The effect of non-recurring items on analysts’earnings forecasts

2018-04-04 06:57NanLiHongtongSuWanqingDongKaiZhu

Nan Li,Hongtong Su,Wanqing Dong,Kai Zhu

aSchool of Accountancy,Shanghai University of Finance Business and Economics,China

bSchool of Accountancy,Shanghai University of Finance and Economics,China

cChina Securities Regulatory Commission Shanghai Commissioner’s Office,China

1. Introduction

This paper examines the effect of the disclosure of non-recurring items and their characteristics on analysts’forecast revisions.Unlike earnings generated from continuous operation,non-recurring items are one-time and contingent.The CSRC announcement“Explanatory Announcement No.1 of Corporate Information Disclosure on Public Issuance of Securities-Non-recurring items(2008)”de fines non-recurring items as“earnings from transactions and events which are not directly related to normal business,or related to normal business but influence statement users’decisions in the corporation’s business performance and profitability due to its special nature and contingency.”Questions arise from this:do the non-recurring items influence statement users’value judgments,and if so,how?

The literature has mainly focused on whether non-recurring items can be used to manipulate corporate earnings(Jaggi and Baydoun,2001;McVay,2006).In terms of the role non-recurring items played in statement users’decisions,research has mainly focused on the correlation between non-recurring items and stock price.Some researchers hold the view that the information involved lacks consistency.In that case,nonrecurring items have no incremental information for the capital market(Nichols,1973;Ramakrishnan and Thomas,l998;Castagna and Matolcsy,1989).Yang(2008)and Cready(2010)discovered that various nonrecurring items differed in consistency,which brought differences in value relevance.

Using analysts’forecast revisions as proxy for the information process outcome,this paper investigates the effect of non-recurring items on statement users’decision-making processes.As a group of statement users who possess professional knowledge,securities analysts predict the corporation’s future earnings level and provide investment advice.If non-recurring items are one-time,contingent and have no influence on the corporation’s future profitability,analysts will not revise future earnings forecasts.However,if non-recurring items contain information about the corporation’s future earnings changes,the analyst will revise earnings forecasts accordingly.

This paper uses Chinese A-stock companies in the Shenzhen and Shanghai security markets from 2009 to 2013 as a research sample to investigate the relationship between non-recurring items and analysts’forecast revisions.The empirical results suggest the following.(1)Analysts revise earnings forecast upwards when non-recurring gains occur,and do not revise earnings forecasts when non-recurring losses occur.The revision is asymmetric.(2)Due to changes in business scope,non-recurring items incorporate more information for analysts to revise earnings forecasts than other items.(3)When listed companies use non-recurring items to turn losses into gains for earnings management,analysts can see through this manipulation and revise the forecasts downward.

We conclude that non-recurring items incorporate information about corporate future earnings,but nonrecurring items of different types and from different sources have different effects on analysts’earnings forecast revision.Therefore,disclosure of non-recurring items is consistent with the requirements of statement users.This paper also provides empirical evidence for the further improvement of methods for disclosing nonrecurring items.

The remainder of the paper is organized as follows.Section 2 provides the institutional background,literature review and development of hypotheses.Section 3 describes our data and empirical methodology.Section 4 reports the empirical results and analyses.Section 5 concludes the paper.

2. Institutional background and theoretical analysis

2.1. Institutional background

Accounting theory holds that there are differences between recurring items and non-recurring items,and countries disagree on how to disclose non-recurring items.The U.S.Financial Accounting Standards Board(FASB)requires companies to recognize non-recurring items based on their business scope.In contrast,the accounting standard for non-recurring items in China is more standardized and consistent.In 1999,the CSRC clarified the concept and disclosure requirements of non-recurring items for the first time,and it has subsequently adjusted the definition of non-recurring items and disclosure requirements for several items.

In terms of items included,the CSRC first defined specific items of non-recurring gains and losses in 2001,which were divided into identified items and presumed items.In 2004,the CSRC canceled the classification and adjusted the specific items of non-recurring gains and losses.In 2007,the CSRC removed three obsolete items and added certain items such as net pro fit of subsidiaries under common Control for the current period from the beginning to the merger date,restructuring costs such as employee resettlement expenses and integration costs,and gains and losses arising from estimated liabilities unrelated to the company’s main business.Meanwhile,the CSRC adjusted the scope of items such as asset disposal income,government subsidies,asset consumption,non-monetary exchange pro fit and loss and other items.In 2008,further items were defined as non-recurring items,including gains and losses from financial assets or liabilities held for trading,and gains and losses on disposal of financial assets or liabilities held for trading and financial assets held for sale.

Although items included in non-recurring pro fits or losses can vary according to regulations,listed company disclosures of non-recurring items are highly comparable within the same accounting period and there is little possibility of manual adjustment.Information disclosure of endogenous issues can be well controlled in an investigation of the economic consequences of non-recurring items.

