Status quo of China’s knitting industry,Jan.—Oct.,2016

2017-03-03 09:38:28ByZhaoZihan

China Textile 2017年1期

By+Zhao+Zihan

The above-designated enterprises saw an overall smooth operation, knitwear better than knitted fabrics

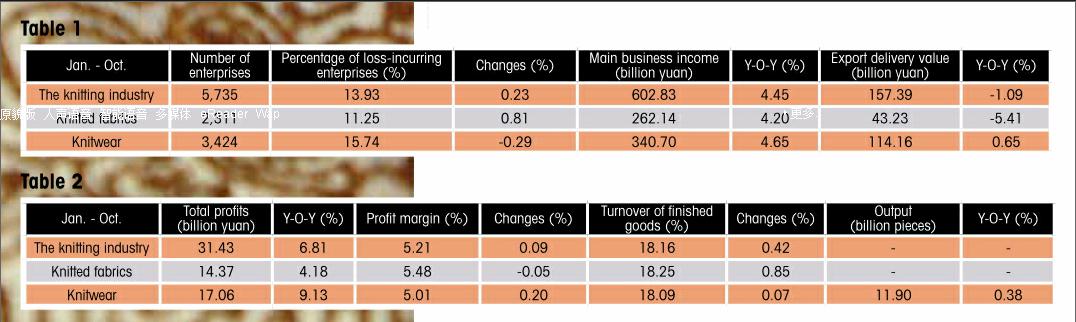

From January to October in 2016, 5,735 above-designated knitting enterprises witnessed the main business income of 602.83 billion yuan, an increase of 4.45% year on year, while the export delivery value decreased by 1.09% year on year and the percentage of loss-incurring enterprises increased by 0.23 percentage point. As for the knitwear sector, the range of loss reduced by 0.29 percentage point, while the main business income and export delivery value year on year were respectively better than the knitting industry in general. The knitted fabrics suffered increasing losses by 0.88 percentage point as well as a significant decline in export delivery value, down 5.41% year on year. (Table 1)

In the first ten months of 2016, the total profits of the knitting industry continued to grow, up 6.81% year on year, while the knitted garments increased faster than the knitted fabrics. The cumulative production reached 11.9 billion pieces, a slight year-on-year increase by 0.38%. The profit margin of the industry increased by 0.09 percentage point to 5.21% over the same period of the previous year, while the knitted fabrics enjoyed higher profit margins of 5.48% than the industry average. The turnover of finished goods increased 0.42 percentage point over the same period of the previous year, of which the knitted fabrics saw a relative high capital operating efficiency. (Table 2)

Increased pressures on exports, more decline on Y-O-Y growth

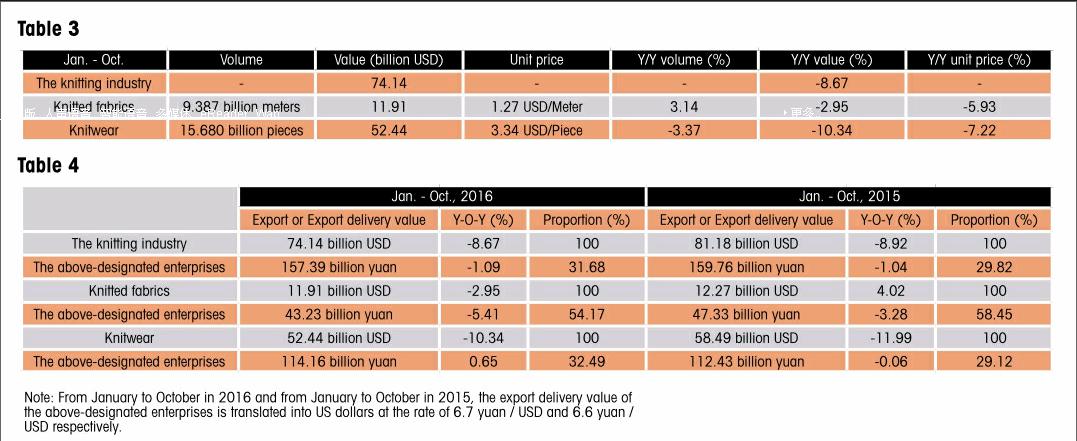

From January to October in 2016, the export value of knitting industry(including knitted fabrics, knitted garments and accessories) was 74.14 billion USD, down 8.67% over the same period of the previous year. Among them, the export of knitwear presented the largest dropping by -10.34%. The knitted fabrics saw increase in export volume but decrease in prices owing to the intensified low-cost competition caused by low international market demand. The knitwear suffered a decline in both export volume and value, while the export price showed a larger decreasing than the volume, up to -7.22%. (Table 3)

Increasingly obvious industry polarization, enhanced international competitiveness of large enterprises

From January to October in 2016, the proportion of the export delivery value of the above-designated knitting enterprises accounted in the whole industry increased 1.86 percentage points over the same period of the previous year, and that of the knitted garments grew by 3.37 percentage points, while the export delivery value of the above-designated knitting enterprises decreased by 1.09%, far less than the decline of -8.76% in export of knitting industry, indicating the better tenacity of the above-designated enterprises in response to the sluggish international markets.

During the first ten months of 2016, the export of knitted fabrics of the above-designated enterprises accounted for 54.17% of the total exports of knitted fabrics of the industry, indicating that the export of knitted fabrics were mainly from large enterprises, 4.28 percentage points lower over the same period of the previous year, while the decrease in export delivery value of the above-designated enterprises was larger than the industry. There is still some room for improvement for knitted fabric enterprises in response to market demand changes, while small and medium enterprises are enjoying certain advantages in meeting the market demands for a variety of knitted fabrics.(Table 4)

- China Textile的其它文章

- COTTON USA to make business connections at Heimtextil

- Interfilière Hong Kong has had a huge makeover

- ISPO BEIJING 2017:Exhibition space fully booked

- SPGPrints/Stovec achieve success at India ITME 2016

- Oerlikon Neumag BCF solutions offer maximum flexibility and efficiency

- Lenzing invests in new TENCEL?fiber plant in the USA