Research on the Formation Mechanism for the Co-agglomeration of Producer Services and Manufacturing in the Guangdong-Hong Kong-Macao Greater Bay Area

2023-11-05 02:21:44JiaoPingHuangFeibinandLiSusu

Contemporary Social Sciences 2023年5期

Jiao Ping,Huang Feibin,and Li Susu

Guangdong University of Finance &Economics

Abstract: The Guangdong-Hong Kong-Macao Greater Bay Area is witnessing a surge in economic development,showcasing robust resilience in the co-agglomeration of producer services and manufacturing industries,along with the increasingly evident impact generated by such co-agglomeration.Based on the panel data collected from ten cities in the Guangdong-Hong Kong-Macao Greater Bay Area (excluding Zhaoqing)spanning from 2010 to 2020,we examined the formation mechanism for industrial co-agglomeration in the area from three dimensions: industrial correlation,spatial correlation,and policy guidance.Our analysis was based on a vertical correlation model and was validated using the seemingly unrelated regressions (SUR)method.The findings are as follows: (a) There currently exists no spatial correlation between the producer services and manufacturing sectors in the area,and the correlation between the two remains limited to the former providing specialized services to the latter.(b) Policy guidance has a positive impact on the location selection of industries within the area.By implementing a comprehensive range of favorable policies,local governments can provide effective and scientifically guided recommendations regarding the location of producer services and manufacturing sectors.Therefore,it is crucial to foster the collaboration between producer services and manufacturing sectors and further enhance the co-agglomeration between the two sectors.In addition,the government authorities should also strive to enhance its economic governance capacity,thereby facilitating the formation of such co-agglomeration.

Keywords: Guangdong-Hong Kong-Macao Greater Bay Area,producer services,manufacturing,co-agglomeration,policy guidance

Currently,the Guangdong-Hong Kong-Macao Greater Bay Area is witnessing a surge in economic development,showcasing robust resilience in the co-agglomeration of producer services and manufacturing sectors.In the early stages of reform and opening up,the cities in the Pearl River Delta region,by leveraging Hong Kong’s and Macao’s open business environment and convenient transportation conditions,gradually developed a novel economic cooperation model,which involves manufacturing and service sectors.The implementation of this model has facilitated enterprises based in the Pearl River Delta to expand their trade operations globally.However,the producer services sector in the Pearl River Delta relatively lags behind the progress of the manufacturing sector.As a result,these two sectors have yet to establish a robust synergy for complementary development.To transform the Guangdong-Hong Kong-Macao Greater Bay Area into a world-class manufacturing hub,it is imperative to actively foster co-agglomeration of producer services and manufacturing sectors and enhance their spatial correlation so as to generate spillover effects and promote the optimization and upgrading of the manufacturing sector as well as regional economic growth.So,what is the mechanism underlying the formation of the coagglomeration of producer services and manufacturing sectors? What measures can the Greater Bay Area take to effectively promote such co-agglomeration in order to promote economic development? The response to the aforementioned questions holds immense practical significance for the Greater Bay Area in facilitating the transformation and upgrading of its manufacturing sector,as well as establishing a globally competitive modern services industry system.

Ellison and Glaeser (1997,pp.889–927) first proposed the co-agglomeration theory,positing that industries characterized by input-output correlation tend to exhibit spatial agglomeration.This phenomenon represents a bidirectional dynamic coordination process between industry and space.Previous studies have primarily focused on the industrial level when examining industrial agglomeration.Some scholars found that the industrial correlation between producer services and manufacturing sectors can facilitate the co-agglomeration of these two sectors (Ke et al.,2014,pp.1829–1841;Ji &Duan,2014,pp.79–84).The producer services sector and the manufacturing sector often demonstrate a significant level of spatial proximity in industrial distribution.The proximity allows producer services enterprises to leverage the customer base of the manufacturing sector while also enabling manufacturing enterprises to access cost-effective services (Coffey &Bailly,1991,pp.95–117;Klaesson,2001,pp.375–394).

However,with the advancement and refinement of the new economic geography theory,scholars are now able to extend their analysis beyond the industrial level and incorporate spatial factors within the theoretical framework.Chen Na and Gu Naihua(2013,pp.25–44) found a spatial co-agglomeration effect between producer services and manufacturing sectors,which can be primarily attributed to the availability of resources and services.Furthermore,such spatial co-agglomeration varies across different cities.Zhang Hu and Han Aihua (2019,pp.39–50) argued that the interaction and mutual influence between producer services and manufacturing sectors at the industrial level will undoubtedly lead to spatial co-agglomeration or co-location.Chen Guanghan and Ren Xiaoli (2021,pp.143–152) have concluded,based on the center-periphery theory,that the urban agglomeration of the Guangdong-Hong Kong-Macao Greater Bay Area demonstrates a distinctive industrial layout characterized by core cities prioritizing the development of producer services while peripheral regions focus on advancing manufacturing.These two sectors demonstrate a mutually beneficial interactive relationship aimed at achieving coordinated development.

In recent years,some scholars have incorporated policy factors into the analytical framework of industrial co-agglomeration.According to Chen Xiaofeng (2017,pp.89–96),policy guidance is a key factor contributing to the co-agglomeration of producer services and manufacturing sectors.Xu Zhongrong (2022,pp.93–100) posited that the mechanism underlying the co-agglomeration of producer services and manufacturing sectors in metropolitan areas is evidenced through synergies across various dimensions,including policy,structure,space,and quality.Song Xiaoling and Li Jinye (2023,pp.56–65) argued that the policy environment can impose both constraints and incentives on the formation and development of industrial co-agglomeration.Additionally,it can establish a fair competition environment and a robust legal framework for such coagglomeration.

The existing literature has provided valuable insights and references for this study.However,most studies primarily focus on industrial correlation and spatial correlation when examining the mechanism underlying industrial co-agglomeration.Some studies only explore the impact of policy factors on industrial co-agglomeration.Consequently,there is a lack of research that simultaneously considers all three dimensions of industry,space,and policy.The primary contribution of this paper lies in its comprehensive analysis of the formation mechanism of industrial co-agglomeration,which encompasses three dimensions: industrial relevance,spatial relevance,and policy guidance.Additionally,it employs a vertical correlation model for empirical testing,which significantly enriches the research content of the industrial co-agglomeration theory.