2.2. Literature review

A considerable body of research focuses on whether non-recurring items(as part of earnings)are a means of earnings management.According to Craig and Walsh(1989),Beattie and Brown(1994),Lin and wei(2000)and McVay(2006),non-recurring items are an effective means of earnings management.This practice is more common in unprofitable and low-pro fit companies that are eager to turn losses into gains(Wang and Jiawei,2008;Meng and Wang,2010).

However,there is no consensus on whether non-recurring items have value-relevance.Some researchers have suggested that non-recurring items have low value relevance because they provide non-continuous information and little incremental information for capital markets(Ramakrishnan and Thomas,l998;Castagna and Matolcsy,1989;Strong and Walker,1993).Cready(2010)found that frequently occurring nonrecurring items have a certain degree of continuity and value relevance.As disclosure frequency of nonrecurring items in previous quarters increases,the continuity and value relevance increases.The value relevance of non-recurring items will decrease with the decline in continuity,while the quality of accounting information will be improved and earnings management will be curbed if regulators expand the definition of nonrecurring items(Mu,2005).In addition,the market reacts differently to non-recurring items,which means that investors exploit information incorporated in non-recurring items when they make decisions(Meng and Wang,2010).

Although stock price is an important index of value relevance in accounting information research,as a synthetic index it is affected by profitability and earnings volatility.One-time and contingent non-recurring items affect the level and volatility of earnings.The direction and magnitude of its effect on stock prices are unknown.Therefore,it is not necessarily reasonable to evaluate the decision usefulness of non-recurring items in terms of stock price relevance.

2.3. Theoretical analysis

Securities analysts provide investment advice on stocks based on their forecast of company profitability.Compared to with normal investors,securities analysts place more emphasis on the company’s future profitability and underlying business reasons.Accounting information quality affects an analyst’s earnings forecast,including earnings forecast error,volatility and revision(Gleason and Lee,2003;Ivkovic and Jegadeesh,2004;Beyer,2008;Brown and Rozeff,1979;Dowen,1989;Clement et al.,2011).It is difficult for analysts to predict companies’non-recurring items,but the question of whether analysts care about the disclosure of non-recurring items and make revisions accordingly requires further study.

Non-recurring items are one-time and contingent.Analysts mainly base their earnings forecasts on the company’s continuous business,so it is difficult to effectively forecast future non-recurring items in advance.Given the features of non-recurring items(there is no relationship between the effect on current net pro fit and on future company pro fitability),even a large number of non-recurring items that leads to significant deviation in analysts’earnings forecasts will not change analysts’judgments of companies’future operating ability and profitability.Therefore,there is no relationship between non-recurring items and analysts’earnings forecasts.We thus have an irrelevance hypothesis.

However,non-recurring items arising from part of the business are not entirely contingent or one-time.Unlike continuing business,non-recurring items do not have long-term effects,but some non-recurring items such as those arising from corporate restructuring could have a relatively longer period of influence than actual contingent events.The influence of restructuring on book earnings is one-time,but restructuring might lead to a change in the nature of the business,which probably causes long-term effects on future earnings.When forecasting future earnings,analysts need to take business transformation and modification into consideration and revise earnings forecasts accordingly.If companies obtain positive non-recurring items through such business,this will lead to an increase in future earnings(asset restructuring,government subsidies,tax preferences and so on)or a reduction in future costs(gains on debt restructuring),which improves companies’future profitability and operating cash fl ow,thus increasing future earnings.

We emphasize that non-recurring items will not affect analysts’earnings forecasts and revisions if analysts are not concerned about them.However,if analysts do care about non-recurring items,even though they usually just need to arrive at the total net pro fit,they will revise earnings forecasts accordingly based on the sustainable effects of the non-recurring items.Therefore,analysts will revise earnings forecasts upward when there is a larger amount of non-recurring items,so we arrive at an effective attention hypothesis.We thus propose a pair of competitive hypotheses as follows.

H1a.There is no relationship between non-recurring items and analysts’earnings forecasts.(Irrelevance Hypothesis)

H1b.The higher the non-recurring pro fits or losses,the higher the likelihood and degree that analysts will revise earnings forecast upwards(Effective Attention Hypothesis).Furthermore,non-recurring items resulting from changes in business scope will have greater influence on analysts’earnings forecast revisions than other items.

As noted earlier,non-recurring items are an important means for low pro fit companies to manage earnings(Jaggi and Baydoun,2001;McVay,2006).If analysts believe that non-recurring items have no effect on companies’future earnings,they will not revise earnings forecasts even if companies use non-recurring items to turn losses into gains.If analysts think that non-recurring items will change companies’future earnings levels,but at the same time are not interested in the non-recurring items’implications for potential earnings management,they will just revise earnings forecasts mechanically.In that case,the issue of whether non-recurring items change companies’pro fits will not cause changes to analysts’earnings forecast revision.

