New Opportunities Emerging for RMB Internationalization

2021-05-04 11:23ByXUGANG

CHINA TODAY 2021年4期

By XU GANG

THE onset of a global economic recession due to the COVID-19 pandemic and growing tensions between China and the U.S. in 2020 has fueled a spirit of pessimism around the world. The process of RMB internationalization nevertheless bucks the trend and is gaining momentum, which is undoubtedly heartening news in a generally gloomy time.

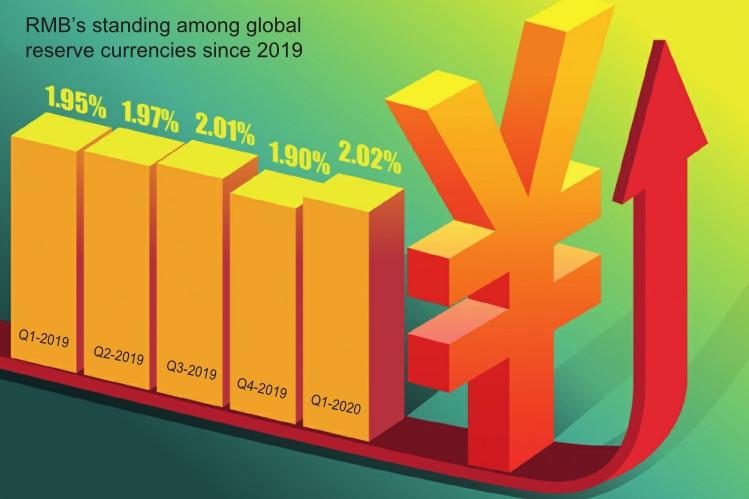

According to the RMB Internationalization Report 2019-2020 released by the China Banking Association, the volume of RMB cross-border settlements maintained strong growth despite the impact of the pandemic, increasing by 24.1 percent for 2019 and 36.3 percent in the first half of 2020. RMB is now the worlds fifth most used reserve currency, fifth preferred payment currency, and eighth foreign exchange currency. RMB cross-border settlement services have extended to 242 countries and regions around the world. And the Peoples Bank of China has signed bilateral currency swap agreements with the central banks of 39 countries and regions. All these mark a higher level of internationalization of the Chinese currency.

The process of RMB internationalization has not been all smooth sailing though. Talks on the issue started after China joined the WTO, but it was not until the 2008 financial crisis that the process truly took off. Facing the onslaught of a crushing financial tsunami, countries felt the urgency to take issues of national finance and currency into their own hands, and the call to reform the international monetary system became louder. Against this backdrop, RMB internationalization took the first step, and the first cross-border trade was settled in RMB in Shanghai in July 2009.

The year 2015 was a watershed in the process. On August 11 that year, China launched a reform of the exchange rate mechanism, putting an end to the expectation for lasting, unfailing appreciation of RMB, which marked a shift in the fundamentals of RMB internationalization. In November the same year the IMF announced its decision to include the RMB in the SDR basket, along with the U.S. dollar, the euro, Japanese yen, and British pound sterling. This expanded the RMBs function from a currency for trade settlement to one also for international investment, financing, and reserve status.

But in 2016 the anti-globalization trend surged, along with protectionism, trade conflicts between China and the U.S. escalated, and capital flight prompted national governments to tighten supervision of capital accounts. Under these escalating circumstances, the Chinese government and publics attention on RMB internationalization became superseded by concerns for trade disputes and financial concerns. The RMB internationalization process entered a low period, with certain indexes backsliding.

The headwinds at home and abroad have added to the challenges China faces in its development, but also given wings to RMB internationalization.

Facing the threat of the U.S. decoupling its economy from China, Chinese policy-makers have once again made RMB internationalization a priority, which also gained much public support. The signing of the phase one trade agreement between China and the U.S. didnt bring bilateral relations back on track to the previous level of openness and cooperation. Instead the Trump administration, failing to control the pandemic and jostling for re-election, shifted the blame onto China in an attempt to divert domestic attention and fury, sending Sino-U.S. tensions into a nosedive. During the past year or so, the U.S. has passed acts interfering in Chinas internal affairs, including those on Hong Kong, Xinjiang, and Taiwan, and added a lot more Chinese companies, institutions, and citizens onto its governance sanctions list to ratchet up suppression of China. In this context globalizing its currency becomes the only option for China to shield itself against the risks from U.S. sanctions, the dominance of dollar, and the central position of the U.S. in the global financial network. This decision has the backing of both politicians and public opinion in China.