Analysis of Formation Mechanism

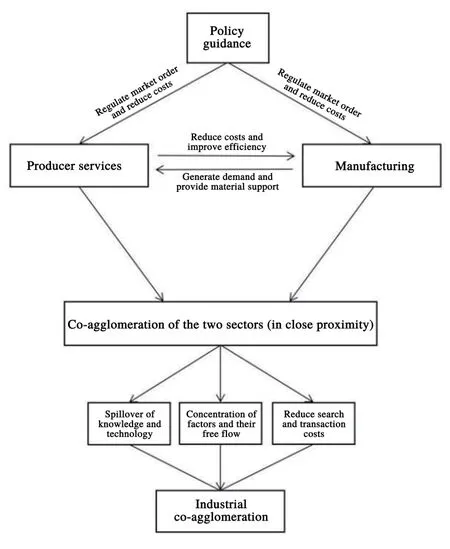

The present study investigates how industrial co-agglomeration between producer services and manufacturing sectors is formed,considering the three dimensions of industry,space,and policy simultaneously (see Figure 1).

Figure 1 Roadmap for the formation mechanism of industrial co-agglomeration

Industrial Correlation

According to the industrial correlation theory,if one industry utilizes the output of another industry as its raw material,there exists a forward correlation between these two industries;Otherwise,there exists a backward correlation.Inessence,the manufacturing and producer services sectors are the products of the increasing specialization in the industrial division of labor.It is also a process wherein vertical integration of production transitions into vertical specialization.Consequently,there exists a robust upstream and downstream industrial correlation between these two sectors.This is primarily manifested in the fact that producer services contribute to cost reduction and efficiency enhancement in manufacturing,while manufacturing provides demand and material support for producer services (Feng &Liu,2005,pp.51–56).

The producer services sector,which offers indispensable intermediate inputs to the manufacturing sector,has progressively integrated itself into the core production links of the manufacturing sector through its specialized expertise and cutting-edge technology.Its main service support for the manufacturing industry lies in cost reduction and efficiency improvement,thereby achieving industrial co-agglomeration.From the perspective of production costs,if the internal costs generated by a particular production process exceed the expenses associated with outsourcing,manufacturing enterprises will opt to outsource that process in order to reduce costs and improve efficiency.In terms of capital turnover costs,the producer services can provide an optimal financial service system to address financing challenges faced by the manufacturing sector,such as limited funding channels and slow financing speed.In terms of logistics costs,the producer services can effectively reduce the fixed costs associated with warehousing and transportation for manufacturing enterprises,thereby enhancing the transportation efficiency of products.

The manufacturing sector generates demand and provides material support for producer services,thereby enhancing the efficiency of producer services to achieve industrial coagglomeration.The producer services sector needs to leverage specific carriers to realize the value of its own service products.The road transport sector,for instance,relies on dedicated trucks from the automobile manufacturing sector to provide freight services.These trucks serve as essential material support provided by the manufacturing sector to facilitate transportation.The manufacturing sector,in its pursuit of industrial transformation and upgrading as well as the enhancement of its competitive advantage,has set a higher standard for producer services.The producer services sector is consistently enhancing its expertise and expanding its scale to meet the growing specialization requirements of the manufacturing sector.This will undoubtedly result in an improvement in both service quality and production efficiency,thereby strengthening industrial co-agglomeration.

Spatial Correlation

The spatial layout of producer services and manufacturing sectors exhibits a tendency towards co-agglomeration based on the correlation between these two sectors.The agglomeration of industries within the manufacturing sector can generate significant market demand for the producer services sector.To cater to the diverse needs of numerous manufacturing enterprises,an increasing number of producer services enterprises will inevitably establish their presence in the agglomerative area,thereby giving rise to the phenomenon of intra-industry agglomeration (Ellison &Glaeser,1997,pp.889–927).Jacobs’ externality theory suggests that knowledge spillover has the potential to transpire across diverse industries.The close spatial proximity between the producer services sector and the manufacturing sector facilitates the concentration and efficient flow of resource factors,thereby promoting resource sharing and facilitating knowledge and technology spillovers,ultimately enhancing the level of industrial co-agglomeration.

Spatial proximity can also reduce the search costs between producer services and manufacturing.It shortens the geographical distance between enterprises,facilitating the manufacturing sector in their search and comparison of intermediate inputs.Additionally,it enables producer services to expand their service scope and conduct market demand research more effectively.For example,the presence of multiple financial institutions in close proximity can greatly benefit a manufacturing enterprise facing financial difficulties.It allows the enterprise to compare and select from various institutions,thereby reducing the financing costs associated with project negotiation.Additionally,these institutions can provide customized services to the specific needs of the manufacturing enterprise and improve their service system,thereby effectively minimizing the search costs of the manufacturing enterprise (Coffey &Bailly,1991,pp.95–117;Klaesson,2001,pp.375–394).

Policy Guidance

The deepening of the social division of labor separates the producer services sector from the manufacturing sector,giving rise to a relatively independent new business form.The producer services sector,when confronted with limited market size,can rely on the market mechanism to fulfill development demands owing to its streamlined operational model and a narrower scope of products and services.However,as the manufacturing sector presents increasingly professional and diversified demands,the producer services sector is faced with a complex market environment.In such circumstances,an intermediate organization is needed to regulate the relationship between the market and enterprises,which is typically assumed by local governments whose policy guidance will profoundly impact the layout and development of related industries.

The rationality and applicability of policy guidance have a positive impact on market order and transaction costs,subsequently influencing the level of co-agglomeration of producer services and manufacturing sectors.The market environment of inter-industrial agglomeration,which refers to the spatial agglomeration of different industries,is characterized by a higher level of complexity in the market environment in comparison to intra-industry agglomeration.Therefore,the implementation of appropriate policies can effectively optimize market order and mitigate transaction costs.The formulation of appropriate policies should be based on the distinctive characteristics inherent in each industry.For producer services,which primarily offer intangibly specialized services,policies should be formulated with the aim of accurately assessing the market value of such services while establishing a standardized market order for industrial co-agglomeration.Moreover,as manufacturing enterprises often require a significant amount of space for their operations,it has a substantial impact on the spatial planning of cities,particularly in terms of dividing functional areas.The implementation of appropriate policies can effectively guide the transfer of industries within the manufacturing sector to align with urban development needs and promote the growth of the manufacturing sector.In addition,the implementation of rational policies can attract producer services enterprises to establish their presence near the manufacturing agglomeration area,thereby promoting industrial co-agglomeration.This will not only reduce enterprises’ search costs but also enhance connectivity between them,ultimately leading to a decrease in mutual transaction costs.However,the market order may become chaotic,and transaction costs may rise when policies are not that rational or applicable,especially if there are conflicting policies between cities.This can significantly impact the flow of factors and economic exchanges.Therefore,the formulation and implementation of rational policies,such as those aimed at optimizing the regional institutional environment and enhancing marketization,can facilitate the co-agglomeration of producer services and manufacturing sectors (Song &Li,2023,pp.56–65).