If analysts pay attention to the number of non-recurring items and also analyze whether management manipulates non-recurring items to embellish their financial statements,then the higher the likelihood of earnings management in non-recurring items,the lower the likelihood that non-recurring gains or losses affect analysts’future earnings forecasts.When listed companies use non-recurring items to turn losses into gains,due to information asymmetry analysts might not be able to effectively identify which non-recurring items are relatively persistent.The result of“adverse selection”is that analysts will pay little attention to non-recurring items used to turn losses into gains when revising earnings forecasts,which will reduce the effect of nonrecurring items on their earnings forecast revision.Based on the discussion above,we propose the following hypotheses:

H2a.There is no correlation between non-recurring items used to turn losses into gains and analysts’earnings forecast revisions(Irrelevance Hypothesis and Mechanicalness Hypothesis).

H2b.The higher the volume of non-recurring items used to turn losses into gains,the lower the upward revision of analysts’earnings forecasts(Efficient Attention Hypothesis).

3. Research design

3.1. Sample and data

We select A-share listed companies in the Shenzhen and Shanghai stock markets from 2009 to 2013 as the sample.Analysts’earnings forecast revision data is obtained from the iFind database,and financial data is obtained from the Wind and CSMAR databases.Out of the total of 4563 firm-year observations that are available,we exclude extreme observations and those with missing values.We winsorize continuous variables at the 1%level to reduce the influence of outliers.

3.2. Models and variables

To begin,this paper examines whether non-recurring items have value relevance and whether they affect analysts’earnings forecast revision.Furthermore,we study whether analysts pay equal attention to nonrecurring gains and losses,and the extent to which different components of non-recurring items affect analysts’earnings forecast revision.In addition,we examine whether analysts can see through the manipulation of nonrecurring items to turn losses into gains and revise their forecasts accordingly.

To examine the relationship between non-recurring items and analysts’earnings forecast revision,model(1)is used to test Hypothesis 1:

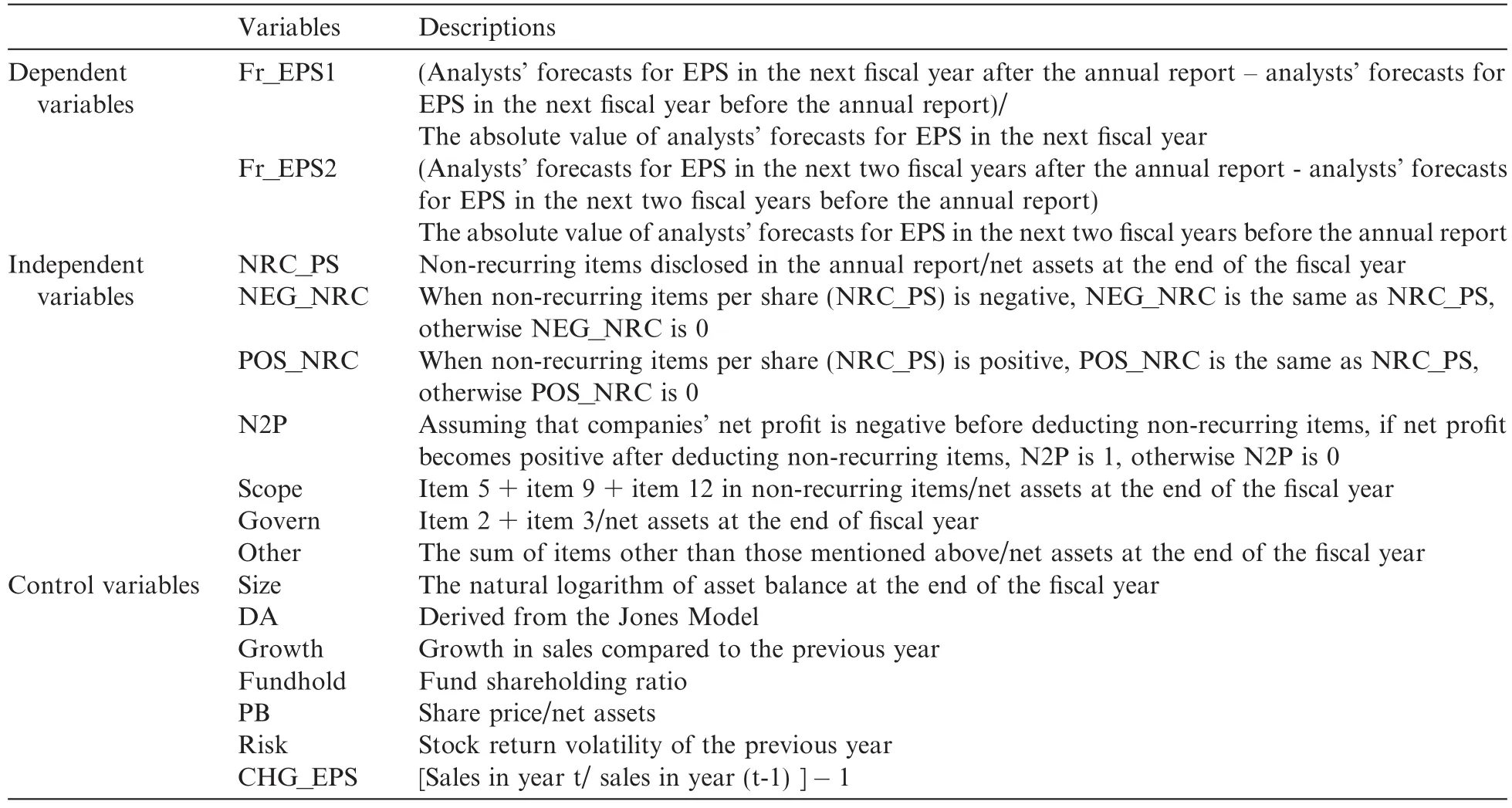

Fr_EPS1 and Fr_EPS2 are dependent variables in model(1).Fr_EPS1 refers to one-year analysts’earnings forecast revision,which equals analysts’forecasts for EPS in the next fiscal year after the annual report,less analysts’forecasts for EPS in the next fiscal year before the annual report,and then divided by the absolute value of analysts’forecasts for EPS in the next fiscal year before the annual report.Fr_EPS2 refers to two-year analysts’earnings forecast revision,which equals analysts’forecasts for EPS in the next two fiscal years after the annual report,less analysts’forecasts for EPS in the next two fiscal years before the annual report,and then divided by the absolute value of analysts’forecasts for EPS in the next two fiscal years before the annual report.By using absolute value in the denominator,we can identify whether analysts revise earnings forecasts upward or downward.The independent variable NRC_PS represents non-recurring items per share,which equals non-recurring items disclosed in the annual report divided by net assets at the end of fiscal year.The following variables are controlled in the model.Size refers to scale of assets,DA refers to the level of earnings management,Growth is firm growth,Fundhold represents the proportion of fund holdings,PB is pricebook ratio,Risk refers to stock return volatility in the previous year,CHG_EPS is change in profitability,and RPL(recurrent pro fit and loss)refers to recurring items.

Model(2)further analyzes the value relevance of non-recurring items by differentiating non-recurring items into non-recurring pro fits and non-recurring losses and then examining whether analysts’concern for nonrecurring pro fits and losses is symmetrical.

The definitions of the dependent variables are the same as above.The independent variables are NEG_NRC and POS_NRC.NEG_NRC refers to non-recurring losses per share.When non-recurring items per share(NRC_PS)is negative,NEG_NRC is the same as NRC_PS,otherwise NEG_NRC is 0.POS_NRC refers to non-recurring pro fits per share.When non-recurring items per share(NRC_PS)is positive,POS_NRC is the same as NRC_PS,otherwise POS_NRC is 0.Control variables are the same as above.

Model(3)examines whether different components of non-recurring items incorporate different information,which affects analysts’earnings forecast revision differently.Non-recurring items are divided into three categories to examine the relationship between each category and analysts’earnings forecast revision:nonrecurring items due to business scope changes,non-recurring items due to government policies,and other non-recurring items.

Table 1 Variable definitions.

The dependent variables in Model(3)are defined in the same way.Scope,the independent variable,refers to non-recurring items due to changes in business scope,which equals the sum of item 5,item 9 and item 12 in non-recurring items.1This definition of non-recurring items is from the China Securities Regulatory Commission Announcement[2008]No.43),Explanatory Announcement No.1 on Information Disclosure for Companies Offering Their Securities to the Public.Item classification numbers are derived from the Wind database classification of non-recurring items of pro fit and loss.Govern represents non-recurring items that result from government policies,which equals the sum of item 2 and item 3.Other refers to other non-recurring items,which is equal to the sum of those items not mentioned above.Control variables are the same as those in Model(1).

Model(4)is used to test Hypothesis 2—that is,whether analysts can see through the manipulation and then revise the forecasts downward when companies use non-recurring items to turn losses into gains.In Model(4),we add the interaction variable between extraordinary pro fit(or loss)and the dummy variable N2P to capture the weakening effect.

The definitions of the dependent variables in Model(4)are the same as above.N2P is a dummy variable that equals one if the company just turns the negative earnings to positive and equals zero otherwise.Assuming that companies’net pro fit is negative before deducting non-recurring items,if net pro fit becomes positive after deducting non-recurring items,N2P is 1 or 0.NRC_PS represents non-recurring items per share,which equals non-recurring items disclosed in the annual report divided by net assets at the end of the fiscal year.All variables except N2P are divided by net assets at the end of the fiscal year.Control variables are the same as those in Model(1).

All of the variable definitions are summarized in Table 1.