As an ancient Chinese saying goes, “A just cause enjoys abundant support, while an unjust one finds little.”The abuse of sanctions by the U.S. has prompted more countries around the world to unpeg their currencies from the dollar, creating an enabling environment for RMB internationalization. All central banks have increased their gold reserves. Turkey, for instance, stocked up an additional 22.2 tons of gold in the first half of 2020 alone. Russia has dumped more than US $100 billion American treasury bonds in recent years. Multiple EU countries have joined the Instrument in Support of Trade Exchanges (Instex), a new channel to bypass U.S. sanctions and trade with Iran, and are trading with Iran through the financial messaging network SWIFT, and the first transactions have concluded. The Cross-border Interbank Payment System(CIPS), which provides clearing and payment services for financial institutions in the cross-border RMB and offshore RMB business, is also gaining traction, with the participation of 951 financial institutions in 97 countries and regions as of last July. Further opening-up of Chinas financial sector also facilitates RMB internationalization. After China introduced the exchange rate reform that allows two-way volatility for the value of its currency, some international investors complained that the insufficient development and openness of Chinas financial market and lack of RMBs convertibility under capital accounts hindered the smooth backflow of offshore RMB, and hence suppressed the proceeds of RMB products. This diminished its appeal as an international reserve, investment, or financing currency. This situation began to change in 2018.

New investment channels were opened, including Shenzhen-Hong Kong Stock Connect, ShanghaiLondon Stock Connect, and Bond Connect; RMB commodities futures, including those of crude oil, iron ore, copper, and rubber, were launched; Chinese stocks and government bonds have been included in relevant international index systems; and the RMB financial assets of foreign institutions and individuals are growing rapidly. Equity investment is now the main driving force for increase in cross-border use of RMB. Meanwhile, in the pilot free trade zones established in several Chinese provinces the trial reform for two-way opening of capital accounts is underway. After China lifted foreign ownership caps in more segments of the financial sector, including insurance and securities, increasing numbers of foreign financial institutions are coming to the country, which will further boost the circulation and connection of RMB assets in and out of China.

The swift recovery of the Chinese economy after the COVID outbreak and the stability of the RMB have further enhanced the Chinese currencys appeal. Thanks to effective measures to contain the virus and the mortality it inflicts, China was among the first countries to reopen its economy, and is one of the few major economies logging positive growth in 2020. This lays a firm foundation for RMB internationalization. China didnt choose a helicopter drop strategy or massive stimulus measures, and has maintained a prudent monetary policy. The benchmark interest rate of RMB has been staying within the range of 2-3 percent, which makes RMB assets even more appealing to investors. By contrast the U.S. is not expected to break free from massive quantitative easing any time soon, and the U.S. dollar index keeps falling. A weaker dollar will boost RMB internationalization.

The development of digital currency by Chinas central bank(DCEP) is preparing the ground for reshuffling in the international monetary system, and will inject new impetus into RMB internationalization. Amid the fierce race among central bank digital currencies (CBDC), countries around the world have stepped up research of theories and are exploring this sphere of financial activity. DCEP is now in the stage of conducting extensive trials in various scenarios, and is expected to be launched as one of the first CBDCs of a major economy. It has the potential of lowering cost of cross-border transactions, improving efficiency, and creating networked externalities, and therefore stands to be accepted by more users around the world.

Despite the aforementioned opportunities, the international standing of the RMB is still not commensurate with Chinas standing in the world economy, and its internationalization process remains a long journey punctuated by challenges arising in changes in both domestic and international economic and social environments. The decision to internationalize its currency is an act China has undertaken on its own initiative as well as one it feels compelled to take in response to the current situation. It is not aimed to seek financial hegemony in the world economy, but rather to better protect Chinas development interests. China is ready to carry out cooperation with other countries in establishing an international monetary system that is fair, neutral, and stable.

- CHINA TODAY的其它文章

- Pursuing High-Quality Development and a Better Life

- “Two Sessions”Reaffirm China’s Commitment to Wider,Win-Win Opening-up

- Xi Jinping Speaks with Guyanese President Irfaan Ali on the Phone

- Basic Research’s Share in R&D Funding Grew

- Five Measures to Construct a Modern Rural Industrial System

- Chinese Artist’s Ink Paintings Exhibited in Chicago