Research Hypotheses

The manufacturing enterprises in the Guangdong-Hong Kong-Macao Greater Bay Area are primarily concentrated in the Pearl River Delta,which boasts a robust foundation in manufacturing.The need for production model transformation in the area has led to a growing demand for producer services.The 14th Five-Year Plan in Guangdong province explicitly proposes expediting the establishment of 20 strategic industrial clusters,highlighting the undeniable significance of producer services in shaping the spatial layout of the manufacturing sector.Based on this,we propose the first hypothesis:

H1: The availability of producer services has a positive impact on the location of the manufacturing sector.

The manufacturing sector in the Guangdong-Hong Kong-Macao Greater Bay Area has not extensively integrated producer services into its core production links.Manufacturing industries closely associated with producer services are primarily concentrated in resourceintensive sectors,and their products do not offer the necessary support for the further development of producer services.In the current market environment,the market demand for producer services is primarily focused on the fundamental production link.Therefore,the second hypothesis of this paper is proposed:

H2: The availability of the manufacturing sector has a negative impact on the location selection of the producer services sector.

The nature of the production and operation of producer services and manufacturing sectors indicates that the producer service sector is a knowledge-intensive industry primarily offering intangible services,with labor cost and quality being its main production costs.In comparison,the manufacturing sector predominantly produces tangible products utilizing various production factors such as resources,labor force,and specialized services provided by the producer services sector.Based on the above statement,we propose the third hypothesis:

H3: Production and transaction costs have a negative impact on the spatial layout of producer services and manufacturing sectors.

In light of the current situation faced by producer services and manufacturing sectors,the government authorities in the Greater Bay Area have implemented a range of policies.These include initiatives such as theMainland and Hong Kong Closer Economic Partnership Arrangement(CEPA) aimed at promoting trade liberalization in services and trade as well as investment facilitation between the two regions.Additionally,they have adopted a “double transfer strategy” involving the transfer of industry and labor force to guide certain manufacturing industries to relocate to other cities.As a result,these measures have significantly enhanced industrial co-agglomeration in the area.Based on this,we propose the fourth hypothesis:

H4: Policy guidance has a positive impact on the location selection of industries.

Model Building and Variable Description

Model Building and Variable Selection

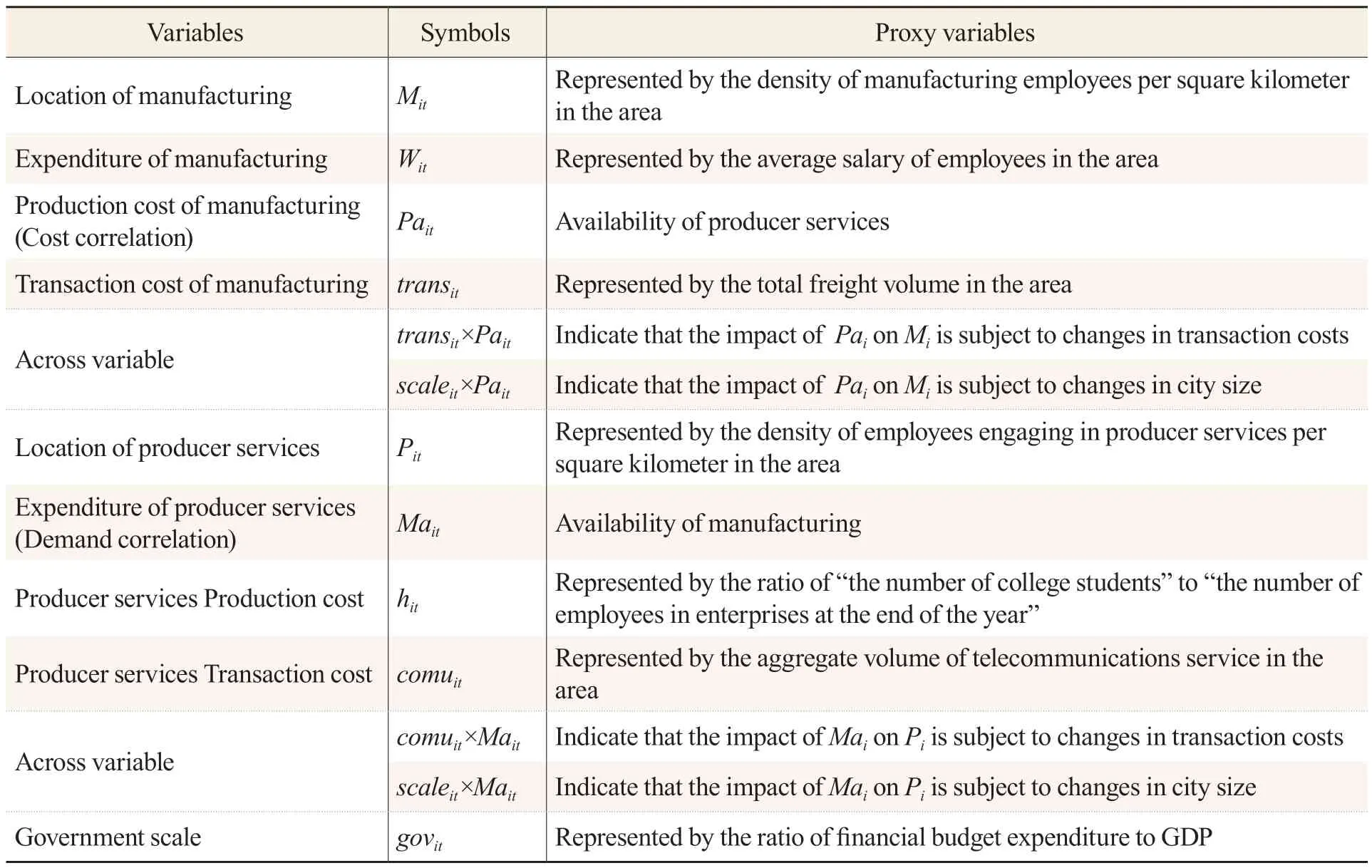

The empirical test in this paper is based on Venables’ model of vertically linked industries (Venable,1996,pp.341–359).According to this model,when there exists a correlation between demand and cost in two industries,the two industries exhibit a vertical input-output correlation.When considering the producer service and manufacturing sectors as research subjects,demand correlation refers to one industry providing a robust market for another industry,thereby attracting enterprises to strategically locate themselves.Cost correlation signifies that an industry can effectively reduce its costs by establishing its presence within the vicinity of another industry agglomeration area.The industrial location signifies the extent of industrial agglomeration within a given region.In general,the greater the value of industrial location,the higher the level of industrial agglomeration.According to the derivation of the theoretical model,the location of the manufacturing sector and producer services sector can be depicted through a function incorporating variables such as production cost,consumption expenditure,and transaction cost.Following the principles of comprehensiveness,scientific rigor,and data availability,this study employs the approach of Gao Juemin and Li Xiaohui (2011,pp.151–160) and utilizes seemingly unrelated regression (SUR),which considers both the equation correlation and error term correlation,to estimate the equation set,thereby building the following model:

Equation (1) reflects the cost correlation within the vertically linked industries.The location of the manufacturing sector is influenced by factors such as the location of producer services,consumption expenditure,and transaction costs.The choice of the availability of the producer services sector as a proxy variable for the production cost of the manufacturing sector is based on the recognition that,with the expansion and excess capacity in traditional manufacturing industries,the knowledge-intensive producer services sector has become a crucial factor in elevating the added value and heterogeneity of products (Glasmeier &Howland,1994,pp.197–229).Therefore,when examining the co-location relationship between producer services and manufacturing sectors,it is appropriate to utilize the availability of producer services as a representation of the production costs of manufacturing.Equation (2) reflects the demand correlation within the vertically linked industries.The location of the producer services sector is influenced by factors such as the location of the manufacturing sector,production expenditure,and transaction costs.Since manufacturing is the main downstream industry of producer services,it is appropriate to express the expenditure of producer services with the availability of the manufacturing sector.The meanings of variables in Equation (1) and Equation (2) are illustrated in Table 1.

Table 1 Interpretation of Variables in the Equation Set

Drawing on the practice of Chen Jianjun and Chen Jingjing (2011,pp.141–150) and based on the research content,we selected the following variables.The present study measures the industrial location by utilizing the density of industry-specific employees per square kilometer in the area.Here,Mitrepresents the location of manufacturing;Pitrepresents the location of producer services;Witrepresents the expenditure level of manufacturing,that is,the average expenditure required for each employee employed in the manufacturing sector,which is reflected by the average wage of employees in the area.Under normal circumstances,the average salary of employees in labor-intensive manufacturing industries is typically lower,whereas that in technology-intensive manufacturing industries tends to be higher.Transitrepresents the transaction cost of the manufacturing sector.The higher the volume of transportation and the lower the cost of transportation,the lower the transaction cost.As producer services are predominantly knowledge-intensive industries,the ratio of the number of college students to the number of employees in enterprises at the end of the year is utilized as a proxy variable,with the variablehitserving as an indicator of the level of knowledge intensity in regioni.The transaction cost of producer services (comuit) is measured by the aggregate volume of telecommunications services in the area,as producer services typically involve intangible outputs that are transmitted through channels such as the internet,rather than tangible goods.In general,the larger the aggregate volume of telecommunications services,the higher the level of regional information transmission and the lower the transaction cost.The present study utilized the permanent population of a city as a statistical criterion for measuring the scale of the city,which can effectively reflect the level of economic development and the extent of substance and factor aggregation and diffusion to examine the impact of city size on industrial location.For this paper,a year-end total population was selected as an indicator for measuring city size.The influence of policy guidance is often contingent upon the scale of the local government.The larger the scale of the government,the more robust the implementation of relevant policies.Therefore,the measurement of policy guidance in this paper is based on the scale of government (govit),which is represented by the ratio of government budget expenditure to gross domestic product (GDP).

The derivation for the availability of manufacturing industry and producer services are presented in Equation (3) and Equation (4),respectively:

θitin Equation (3) and Equation (4) represents the manufacturing (producer services)location of regioni,which is represented by the proportion of the number of employees of an enterprise in the total number of employees of the same industry in the whole region,based on the practice of Chen Jianjun and Chen Jingjing (2011,pp.141–150).tijdenotes the temporal distance between regioniand regionj,and is a distance decay variable.Specifically,the temporal distance refers to the duration required for traveling between two regions by car.In this study,the office addresses of governmental institutions in each city were selected as the starting points,and the temporal distance indicators (tij) were manually collected using AMAP.The value ofλis set to 0.017,based on calculations conducted by Hugosson and Johansson (2001).

Data Sources and Processing

The scope of this study is limited to industries represented by 2-digit numeric codes ranging from 13 to 43 within the manufacturing sector,as defined by theIndustrial Classification for National Economic Activities(GB/T 4754-2017).By referring to the revisedStatistical Classification of Producer Services(2019) and calculating the intermediate demand rate of the services and manufacturing sectors classified in theInput-Output Table of Guangdong Province(42 Sectors) in 2017,this study categorized four industries with an intermediate demand rate exceeding 50 percent as producer services industries.These industries encompass wholesale and retail,transportation,warehousing,and postal services,leasing,and business services,as well as finance.We redefined the producer services in Hong Kong and Macao by comprehensively referring to theHong Kong Standard Industrial Classification Version 2.0,the first revision ofMacao Industry Classification,and the statistical standard of the National Bureau of Statistics.The corresponding producer services in Hong Kong encompass transportation,warehousing,postal and courier services,wholesale and retail trade,finance and insurance,and information and communications,while those in Macao include transportation,warehousing and communications,wholesale and retail trade,real estate and business services,and finance.In view of the data availability,a panel dataset comprising ten cities in the Guangdong-Hong Kong-Macao Greater Bay Area (excluding Zhaoqing) from 2010 to 2020 was selected for research purposes.The data sources include theHong Kong Annual Digest of Statistics,Macao Yearbook of Statistics,Guangdong Statistical Yearbook,and statistical yearbooks of cities in the Pearl River Delta region from 2011 to 2021.