4. Empirical results

4.1. Descriptive statistics

Table 2provides descriptive statistics for the variables used in the regression analysis.It shows that oneyear analysts’earnings forecast revision(Fr_EPS1)has a mean(median)of-0.284(-0.013),which means that analysts’overall earnings forecast revisions are downward.Two-year analysts’earnings forecast revision(Fr_EPS2)has a mean(median)of-0.495(-0.013),indicating that a downward trend exists in analysts twoyear earnings forecast revision and there are considerable differences between analysts’one-year earnings forecast revision(Fr_EPS1)and analysts’two-year earnings forecast revision(Fr_EPS2).

In addition,NRC_PS has a mean of-0.4951,which means that overall net extraordinary pro fit is positive and accounts for 6.48%of net assets.POS_NRC has a mean of 0.0676 and NEG_NRC has a mean of-0.0023,indicating that in listed companies,average extraordinary gains are much larger than average extraordinary losses.

For each kind of non-recurring items,Scope has a mean of 0.03,which means that non-recurring items due to changes in business scope account for 3%of equity,while Govern has a mean of 0.0374,indicating that non-recurring items that result from government policies account for 3.74%.Of the two scenarios where non-recurring items change companies’earnings(from negative to positive,or positive to negative),the latter rarely happens,while 7%of companies use non-recurring items to turn losses into gains.For Control variables,earnings management has a large variance,suggesting that earnings management of listed companies is different in scale.Variances of the remaining Control variables are low,indicating that those Control variables are less discrete in the sample.

