securities Co. Ltd.

The joint ventures were approved by the China Securities Regulatory Commission (CSRC) on December 31, 2010, and will start business operations in the second quarter this year.

The joint venture between First Capital and JPMorgan Chase JV will be headquartered in Beijing and the one between Morgan Stanley and China Fortune Securities, headquartered in Shanghai. In each joint venture, the foreign party holds 33 percent of the shares, the maximum shares foreign parties can hold in securities joint ventures in China.

At the end of 2010, the CSRC approved three securities joint ventures, with the third one between the Royal Bank of Scotland and Guolian Securities Co. Ltd., approved last November.

Thus, 10 securities joint ventures have been set up in China since it entered the WTO in 2001 and opened its securities market.

Meanwhile, Citigroup is going to team with Central China Securities Co. Ltd. and Australia’s biggest investment bank Macquarie Group Ltd. is also planning a joint venture with Hengtai Securities Co.

Foreign banks like the Hongkong and Shanghai Banking Corp. Ltd., Hang Seng Bank Ltd. and the Bank of East Asia, Ltd. have also shown an interest in looking for partners to establish securities joint ventures in China.

The reason foreign securities companies are accelerating their steps in China is simple: They are optimistic about the growth of the Chinese securities market. According to a PricewaterhouseCoopers (PwC) report, in 2010, 349 companies made initial public offerings (IPOs) in China’s A-share market, ranking first in the world. These companies raised funds worth 478.3 billion yuan ($72.7 billion), hitting a record high. PwC estimates in 2011 capital raised may be around 400 billion yuan ($60.8 billion).

With their capital advantages, advanced management concepts and mature operation experience, foreign investment banks will be a powerful rival of domestic securities companies by establishing joint ventures.

Small and medium-sized Chinese securities companies also dream of cooperating with foreign partners. In China there are more than 100 securities companies. According to the CSRC statistics, in 2009, China Fortune Securities Co. Ltd. ranked 30th among all Chinese securities companies by underwriting 7.8 billion yuan ($1.18 billion) worth of stocks, while First Capital Securities Co. Ltd. ranked 33rd by underwriting 6.75 billion yuan ($1.02 billion). With help from Morgan Stanley and JPMorgan Chase, the two Chinese securities companies may see higher growth in the future.

Securities Joint Ventures in China

● China International Capital Corp. Ltd.

● China Euro Securities Ltd.

● Daiwa SSC Securities Co. Ltd.

● Goldman Sachs Gao Hua Securities Co. Ltd.

● UBS Securities Co. Ltd.

● Credit Suisse Founder Securities Ltd.

● Zhong De Securities Co. Ltd.

Zigzag opening

China’s securities market was born in 1990. The country’s first joint venture investment bank—China International Capital Corp. Ltd. (CICC)—was established in 1995, with Morgan Stanley being one of its foreign partners. CICC is qualified for underwriting stocks issued by Chinese listed companies.

After the country became a WTO member in 2001, its securities market was opened to foreign companies.

However, to protect the fledgling market, China only allows foreign securities companies to enter the Chinese securities market by cooperating with Chinese partners. The country also formulated the Rules for the Establishment of Foreign-Shared Securities Companies. According to the rules, foreign securities companies can hold no more than 33 percent of shares in securities joint ventures; securities joint ventures can only be engaged in IPOs of domestic companies and brokerage of foreign stocks, but not allowed for brokerage of domestic stocks and derivatives business.

This policy was implemented as of July 2002. On December 19, 2002, China Euro Securities Ltd., the first securities joint venture after China entered the WTO, was approved by the CSRC. Registered in Shanghai, China Euro Securities was co-established by Hunan-based Fortune Securities Co. Ltd. and CLSA Asia-Pacific Markets, with a 67-33 percent shareholding structure.

After China Euro Securities, several other securities joint ventures were founded, including Daiwa SSC Securities Co. Ltd., UBS Securities Co. Ltd. and Goldman Sachs Gao Hua Securities Co. Ltd.

During this period, a large number of domestic securities companies were established; some good, some bad. Malpractice at securities companies, such as embezzling customers’ transaction funds, brought unforeseen troubles to investors and market development. In response, the CSRC started comprehensive rectification of securities companies from 2004, and examination and approval of new securities joint ventures suspended thereafter.