Empirical Results and Analysis

Baseline Regression Analysis

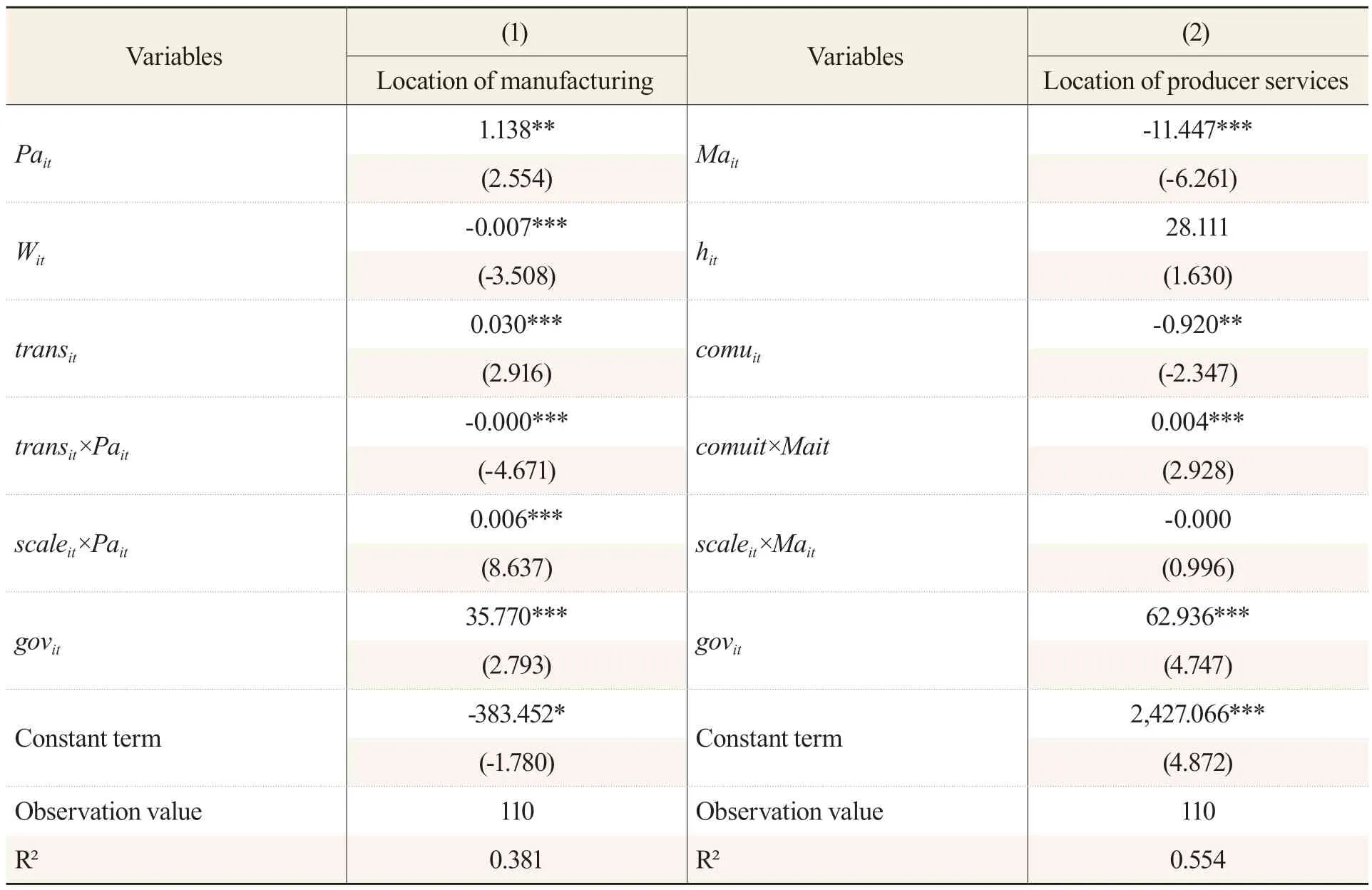

The estimated results of the equation set are shown in Table 2.Among the core explanatory variables,the availability of producer services,which measures the cost of manufacturing production (Pait),has a significant positive impact on the location of the manufacturing sector due to its provision of intermediate inputs that enable the latter into subsequent stages of production.On the other hand,the availability of costeffective and easily accessible specialized services offered by producer services in the production process will encourage manufacturing enterprises to strategically plan their layout there.However,the availability of the manufacturing sector,which measures the expenditure of producer services (Mait),significantly inhibits the location selection of producer services,indicating that the integrated development of these two sectors has not yet reached a level of reciprocal demand.Producer services still play a subordinate role in the manufacturing production chain and have yet to fully integrate into the core production processes of the manufacturing sector.As a result,the location of producer services and manufacturing sectors in the Guangdong-Hong Kong-Macao Greater Bay Area has not been strategically aligned,impeding further advancements in industrial coagglomeration within the area.

Table 2 Estimation of Baseline Regression Results Through SUR

In the control variables,the expenditure of manufacturing (Wit) has a negative impact on the location of the manufacturing sector.In other words,the increase in the average salary of employees does not promote the concentration of the manufacturing sector,indicating its reliance on low-end labor.This observation also provides insight into recruitment challenges faced in the Pearl River Delta in recent years.The coefficient of manufacturing transaction cost (transit) has a significant positive impact on the location of the manufacturing sector;that is,an increase in freight volume stimulates agglomeration within this sector,indicating that the improvement of transportation infrastructure and logistic services can improve transaction efficiency.Although the coefficient of transaction cost (hit) is high at 28.11,its impact on the location of producer services is not significant.This indicates that the increase of human capital investment in the Greater Bay Area is conducive to the agglomeration of producer services,but its impact on the degree of agglomeration remains limited due to its relatively small scale.Transaction costs (comuit) have a significant negative effect on the location of producer services,indicating that the improvement of the regional informatization level is not conducive to the agglomeration of producer services.

In the across variables,transaction costs and city size have different impacts on industrial location.From the perspective of transaction cost,there is a significant negative correlation between the location of manufacturing and the across variable (transit×Pait) representing manufacturing transaction cost and availability of producer services.This suggests that a reduction in transaction costs (an increase in freight volume) will exert a significant repulsive force on the location selection for manufacturing.This phenomenon can be primarily attributed to the fact that producer services are not reliant on traditional modes of transportation,and any enhancement in traditional freight transport efficiency will stimulate increased allocation towards traditional production factors within the manufacturing sector,consequently leading to crowding out effects on producer services.The across variable(comuit×Mait) representing the transaction cost of producer services and the availability of the manufacturing sector exhibits a significant positive correlation with the location of the producer services sector.This can be attributed to the fact that the reduction of transaction costs (increase of aggregate volume of telecommunications services) establishes an efficient communication channel between the producer service sector and the manufacturing sector,thereby facilitating agglomeration in the producer service sector.From the perspective of city size,the across variable representing city size and availability of producer services (scaleit×Pait) has a significant positive impact on the location of the manufacturing sector.This suggests that as cities grow in size and urban land prices rise,it becomes imperative for the manufacturing sector to increase its reliance on producer services as intermediate inputs in order to enhance its value-added capabilities and ensure smooth operations.Consequently,this facilitates the agglomeration of manufacturing activities.As for the location of producer services,the value of the across variable representing city size and manufacturing availability(scaleit × Mait) is negative and not significant,indicating that city size neither alleviates the availability of manufacturing nor has a negative impact on the agglomeration of producer services,but the impact is not obvious.

Government scale (govit) exhibits a significant positive correlation with the agglomeration of both the producer services and manufacturing sectors.The government scale reflects the extent to which it intervenes in the market.The empirical results indicate that through the implementation of well-designed policies,the Greater Bay Area will significantly enhance the spatial agglomeration of producer services and manufacturing enterprises.This shows that policies such as CEPA and the “double transfer strategy”have played a positive role in the agglomeration and transfer of the producer services and manufacturing sectors in the Greater Bay Area.