4.2. Empirical results

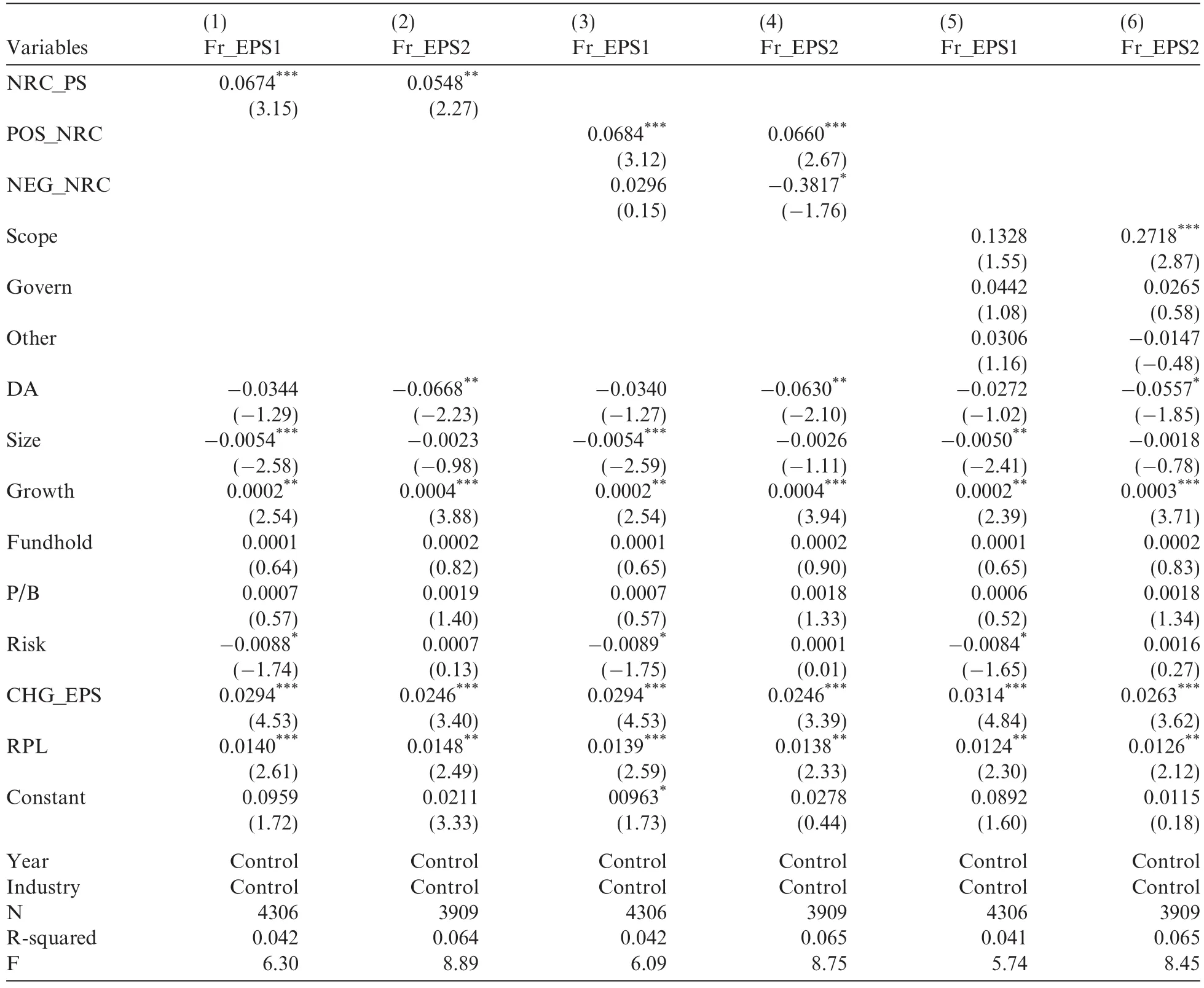

Table 3shows regression results for Hypothesis 1,where Fr_EPS1 is analysts’one-year earnings forecast revision and Fr_EPS2 is analysts’two-year earnings forecast revision.The independent variable NRC_PS measures non-recurring gains or losses per share and heteroscedasticity is controlled during the regression process.If the coefficient of NRC_PS is positive,then there is relevance between disclosure of non-recurring items and analysts’earnings forecast revision:non-recurring items incorporate incremental information and analysts absorb it.

Table 2 Descriptive statistics.

Table 3 Regression results for Hypothesis 1.

Columns(1)and(2)of Table 3 show that the coefficient of NRC_PS is positive and significant at the 1%(5%)level when the dependent variable is analysts’one-year(two-year)earnings forecast revision.This indicates that non-recurring items have value relevance and affect analysts’earnings forecast revision.The higher the volume of non-recurring items,the greater the likelihood and degree of analyst earnings forecast revision,which supports Hypothesis 1b.As Control variables,the coefficient of Size(Risk)is negative and significant at the 1%(10%)level when the dependent variable is Fr_EPS1.It is not significant when the dependent variable is Fr_EPS2,which suggests that analysts will revise one-year earnings forecasts downward with the increase in Size(Risk),but will not revise two-year earnings forecasts.The coefficients of Growth,CHG_EPS and RPL are significantly positive,which indicates that analysts will pay special attention to sales growth,changes in profitability and recurring items and revise their one-year(two-year)earnings forecast accordingly.The revision will be greater with the increase in Growth,CHG_EPS and RPL.The coefficient of DA is significantly negative if the dependent variable is Fr_EPS2 but not significant if the dependent variable is Fr_EPS1,indicating that analysts will revise two-year earnings forecasts downward but will not revise the one-year earnings forecast.The coefficients of P/B and Fundhold are not significant,which indicates that analysts will not revise earnings forecasts with changes in P/B ratio or Fundhold.

Columns(3)and(4)show that the coefficient of POS_NRC is positive(significant at 1%),meaning that analysts will revise earnings forecasts as non-recurring gains increase.However,the coefficient of NEG_NRC is not significant when the dependent variable is Fr_EPS1,indicating that the revision is asymmetric in oneyear earnings forecasts.The coefficient of NEG_NRC is negative(significant at 10%)if the dependent variable is Fr_EPS2,which indicates that non-recurring items could be a means for earnings management.When the company uses non-recurring items to lower earnings,analysts will see through this manipulation and revise earnings forecasts for the second year.

In the columns(5)and(6)of Table 3,only the coefficient of Scope is positive(significant at 1%),which indicates that Scope,Govern and Other are non-recurring items with different information implications,and affect analysts’earnings forecasts differently.Analysts focus on items 5,item 9 and item 12,which are non-recurring items resulting from changes in the business scope.Those caused by changes in government policies and other contingent,one-offitems will not significantly influence analysts’revision.

To sum up,analysts mainly care about items 5,9 and 12.Specifically,item 5 of non-recurring items is the difference between the investment cost of obtaining subsidiary incorporation,affiliated businesses and joint ventures and the gains generated from the fair value of identifiable net assets in the invested company.Item 9 is the pro fits or losses of restructuring.Item 12 is current pro fits and losses of a subsidiary generated by busi-ness combination under common Control from the beginning of the fiscal year to the merger date.The items above are usually caused by changes in a company’s business operating scope.Compared to non-recurring items caused by political reasons or other contingent events,the items above draw much more attention from analysts.

Table 4 Regression results for Hypothesis 2.

