Cotton market fundamentals & price outlook,April 2021

2021-07-06 03:46:10

China Textile 2021年2期

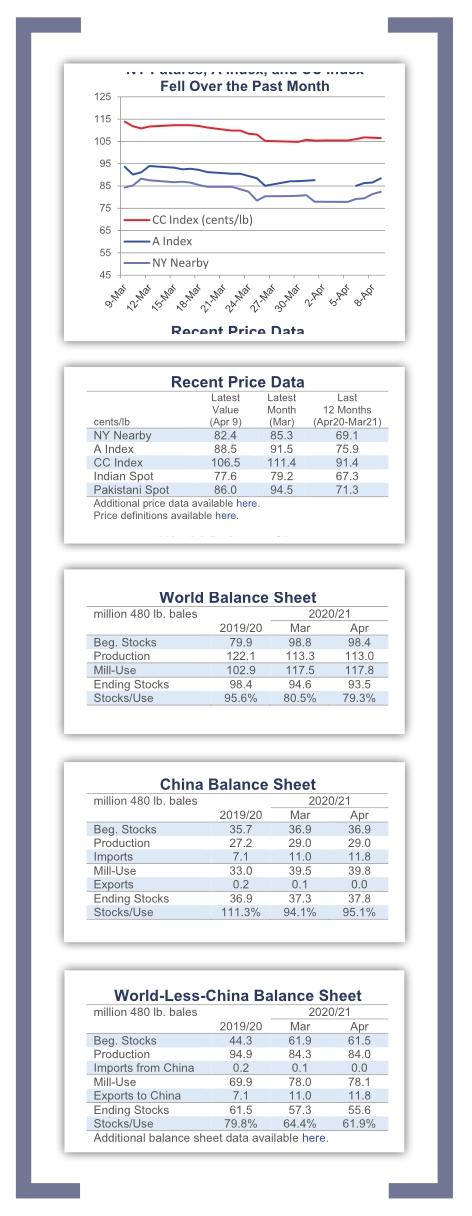

Recent price movement

All benchmark prices decreased over the past month.

The May NY/ICE futures contract fell from 88 to 78 cents/lb between early March and early April. In later trading, prices have rebounded to levels near 82 cents/lb.

The December NY/ICE futures contract fell from values around 85 cents/ lb in early March to those as low as 76 cents/lb near the end of that month. More recently, prices recovered to levels near 82 cents/lb.

The China Cotton Index (CC Index 3128B) fell from 114 to 106 cents/lb over the past month. In domestic terms, prices fell from 16,300 to 15,300 RMB/ ton. The RMB has weakened against the dollar since early March, from 6.52 to 6.56 RMB/USD.

Indian spot prices eased from 80 to 78 cents/lb in international terms. In domestic terms, values decreased from 45,800 to 45,400 INR/candy. The INR was relatively stable against the dollar over the past month, holding near 73 INR/ USD.

Pakistani spot prices declined from 95 to 87 cents/lb in international terms. In domestic terms, values fell from 12,300 to 10,800 PKR/maund. The PKR strengthened against the dollar over the past month, from 157 to 153 PKR.USD.

Supply, demand, & trade

The latest USDA report featured a small decrease in global production (-276,000 bales to 113.0 million) and a small increase in global mill-use(+387,000 bales to 117.8 million). An upward revision to world mill-use last crop year drove 2020/21 beginning stocks lower (-427,000 bales to 98.4 million).

The net effect of lower beginning stocks, lower production, and higher consumption was a 1.1 million bale reduction to the forecast for 2020/21 ending stocks (to 93.5 million bales). Nonetheless, the current figure for the global stocks-to-use ratio still ranks among the top six on record, and the current estimate for the world-less-China stocksto-use ranks among the top two in the modern era (since 2000/01).

At the country-level, the only notable change was for Australia (-100,000 bales to 2.5 million).

For mill-use, the largest revisions included those for China (+250,000 bales to 39.8 million), Bangladesh (+200,000 bales to 7.7 million), Mexico (+150,000 bales to 1.7 million), and Indonesia(-150,000 bales to 2.4 million).

The global trade forecast swelled 947,000 bales to 45.5 million. In terms of imports, the largest changes were for China (+750,000 to 11.8 million), Bangladesh (+200,000 to 7.4 million), Pakistan (+100,000 to 5.3 million), and Indonesia (-150,000 bales to 2.3 million). In terms of exports, the largest changes were for Brazil (+500,000 bales to 10.5 million), the U.S. (+250,000 to 15.8 million), and Egypt (+125,000 bales to 0.3 million).

Price outlook

China accounts for 32% of the current U.S. export commitment for 2020/21 delivery, and China has taken 39% of U.S. shipments so far this crop year.

In each of the five past crop years, China accounted for less than 20% of U.S. exports. The increase in Chinas share of U.S. exports comes from a meteoric rise in Chinese purchases in 2020/21. U.S. exports to China are up 276% year-overyear. The strength of Chinese demand has been the driver of the 15% year-overyear growth in overall U.S. shipments this crop year. Excluding China, U.S. exports are down 20% year-over-year.

The importance of Chinese demand to U.S. exports creates uncertainty for the market. In the Phase One deal, China promised to increase agricultural purchases in the 2021 calendar year (+$7.0 billion beyond 2020 levels). If fulfilled, this could be a factor that pulls U.S. stocks tight in 2021/22. If political tension between the two countries causes the deal to be abandoned, a negative reaction in prices could be expected.

Meanwhile, demand from other markets should improve. COVID vaccines are being distributed. Along with fiscal and monetary stimulus, the hope that the pandemic will be contained has lifted forecasts for economic growth.

The International Monetary Fund (IMF) just released a prediction that the global economy will expand 6.0% in 2021. This represents the strongest rate of growth in nearly five decades. Although some recovery in cotton consumption has already been enjoyed in 2020/21, global GDP growth is correlated with global mill-use. The acceleration in economic growth predicted in 2021 suggests a further boost to mill demand into 2021/22.

For price direction, any increase in global milluse will have to be balanced against production and stocks. The USDA will issue its first complete set of supply, demand, and trade forecasts next month. Although the weather, COVID, and trade policy will continue to create uncertainty for the outlook, their projections will help inform expectations for 2021/22.

- China Textile的其它文章

- Overview of textile situation in America

- Cotton market fundamentals & price outlook,March 2021

- Prosperity index of specialized market rebounds significantly in the past two months

- Development of nonwovens capacity and demand in Southeast Asia

- Start and prospects of industrial textile industry entering 2021

- Analysis of status and trend of global textile digital ink jet printing