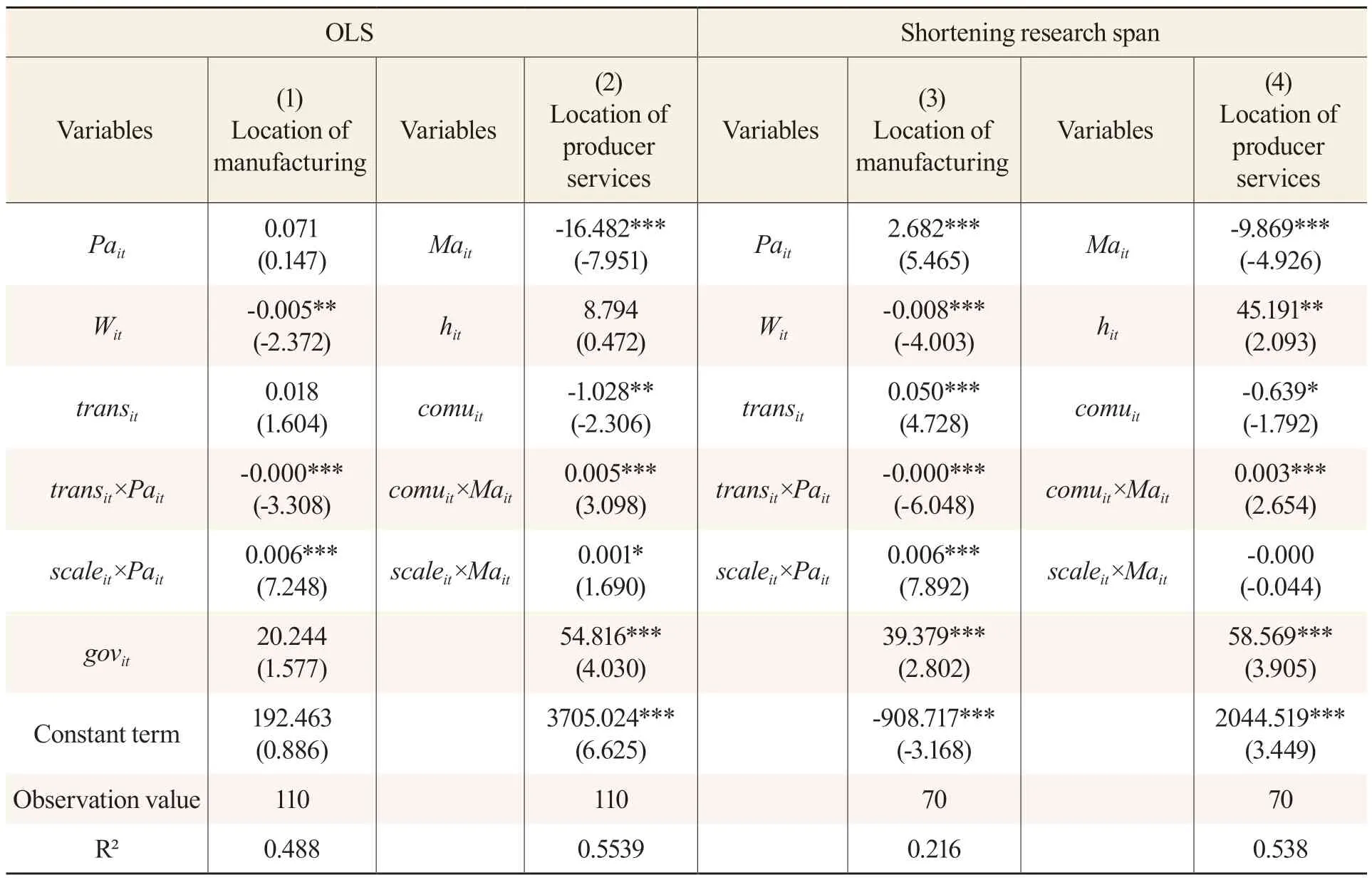

Robustness Test

The robustness test in this study was conducted using the ordinary least squares (OLS)estimation method and by shortening the research span.First,the robustness test was performed by using the OLS estimation method.As indicated in Table 3,the variable symbols of models (1) and (2) are consistent with the baseline regression results,except for differences in significance.Second,the robustness test was conducted by shortening the research interval.In the baseline regression,the research period spans from 2010 to 2020.The research period is narrowed down to 2014–2020 to mitigate potential interference caused by policies such as the“double transfer strategy” on industrial location.The regression results are presented in models(3) and (4) in Table 3,revealing that there is no significant deviation observed in the estimated results compared to those in baseline regression.Thus,the empirical analysis of the formation mechanism of industrial co-agglomeration in this paper is robust.

Table 3 Robustness Test

Analysis of Industry Heterogeneity

The SUR method was employed in this paper to conduct an empirical analysis of each subindustry within the producer services and manufacturing sectors.The specific findings are presented in Table 4 and Table 5.