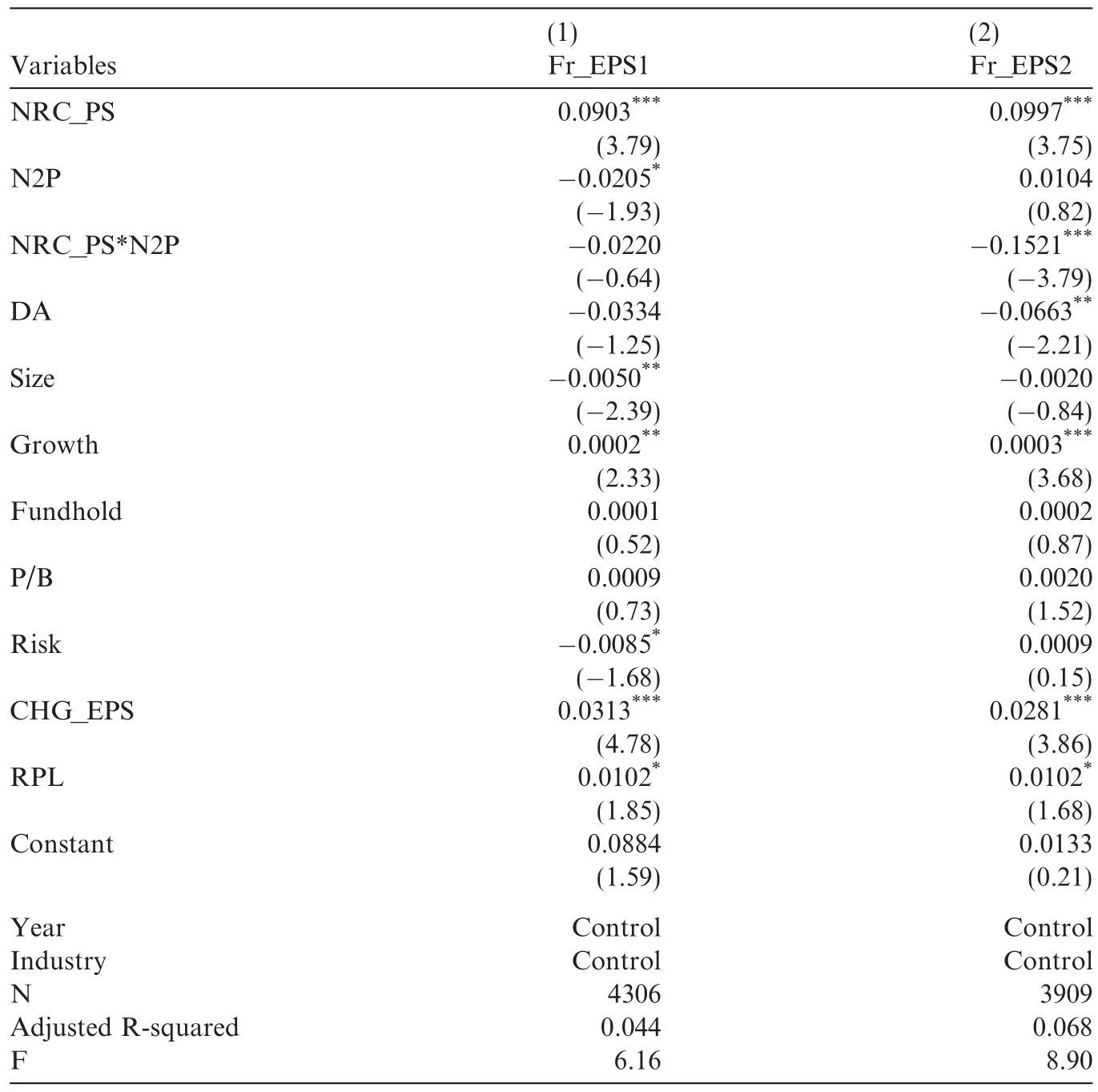

Table 4shows the empirical results from the examination of Hypothesis 2.The coefficient of the interaction NRC_PS*N2P is not significant in the first column but is significant at 1%level in the second column.This indicates that when companies use non-recurring items to turn losses into gains,analysts can see through this manipulation and then revise the forecasts downward,which is mainly reflected in analysts’two-year earnings forecast revision.When the dependent variable is Fr_EPS2,the sum of the coefficient of NRC_PS and that of NRC_PS*N2P is negative,which indicates that analysts will consider it as a bad performance signal and revise the forecasts downward if there is a comparative likelihood that management uses non-recurring items to turn losses into gains.

5. Conclusion

Decision usefulness is an important feature of accounting information.The question of whether decision makers can use accounting information to judge revision is an important measure of the quality of that information.Non-recurring items are an important part of accounting information.In a context of continuous reform and perfection of regulations and requirements on the disclosure of non-recurring items,this paper explores the effect of non-recurring items on statement users and specific expected changes.This knowledge can enhance discussions on decision usefulness,improve information disclosure and promote a healthy development of capital market.

Prior literature on non-recurring items focuses on earnings management,value relevance and so on.No consensus has been reached on whether non-recurring items incorporate information and how they influence financial statement users.However,we do not use stock price to examine the value relevance of non-recurring items.Due to the characteristics of non-recurring items,there is inevitably a large amount of noise,making it difficult for us to test whether non-recurring items provide incremental information.This paper tries to avoid pricing noise in the stock market and directly examines the effect of disclosing non-recurring items on economic behavior of certain information users,analyzing the relevance between analysts’earnings forecast revision and the information provided by non-recurring items.