In August 2007, the comprehensive rectification of securities companies was completed and during the second China-U. S. Strategic Economic Dialogue, held in May of that year, the Chinese Government agreed to annul the ban on foreign securities companies accessing the Chinese market and issue new licenses of securities companies, including joint ventures. It also agreed to allow foreign securities companies to further expand their business scope in China before the third Strategic Economic Dialogue.

At the end of December 2007, as one of the fruits of the third China-U.S. Strategic Economic Dialogue, the CSRC publicized the revised Rules for the Establishment of Foreign-Shared Securities Companies and newly formulated Provisions for Trial Implementation on Establishing Subsidiary Companies by Securities Companies, both effective since January 1, 2008. Examination and approval of securities joint ventures were resumed, but the speed was anything but quick. Within the following three years, only two securities joint ventures were approved: Credit Suisse Founder Securities Ltd. and Zhong De Securities Co. Ltd.

CFP

Some Chinese securities researchers have expressed their concerns about whether securities joint ventures approval will be accelerated this year.

Chen Zhengrong, a researcher at the Research Institute of Haitong Securities Co. Ltd., said the Chinese securities market is steadily opening up. And with this opening up, the Chinese securities market has become more closely connected with the global securities market in terms of market tendency, resource distribution among different industries and other aspects.

“However, opening the Chinese securities service industry should be carried out in an orderly and gradual way,” Chen said.

Just emerging from the global financial crisis, China should control the opening of the securities market and give top priority to risk prevention, Chen said. The Chinese securities market is now in a primarily mature stage, with distinct characteristics of an “emerging and transitional market.” The opening process of the securities market should not only promote development and improvement of the market, but also maintain domestic financial security and stability.

Fierce competition

Securities joint ventures’ development in China is unstable and difficult, maybe because the Chinese securities market was just opened and foreign securities companies are still getting used to the new environment. From IPO underwriting in 2010, joint ventures fell behind their Chinese competitors.

According to figures from Wind Information Co. Ltd., 58 securities companies gained underwriting fees worth 17 billion yuan ($2.58 billion). Of the total, six joint ventures just got IPO projects from 20 companies and earned underwriting and recommendation fees of 1.39 billion yuan ($210.93 million), only 8.1 percent of the total.

Among the top 10 securities companies in China, only CICC was a joint venture. With five IPO projects, CICC earned underwriting and recommendation fees of 700 million yuan ($106.22 million), ranking seventh among all securities companies in China. Zhong De Securities Co. Ltd. underwrote seven IPO projects and gained 263 million yuan ($39.91 million), ranking 20th. UBS Securities Co. Ltd. obtained two IPOs and earned 170 million yuan ($25.8 million), ranking 40th. Daiwa SSC Securities Co. Ltd. got one IPO order and earned 10.1 million yuan ($1.53 million), ranking sixth from last. In 2010, Goldman Sachs Gao Hua Securities Co. Ltd. had no IPO orders.

In contrast, domestic securities companies grew fast in 2010. The top nine domestic securities companies underwrote 181 IPOs, more than 50 percent of the market’s total and earning 54 percent of the total underwriting and recommendation fees. Ping An Securities Co. Ltd. won 38 IPOs and earned underwriting and recommendation fees of 1.99 billion yuan ($301.97 million), ranking first both in IPO number and underwriting revenue. Then came Guosen Securities Co. Ltd. with 32 orders, Huatai United Securities Co. Ltd. with 23, GF Securities Co. Ltd. with 21 and China Merchants Securities Co. Ltd. with 20.

Market analysts think the major reason for the failure of securities joint ventures is their unclear internal governance. Disagreements between the two parties may exist, and since joint ventures are held to a smaller business scope, the development of their investment banking business is limited.

But this does not mean securities joint ventures are not competitive.

In 2007 when the Chinese stock market soared, CICC, UBS Securities Co. Ltd. and Goldman Sachs Gao Hua Securities Co. Ltd. occupied the first, third and sixth position in the Chinese market in terms of underwriting and recommendation revenue. They participated in IPOs of large state-owned enterprises including PetroChina Co. Ltd., China Pacific Insurance (Group) Co. Ltd. and China Railway Group Ltd. In 2009, CICC maintained the top title.

Today, most foreign financial institutions consider securities joint ventures as a window to enter the Chinese securities market. At their initial stage of development, the main goal is to develop mutual understanding and gain experience. The planned international board affiliated to the Shanghai Stock Exchange may be their real target, where offshore companies are allowed to sell shares denominated in Chinese currency.