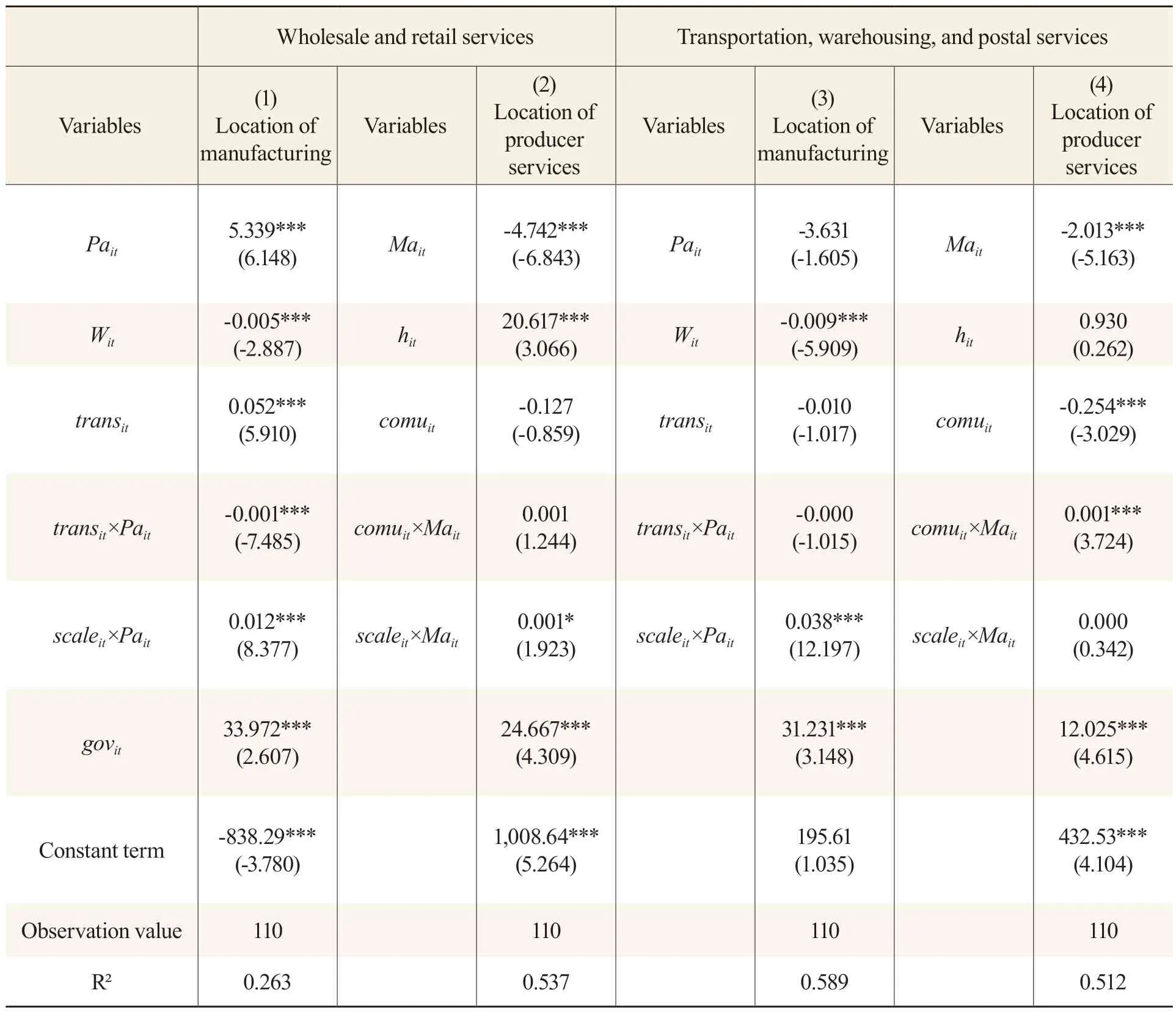

Table 4 Analysis of Industry Heterogeneity

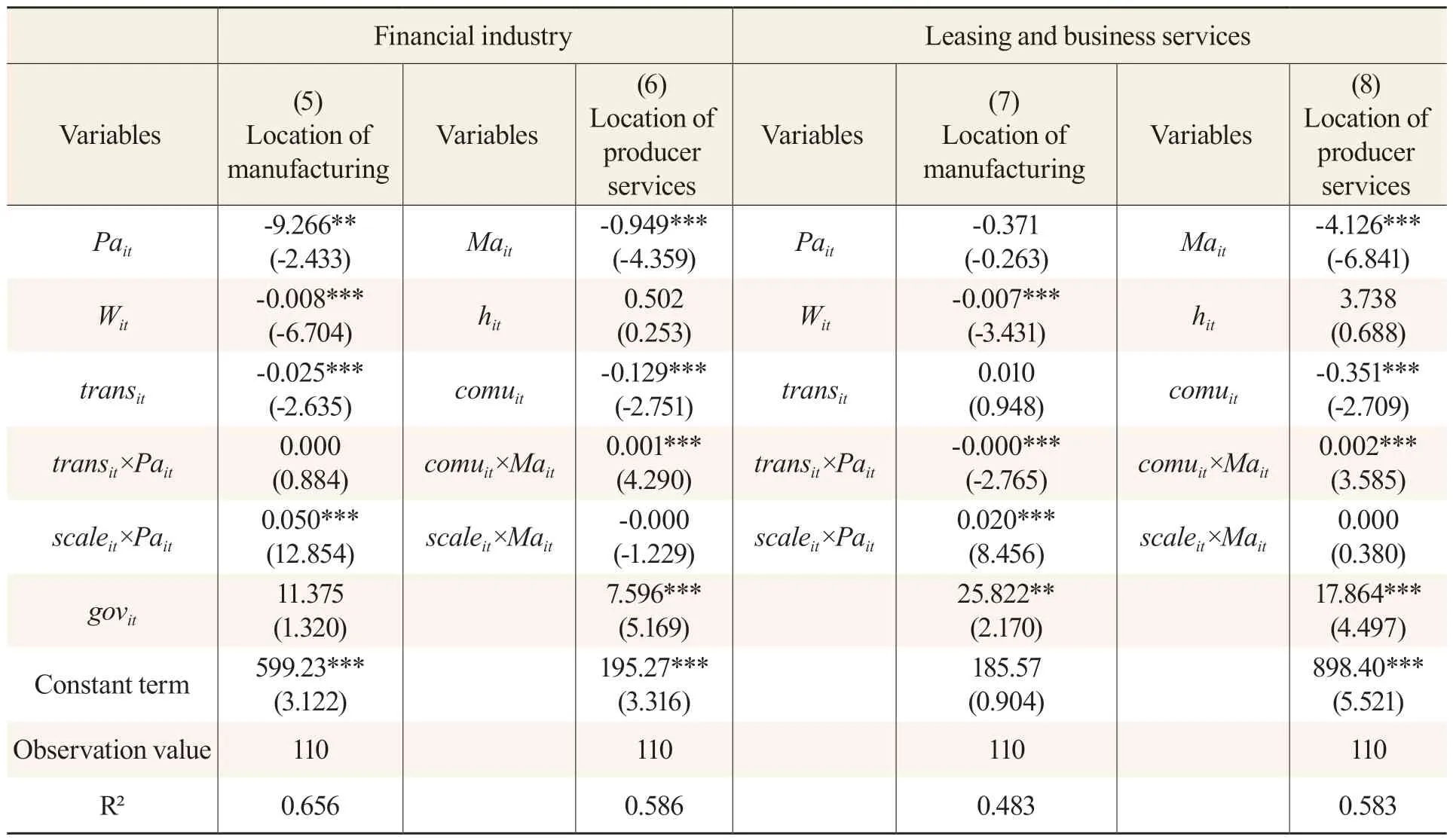

Table 5 Analysis of Industry Heterogeneity

Among the core explanatory variables,there exist significant differences in terms of the impact of the availability of various producer services (Pait) on the location of manufacturing,while there is a notable negative correlation between the availability of manufacturing (Mait) and the location of various producer services.In terms of the availability of producer services (Pait),only wholesale and retail trade exhibit a significant positive impact on the location of the manufacturing sector,whereas the availability of the financial industry has a significant negative impact on that.This could be attributed to the widespread distribution of wholesale and retail industries,which enables manufacturing industries to have closer proximity to consumer markets.Conversely,areas within the Greater Bay Area with well-developed financial industries,such as Guangzhou,Shenzhen,and Hong Kong,are facing high land prices,which hinders the production operations of the manufacturing sector there.Although the availability of the manufacturing sector(Mait) has a significant negative impact on the location of the producer services sector,the coefficients vary across different subsectors.Notably,the wholesale and retail trade exhibit the lowest coefficient,while the financial industry demonstrates the highest coefficient.These findings suggest that the availability of the manufacturing sector does not necessarily drive or promote the location selection of the producer services sector.From the above analysis,it can be further deduced that the producer services and manufacturing sectors in the Greater Bay Area have not yet formed the co-agglomeration in terms of spatial distribution.