Using the sample of A-share listed companies in the Shenzhen and Shanghai stock markets between 2009 and 2013,this paper discusses the direction,magnitude and range of analysts’earnings forecast revision upon disclosure of non-recurring items.Empirical results show that analysts revise earnings forecasts according to the disclosure of non-recurring items in the annual report,but the revision is asymmetric.Analysts revise earnings forecasts upward when net non-recurring pro fits occur,and the revision increases with the amount of net non-recurring gains.However,they will not revise earnings forecast downward when net non-recurring losses occur.This indicates that non-recurring items incorporate information increment.Moreover,analysts tend to be optimistic.They tend to revise their forecasts as a result of good news and respond less to bad news.In addition,this paper discovers that analysts will only revise earnings forecasts according to non-recurring items due to change in company business scope,which means that only those non-recurring items that can cause long-term business changes will in fluence financial statement users’decisions.Analysts will not revise earnings forecast for occasional,one-offitems that do not provide long-term business information for the future.Analysts can also see through the ways that management turn losses into gains by manipulating non-recurring items,and accordingly revise their forecasts downward.

This paper indicates that non-recurring items incorporate information on future earnings,which will affect statement users’judgment of firm value.Furthermore,non-recurring items from different sources provide different levels of incremental information.As key players in the information intermediary,analysts are able to interpret information on non-recurring items in financial statements.Full disclosure of non-recurring items can improve the quality of corporate financial reporting and help capital market investors to make decisions.Our research has reference value for regulators and investors.Disclosure of non-recurring items should be better regulated,especially the disclosure of non-recurring items that re fl ect companies’normal business.This is of great importance if we are to improve China’s information disclosure system,curb earnings manipulation by management,protect the interests of investors and promote healthy capital market development.

The authors thank the anonymous referees and the editor for their constructive suggestions.Any errors are the sole responsibility of the authors.This study is supported by the National Natural Science Foundation of China(Project No.71272008 and No.71632006),Social Sciences Major Issue Research Projects of The Ministry of Education of China(Project No.11JJD790008 and No.14JJD630005)and the Subject of Shanghai Education Committee(Project No.2014111143).

Beattie,Viven,Brown,Stephen,1994.Extraordinary items and income smoothing:A positive accounting approach.J.Business Finance Accounting 21,791–811.

Beyer,Anne,2008.Financial analysts’forecast revisions and managers’reporting behavior.J.Accounting Econ.,334–348

Brown,L.D.,Rozeff,M.S.,1979.The predictive value of interim reports for improving forecasts of future quarterly earnings.Accounting Rev.,585–591

Castagna,A.,Matolcsy,Z.,1989.The marginal information content of selected items in financial statements.J.Business Finance Accounting 16,317–333.

Clement,Michael B.,Hales,Jeffrey,Xue,Yanfeng,2011.Understanding analysts’use of stock returns and other analysts’revisions when forecasting earnings.J.Accounting Econ.51,279–299.

Craig,Russell,Walsh,Paul,1989.Adjustments for‘extraordinary items’in smoothing reported pro fits of listed Australian companies:Some empirical evidence.J,Business Finance Accounting 16,229–245.

Dowen,R.J.,1989.The relation of firm size,security analyst bias,and neglect.Appl.Econ.21(1),19–23.

Fan,Yum,Barua,Abhijit,Cready,William M.,2010.Managing earnings using classification shifting:Evidence from quarterly special items.Accounting Rev.85(4),1303–1323.

Gleason,Cristi A.,Lee,Charles M.C.,2003.Analyst forecast revisions and market price discovery.Accounting Rev.78(2),193–225.

Ivkovic,Zoran,Jegadeesh,Narasimhan,2004.The timing and value of forecast and recommendation revisions.J.Financ.Econ.73(2),433–463.

Jaggi,Bikki,Baydoun,Nabil,2001.Evaluation of extraordinary and exceptional items disclosed by Hong Kong companies.Abacus Sydney 37(2),217–232.

Lin,Shu,Wei,Minghai,2000.The earnings management by Chinese A-share firms in the IPO Process.China Accounting Rev.2(2),87–130.

McVay,Sarah E.,2006.Earnings management using classi fication shifting.Accounting Rev.56(2),501–531.

Meng,Yan,Wang,Wei,2010.Event study on market reaction to special items.China Accounting Rev.1,101–110.

Morong,Yang,2008.Research on Non-recurring Items Disclosure Issues–from the Perspective of Usefulness of Investors’Decisionmaking,Doctoral thesis.Hefei University of Technology.

Mu,Lanying,2005.How to deal with the non-recurring pro fits and losses of listed companies.Finance Accounting J.3,59–75.

Nichols,Donald R.,1973.The effect of extraordinary items on predictions of earnings.Abacus 9(3),81–92.

Ramakrishnan,Ram,Thomas,J.K.,1998.Valuation of permanent,transitory and price-irrelevant components of reported earnings.J.Accounting Auditing Finance,301–326.

Strong,N.,Walker,M.,1993.The explanatory powers of earnings for stock returns.Accounting Rev.68,365–399.

Wang,Junqiu,Jiawei,Tang,2008.Empirical study on management of non-recurring items in listed companies.China Manage.Inf.11,80–92.