Among the across variables,the impact of transaction cost and city size on the choices for industrial spatial distribution basically remains consistent with the overall analysis results.From the perspective of transaction cost,the across variables representing transaction cost and productivity availability (transit×Pait) exhibit a negative correlation with the spatial distribution of the manufacturing sector.This is particularly apparent in industries such as wholesale and retail trade,leasing,and business services.On the contrary,the across variable representing transaction cost and the availability of manufacturing (comuit×Mait) exhibits a positive correlation with the location of producer services,and only the coefficient of wholesale and retail trade fails to pass the significance test at one percent.From the perspective of city size,with the expansion of city size,the availability of various producer services (scaleit×Pait) has a significant positive impact on the spatial distribution of the manufacturing sector,of which the financial industry exhibits the highest value.However,the availability of manufacturing (scaleit×Mait) only has a significant positive impact on the wholesale and retail trade.

Government scale (govit) exhibits a positive correlation with both the producer services and manufacturing sectors.It is worth noting that only when referring specifically to the financial industry within the producer services sector will the impact of government scale on the location of the manufacturing sector become insignificant,while in all other cases,statistical significance is observed at a five percent level.This fully demonstrates that rational government intervention has a positive impact on guiding the location selection of both producer services and manufacturing sectors.During the process of economic development,the government’s efforts to promote the agglomeration of producer services and manufacturing sectors through investment attraction are consistent with the laws of economic development.

Conclusions and Policy Recommendations

Our research for this paper analyzed the formation mechanism of industrial coagglomeration from three dimensions: industrial correlation,spatial correlation,and policy guidance,based on the panel data collected from ten cities in the Guangdong-Hong Kong-Macao Greater Bay Area (excluding Zhaoqing) spanning from 2010 to 2020.The analysis was based on a vertical association model and was validated using the seemingly unrelated regressions (SUR) method.Finally,it drew the following conclusions: First,there currently exists no spatial correlation between the producer services and manufacturing sectors in the area,and the correlation between the two remains limited to the former providing specialized services to the latter.Specifically,the availability of producer services,which measures manufacturing production costs,has a significant positive impact on the location selection of the manufacturing sector,while the availability of manufacturing services,which measures the expenditure of producer services,has a significant negative impact on the location selection of the producer services sector.Producer services still play a subordinate role in the manufacturing production chain and have yet to fully integrate into the core production processes of the manufacturing sector.In terms of the availability of producer services,only wholesale and retail services exhibit a significant positive impact on the location of the manufacturing sector,whereas the availability of the financial industry has a significant negative impact on that.The availability of the manufacturing sector has a significant negative impact on the location of the producer services sector,but the coefficients vary across different subsectors.Among them,the wholesale and retail trade exhibit the lowest coefficient,while the financial industry demonstrates the highest coefficient.These findings suggest that the availability of the manufacturing sector does not necessarily drive or promote the location selection of the producer services sector.Second,policy guidance has a positive impact on the location selection of industries in the Guangdong-Hong Kong-Macao Greater Bay Area.The empirical results indicate that the government scale,the variable representing policy guidance,exhibits a positive correlation with both the producer services and manufacturing sectors.Moreover,the results remain robust when industry heterogeneity is taken into consideration,indicating that the implementation of a series of appropriate policies in the Guangdong-Hong Kong-Macao Greater Bay Area can significantly enhance spatial agglomeration in both producer services and manufacturing sectors.Furthermore,it is evident that rational government intervention plays a positive guiding role in determining the location selection of these sectors.

Based on the research conclusions,we put forward the following policy recommendations: Firstly,it is imperative to foster collaboration in the location selection of producer services and manufacturing sectors,thereby enhancing the level of industrial co-agglomeration.On the one hand,the government authorities should provide guidance to manufacturing enterprises in the Guangdong-Hong Kong-Macao Greater Bay Area on optimizing their organizational structure and eliminating certain production and service links that have lost their comparative advantages.Efforts should also be made to encourage these enterprises to fully leverage the advantages of the producer services sector to outsource their business.On the other hand,the Greater Bay Area should increase investment in the producer services subsectors,which own comparative advantages in the area,to fully leverage their role in promoting the manufacturing sector.For instance,it is necessary to make full use of Hong Kong and Macao’s robust foundation in the productive services sector to provide specialized services for the manufacturing sector in the Pearl River Delta region and facilitate its transformation and upgrading.Moreover,for service subindustries that are currently at a disadvantage but urgently needed in the area,government authorities can leverage spillover effects from neighboring regions or attract capital investment by enticing enterprises within these subsectors to establish branches in the locality,thereby further enhancing their alignment with the local manufacturing sector.Second,government authorities should constantly improve their economic governance capacity to promote industrial co-agglomeration.On the one hand,governments at all levels in the Guangdong-Hong Kong-Macao Greater Bay Area should innovate the communication mechanism to facilitate the co-agglomeration of producer services and manufacturing sectors within the area.The coordinated development and rational agglomeration of industries in the Greater Bay Area necessitate collaboration among government authorities across regions,given the interconnected interests among regions.To achieve this,governments at all levels should prioritize their overall interests,remove administrative barriers,clarify urban functions,effectively allocate responsibilities,and guide producer services and manufacturing enterprises to establish their presence in the Greater Bay Area to promote industrial co-agglomeration.

Contemporary Social Sciences2023年5期

Contemporary Social Sciences2023年5期

- Contemporary Social Sciences的其它文章

- Reflections on Cultivating Critical Thinking in Foreign Language Courses in the Context of Integrating Ideological and Political Theories in All Courses

- Value Orientation and Dimension Expansion of City Image Communication: A Case Study of Chengdu

- A Literature Review on “Non-Marriage”: A Global Comparative Perspective

- Evaluation of Green Development Efficiency in Chongqing Municipality Based on Super-SBM and Malmquist Models

- Research Methodology and Analysis of Innovative Pedagogical Models in Mechanical Engineering Courses for International Students at the School of Mechanical Engineering and Automation,Beihang University

- On the Ethical Dimensions of Literary Criticism in the Realm of We Media